What is Global Enterprise Auto Dialer Software Market?

The Global Enterprise Auto Dialer Software Market refers to the worldwide industry focused on the development, distribution, and utilization of auto dialer software by businesses. Auto dialer software automates the process of dialing phone numbers, which is particularly useful for call centers, telemarketing, and customer service operations. This software can significantly enhance productivity by reducing the time agents spend manually dialing numbers and allowing them to focus more on actual conversations with customers. The market encompasses various types of auto dialer software, including predictive dialers, power dialers, and preview dialers, each catering to different business needs. The global market is driven by the increasing demand for efficient communication tools, the need for enhanced customer service, and the growing adoption of cloud-based solutions. As businesses continue to seek ways to streamline their operations and improve customer interactions, the Global Enterprise Auto Dialer Software Market is expected to see substantial growth.

On-premise, Cloud-based in the Global Enterprise Auto Dialer Software Market:

On-premise and cloud-based solutions are two primary deployment models in the Global Enterprise Auto Dialer Software Market. On-premise auto dialer software is installed and run on local servers within a company's own infrastructure. This model offers businesses greater control over their data and systems, as everything is managed internally. Companies with stringent data security requirements or those operating in regulated industries often prefer on-premise solutions because they can ensure compliance with specific standards and regulations. Additionally, on-premise solutions can be customized to meet the unique needs of a business, providing a tailored approach to auto dialing. However, on-premise solutions come with higher upfront costs, including expenses for hardware, software licenses, and IT personnel to maintain the system. They also require regular updates and maintenance, which can be resource-intensive. On the other hand, cloud-based auto dialer software is hosted on remote servers and accessed via the internet. This model offers several advantages, including lower initial costs, as businesses do not need to invest in expensive hardware or infrastructure. Cloud-based solutions are typically offered on a subscription basis, making them more affordable for small and medium-sized enterprises (SMEs) that may have limited budgets. These solutions are also highly scalable, allowing businesses to easily adjust their usage based on their needs. Cloud-based auto dialer software is maintained by the service provider, which means that updates, security patches, and technical support are handled externally, reducing the burden on internal IT teams. Additionally, cloud-based solutions offer greater flexibility, as they can be accessed from anywhere with an internet connection, making them ideal for remote or distributed workforces. Despite the benefits, cloud-based solutions also come with certain challenges. Data security and privacy concerns are significant, as sensitive information is stored on external servers. Businesses must ensure that their service providers comply with relevant data protection regulations and implement robust security measures. Additionally, reliance on internet connectivity can be a drawback, as any disruptions in service can impact the functionality of the auto dialer software. However, many cloud-based providers offer high levels of redundancy and uptime guarantees to mitigate these risks. In summary, both on-premise and cloud-based auto dialer software solutions have their own set of advantages and challenges. On-premise solutions offer greater control and customization but come with higher costs and maintenance requirements. Cloud-based solutions provide cost-effectiveness, scalability, and flexibility but require careful consideration of data security and internet reliability. The choice between the two models depends on a business's specific needs, budget, and operational requirements. As the Global Enterprise Auto Dialer Software Market continues to evolve, businesses will need to weigh these factors carefully to determine the best deployment model for their operations.

SMEs, Large Enterprises in the Global Enterprise Auto Dialer Software Market:

The usage of Global Enterprise Auto Dialer Software Market varies significantly between small and medium-sized enterprises (SMEs) and large enterprises. For SMEs, auto dialer software can be a game-changer in terms of efficiency and cost savings. SMEs often operate with limited resources and smaller teams, making it crucial to maximize productivity. Auto dialer software helps SMEs streamline their outbound calling processes, allowing sales and customer service teams to reach more customers in less time. This increased efficiency can lead to higher sales conversions and improved customer satisfaction. Additionally, cloud-based auto dialer solutions are particularly attractive to SMEs due to their lower upfront costs and subscription-based pricing models. These solutions provide SMEs with access to advanced features and functionalities without the need for significant capital investment. Furthermore, the scalability of cloud-based solutions allows SMEs to easily adjust their usage as their business grows, ensuring they only pay for what they need. In contrast, large enterprises often have more complex requirements and larger teams, necessitating robust and customizable auto dialer solutions. On-premise auto dialer software is often preferred by large enterprises due to the greater control it offers over data and system configurations. Large enterprises may have specific compliance requirements or internal policies that necessitate a higher level of data security and customization. On-premise solutions allow these businesses to tailor the software to their unique needs, ensuring it integrates seamlessly with existing systems and processes. Additionally, large enterprises typically have the resources to manage and maintain on-premise solutions, including dedicated IT teams and infrastructure. However, cloud-based solutions are also gaining traction among large enterprises, particularly those with distributed or remote workforces. The flexibility and accessibility of cloud-based auto dialer software make it an attractive option for large enterprises looking to support remote teams or expand their operations across multiple locations. Cloud-based solutions also offer the advantage of regular updates and technical support from the service provider, reducing the burden on internal IT teams. Both SMEs and large enterprises benefit from the advanced features offered by modern auto dialer software, such as predictive dialing, call recording, and analytics. Predictive dialing uses algorithms to optimize the dialing process, ensuring that agents spend more time talking to customers and less time waiting for calls to connect. Call recording allows businesses to monitor and review interactions for quality assurance and training purposes. Analytics provide valuable insights into call performance, helping businesses identify trends, measure success, and make data-driven decisions. These features are essential for improving efficiency, enhancing customer service, and driving business growth. In conclusion, the usage of Global Enterprise Auto Dialer Software Market varies based on the size and needs of the business. SMEs benefit from the cost-effectiveness and scalability of cloud-based solutions, while large enterprises may prefer the control and customization offered by on-premise solutions. Both types of businesses can leverage the advanced features of auto dialer software to improve efficiency, enhance customer interactions, and drive growth. As the market continues to evolve, businesses of all sizes will need to carefully consider their specific requirements and choose the deployment model that best aligns with their operational goals.

Global Enterprise Auto Dialer Software Market Outlook:

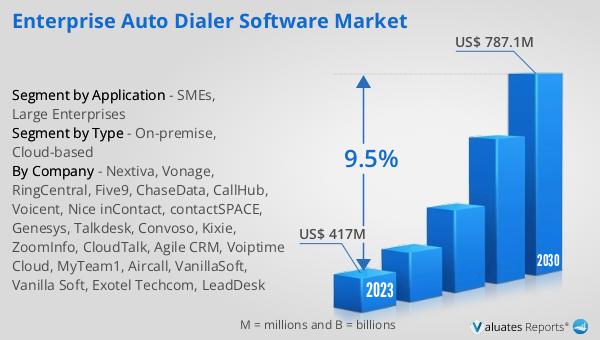

The global Enterprise Auto Dialer Software market was valued at US$ 417 million in 2023 and is anticipated to reach US$ 787.1 million by 2030, witnessing a compound annual growth rate (CAGR) of 9.5% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for efficient communication tools and the adoption of advanced technologies by businesses worldwide. The market's expansion is driven by the need for businesses to streamline their operations, improve customer service, and enhance productivity. Auto dialer software plays a crucial role in achieving these objectives by automating the dialing process, reducing manual effort, and allowing agents to focus on meaningful customer interactions. The projected growth also highlights the rising popularity of cloud-based solutions, which offer cost-effectiveness, scalability, and flexibility, making them an attractive option for businesses of all sizes. As the market continues to grow, businesses will need to stay abreast of the latest trends and innovations to remain competitive and leverage the full potential of auto dialer software.

| Report Metric | Details |

| Report Name | Enterprise Auto Dialer Software Market |

| Accounted market size in 2023 | US$ 417 million |

| Forecasted market size in 2030 | US$ 787.1 million |

| CAGR | 9.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Nextiva, Vonage, RingCentral, Five9, ChaseData, CallHub, Voicent, Nice inContact, contactSPACE, Genesys, Talkdesk, Convoso, Kixie, ZoomInfo, CloudTalk, Agile CRM, Voiptime Cloud, MyTeam1, Aircall, VanillaSoft, Vanilla Soft, Exotel Techcom, LeadDesk |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |