What is Global Cables for Semiconductor & Display Equipment Market?

The Global Cables for Semiconductor & Display Equipment Market refers to the industry that manufactures and supplies cables specifically designed for use in semiconductor and display equipment. These cables are crucial components in the production and operation of semiconductor devices and display technologies, such as LCDs, LEDs, and OLEDs. The market encompasses a wide range of cable types, including power cables, data cables, and signal cables, each tailored to meet the stringent requirements of high-performance and high-reliability applications. The demand for these cables is driven by the rapid advancements in semiconductor technology and the growing adoption of advanced display technologies in various consumer electronics, industrial, and automotive applications. As the semiconductor and display industries continue to evolve, the need for specialized cables that can support higher data rates, increased power efficiency, and enhanced durability becomes increasingly important. This market is characterized by continuous innovation, with manufacturers investing in research and development to create cables that can meet the ever-changing demands of the industry.

Unshielded, Foil Shielded, Braid Shielded, Foil+ Braid Shielded in the Global Cables for Semiconductor & Display Equipment Market:

In the Global Cables for Semiconductor & Display Equipment Market, there are several types of shielding techniques used to protect cables from electromagnetic interference (EMI) and ensure signal integrity. Unshielded cables are the most basic type, lacking any form of shielding. They are typically used in environments where EMI is minimal and cost is a primary concern. These cables are lightweight and flexible, making them easy to install, but they are susceptible to interference, which can degrade signal quality. Foil shielded cables, on the other hand, use a thin layer of aluminum or copper foil to encase the cable's conductors. This type of shielding provides a good level of protection against EMI and is commonly used in applications where moderate interference is expected. Foil shielding is relatively inexpensive and offers a compact design, but it can be less durable than other shielding methods. Braid shielded cables employ a woven mesh of copper or aluminum strands to encase the conductors. This type of shielding is highly effective at blocking EMI and is often used in environments with high levels of interference. Braid shielding is more robust and durable than foil shielding, but it can be bulkier and more expensive. Finally, foil+braid shielded cables combine both foil and braid shielding techniques to offer superior protection against EMI. These cables are designed for use in the most demanding environments, where maximum signal integrity is required. The combination of foil and braid shielding provides a high level of durability and flexibility, making these cables suitable for a wide range of applications in the semiconductor and display equipment industries. Each type of shielding has its own advantages and trade-offs, and the choice of shielding depends on the specific requirements of the application, including the level of EMI, cost considerations, and physical constraints.

Cables for Semiconductor Equipment, Cables for Display Equipment in the Global Cables for Semiconductor & Display Equipment Market:

The usage of Global Cables for Semiconductor & Display Equipment Market can be broadly categorized into two main areas: cables for semiconductor equipment and cables for display equipment. Cables for semiconductor equipment are essential for the operation of various machines and tools used in the fabrication of semiconductor devices. These cables are designed to handle high-speed data transmission, power delivery, and signal integrity in harsh manufacturing environments. They are used in equipment such as wafer processing machines, photolithography systems, and testing and inspection tools. The cables must be able to withstand high temperatures, chemical exposure, and mechanical stress while maintaining reliable performance. In addition, they need to support the precise and accurate transmission of signals required for the intricate processes involved in semiconductor manufacturing. On the other hand, cables for display equipment are used in the production and operation of various display technologies, including LCDs, LEDs, and OLEDs. These cables are responsible for transmitting video signals, power, and control signals between different components of the display system. They are used in equipment such as panel assembly machines, inspection systems, and testing tools. The cables must be able to support high-resolution video transmission, fast refresh rates, and low latency to ensure optimal display performance. They also need to be flexible and durable to accommodate the dynamic movements and mechanical stresses involved in the assembly and operation of display equipment. Both types of cables play a crucial role in ensuring the efficient and reliable operation of semiconductor and display equipment, contributing to the overall performance and quality of the final products.

Global Cables for Semiconductor & Display Equipment Market Outlook:

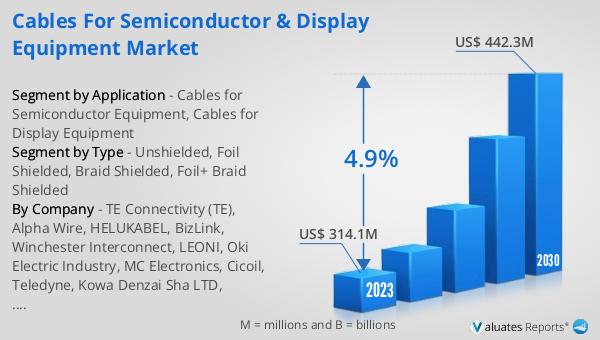

The global Cables for Semiconductor & Display Equipment market was valued at US$ 314.1 million in 2023 and is anticipated to reach US$ 442.3 million by 2030, witnessing a CAGR of 4.9% during the forecast period 2024-2030. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased 5% from $102.6 billion in 2021 to an all-time record of $107.6 billion in 2022. For the third consecutive year, China remained the largest semiconductor equipment market in 2022, despite a 5% slowdown in the pace of investments in the region year over year, accounting for $28.3 billion in billings.

| Report Metric | Details |

| Report Name | Cables for Semiconductor & Display Equipment Market |

| Accounted market size in 2023 | US$ 314.1 million |

| Forecasted market size in 2030 | US$ 442.3 million |

| CAGR | 4.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TE Connectivity (TE), Alpha Wire, HELUKABEL, BizLink, Winchester Interconnect, LEONI, Oki Electric Industry, MC Electronics, Cicoil, Teledyne, Kowa Denzai Sha LTD, CHUGOKU ELECTRIC WIRE & CABLE CO.,LTD., Prysmian, Nexans, LS Cable & System, TF Kable, W. L. Gore & Associates, TOTOKU INC., SAB, Daiichi Denzai (DID), NICHIGOH COMMUNICATION ELECTRIC WIRE CO.,LTD. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |