What is Global Semiconductor Supply Chains Market?

The Global Semiconductor Supply Chains Market is a complex and vital network that ensures the production and distribution of semiconductors, which are essential components in modern electronics. This market encompasses various stages, from the initial design of semiconductor chips to their final assembly and packaging. The supply chain involves multiple players, including raw material suppliers, equipment manufacturers, chip designers, and fabrication plants. These entities work together to produce semiconductors that power a wide range of devices, from smartphones and computers to cars and industrial machinery. The global nature of this supply chain means that disruptions in one part of the world can have significant impacts elsewhere, highlighting the importance of coordination and resilience in this market. As technology continues to advance, the demand for semiconductors is expected to grow, making the efficiency and reliability of the global semiconductor supply chain more crucial than ever.

Semiconductor Design, Wafer Fabrication, Semiconductor Assembly, Test, and Packaging, Semiconductor Equipment, Semiconductor Materials in the Global Semiconductor Supply Chains Market:

Semiconductor design is the first step in the semiconductor supply chain, involving the creation of the blueprint for the chip. This process requires significant expertise and innovation, as designers must create chips that meet specific performance criteria while minimizing power consumption and cost. Once the design is complete, the next step is wafer fabrication. This involves the production of semiconductor wafers, which are thin slices of semiconductor material, typically silicon. These wafers are then processed to create the integrated circuits that make up the chip. The fabrication process is highly complex and requires advanced equipment and cleanroom environments to ensure the purity and precision of the wafers. After fabrication, the wafers are sent to semiconductor assembly, test, and packaging facilities. Here, the individual chips are cut from the wafers, assembled into their final form, and tested for functionality. Packaging is also a critical step, as it protects the chips from physical damage and environmental factors. Semiconductor equipment refers to the machinery and tools used in the various stages of semiconductor production, from design and fabrication to assembly and testing. This equipment is highly specialized and often represents a significant investment for semiconductor manufacturers. Semiconductor materials, on the other hand, include the raw materials used to produce semiconductors, such as silicon, as well as the chemicals and gases used in the fabrication process. The global semiconductor supply chain relies on a steady supply of these materials to maintain production levels and meet the growing demand for semiconductors.

Communication, Computer/PC, Consumer, Automotive, Industrial, Others in the Global Semiconductor Supply Chains Market:

The Global Semiconductor Supply Chains Market plays a crucial role in various sectors, including communication, computers/PCs, consumer electronics, automotive, industrial, and others. In the communication sector, semiconductors are essential for the functioning of devices such as smartphones, tablets, and networking equipment. These devices rely on semiconductors for processing power, connectivity, and data storage, making them indispensable in our connected world. In the computer/PC sector, semiconductors are the backbone of all computing devices, from desktops and laptops to servers and data centers. They enable the processing and storage of vast amounts of data, driving advancements in fields such as artificial intelligence, cloud computing, and big data analytics. Consumer electronics, such as televisions, gaming consoles, and home appliances, also depend on semiconductors for their operation. These devices require semiconductors for functions such as display, audio processing, and connectivity, enhancing the user experience and driving innovation in the consumer market. In the automotive sector, semiconductors are increasingly important as vehicles become more advanced and connected. They are used in various applications, including engine control units, infotainment systems, and advanced driver-assistance systems (ADAS), contributing to the development of safer and more efficient vehicles. The industrial sector also relies on semiconductors for automation, control systems, and robotics, which are essential for modern manufacturing processes. Finally, other sectors, such as healthcare and aerospace, also benefit from the advancements in semiconductor technology, enabling the development of sophisticated medical devices and advanced avionics systems.

Global Semiconductor Supply Chains Market Outlook:

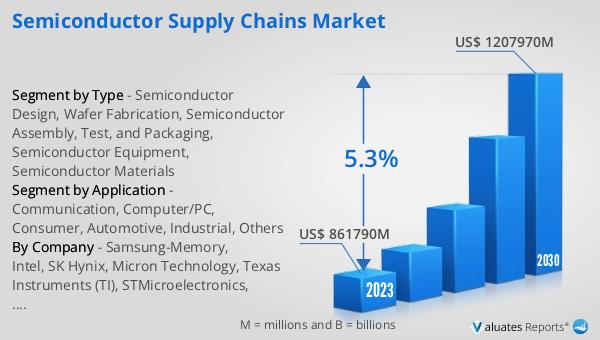

The global Semiconductor Supply Chains market was valued at $861.79 billion in 2023 and is projected to reach $1.21 trillion by 2030, reflecting a compound annual growth rate (CAGR) of 5.3% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for semiconductors across various industries, including communication, computing, consumer electronics, automotive, and industrial sectors. As technology continues to evolve, the need for more advanced and efficient semiconductors is expected to rise, further fueling the market's expansion. The semiconductor supply chain's complexity and global nature highlight the importance of collaboration and innovation among industry players to meet the growing demand and address potential challenges. The market's growth also underscores the critical role of semiconductors in driving technological advancements and supporting the development of new and emerging technologies.

| Report Metric | Details |

| Report Name | Semiconductor Supply Chains Market |

| Accounted market size in 2023 | US$ 861790 million |

| Forecasted market size in 2030 | US$ 1207970 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Samsung-Memory, Intel, SK Hynix, Micron Technology, Texas Instruments (TI), STMicroelectronics, Kioxia, Sony Semiconductor Solutions Corporation (SSS), Infineon, NXP, Analog Devices, Inc. (ADI), Renesas Electronics, Microchip Technology, Onsemi, NVIDIA, Qualcomm, Broadcom, Advanced Micro Devices, Inc. (AMD), MediaTek, Marvell Technology Group, Novatek Microelectronics Corp., Tsinghua Unigroup, Realtek Semiconductor Corporation, OmniVision Technology, Inc, Monolithic Power Systems, Inc. (MPS), Cirrus Logic, Inc., Socionext Inc., LX Semicon, HiSilicon Technologies, TSMC, Samsung Foundry, GlobalFoundries, United Microelectronics Corporation (UMC), SMIC, Tower Semiconductor, PSMC, VIS (Vanguard International Semiconductor), Hua Hong Semiconductor, HLMC, ASE (SPIL), Amkor, JCET (STATS ChipPAC), Tongfu Microelectronics (TFME), Powertech Technology Inc. (PTI), Carsem, King Yuan Electronics Corp. (KYEC), KINGPAK Technology Inc, SFA Semicon, Unisem Group, Applied Materials, Inc. (AMAT), ASML, TEL (Tokyo Electron Ltd.), Lam Research, KLA, Nikon, Canon, Advantest, Teradyne, ASM International, SEMES |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |