What is Global Automotive Semiconductor Packaging Market?

The Global Automotive Semiconductor Packaging Market refers to the industry focused on the development and production of packaging solutions for semiconductor components used in automotive applications. These semiconductor components are essential for various automotive systems, including engine control units, infotainment systems, advanced driver-assistance systems (ADAS), and electric vehicle powertrains. Packaging in this context involves enclosing semiconductor devices in protective materials to ensure their reliability, performance, and longevity under harsh automotive conditions. The market encompasses a wide range of packaging technologies, from traditional methods like lead frames and wire bonding to advanced techniques such as flip-chip and wafer-level packaging. The growth of this market is driven by the increasing demand for advanced automotive electronics, the rise of electric and autonomous vehicles, and the need for more efficient and reliable semiconductor solutions in the automotive industry.

Advanced Packaging for Automotive, Traditional Packaging for Automotive in the Global Automotive Semiconductor Packaging Market:

Advanced Packaging for Automotive refers to the use of cutting-edge technologies to encapsulate semiconductor devices, ensuring they meet the stringent requirements of modern automotive applications. This includes techniques like flip-chip packaging, where the semiconductor die is flipped and bonded directly to the substrate, providing better electrical performance and heat dissipation. Another advanced method is wafer-level packaging, which involves packaging the semiconductor at the wafer level before it is diced into individual chips. This approach offers benefits such as reduced size, improved performance, and lower production costs. Advanced packaging is crucial for applications that require high reliability and performance, such as ADAS, electric vehicle powertrains, and infotainment systems. On the other hand, Traditional Packaging for Automotive involves more conventional methods like lead frames and wire bonding. Lead frames are metal structures that provide mechanical support and electrical connections for the semiconductor die. Wire bonding, the process of connecting the semiconductor die to the lead frame using fine wires, is another traditional technique. While these methods are well-established and cost-effective, they may not offer the same level of performance and miniaturization as advanced packaging techniques. However, they are still widely used in applications where cost is a significant factor, and the performance requirements are less stringent. Both advanced and traditional packaging methods play a vital role in the Global Automotive Semiconductor Packaging Market, catering to different segments of the automotive industry based on their specific needs and requirements.

Automotive OSAT, Automotive IDM in the Global Automotive Semiconductor Packaging Market:

The usage of Global Automotive Semiconductor Packaging Market in areas like Automotive OSAT (Outsourced Semiconductor Assembly and Test) and Automotive IDM (Integrated Device Manufacturer) is crucial for the industry's growth and innovation. Automotive OSAT companies specialize in providing packaging and testing services for semiconductor manufacturers. They play a vital role in the supply chain by offering advanced packaging solutions, such as flip-chip and wafer-level packaging, which are essential for high-performance automotive applications. OSAT companies help semiconductor manufacturers meet the stringent quality and reliability standards required in the automotive industry. They also provide flexibility and scalability, allowing manufacturers to focus on their core competencies while outsourcing the packaging and testing processes. On the other hand, Automotive IDM companies are vertically integrated firms that handle the entire semiconductor manufacturing process, from design and fabrication to packaging and testing. These companies have the advantage of controlling the entire supply chain, ensuring high-quality and reliable semiconductor solutions for automotive applications. IDMs often invest in advanced packaging technologies to enhance the performance and reliability of their products. They also benefit from economies of scale, as they can produce large volumes of semiconductor devices in-house. Both OSAT and IDM companies contribute significantly to the Global Automotive Semiconductor Packaging Market by providing innovative packaging solutions that meet the evolving demands of the automotive industry.

Global Automotive Semiconductor Packaging Market Outlook:

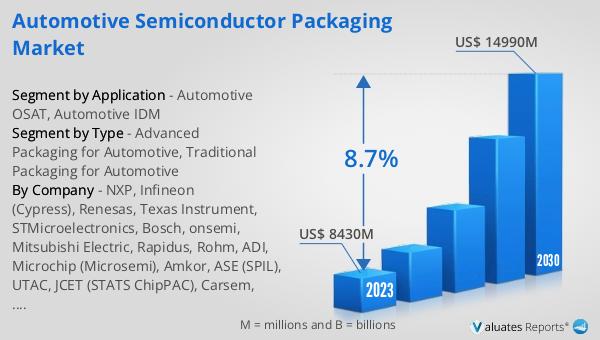

The global Automotive Semiconductor Packaging market was valued at US$ 8430 million in 2023 and is anticipated to reach US$ 14990 million by 2030, witnessing a CAGR of 8.7% during the forecast period 2024-2030. This market growth is driven by the increasing demand for advanced automotive electronics, the rise of electric and autonomous vehicles, and the need for more efficient and reliable semiconductor solutions in the automotive industry. The market encompasses a wide range of packaging technologies, from traditional methods like lead frames and wire bonding to advanced techniques such as flip-chip and wafer-level packaging. The growth of this market is driven by the increasing demand for advanced automotive electronics, the rise of electric and autonomous vehicles, and the need for more efficient and reliable semiconductor solutions in the automotive industry. The market encompasses a wide range of packaging technologies, from traditional methods like lead frames and wire bonding to advanced techniques such as flip-chip and wafer-level packaging.

| Report Metric | Details |

| Report Name | Automotive Semiconductor Packaging Market |

| Accounted market size in 2023 | US$ 8430 million |

| Forecasted market size in 2030 | US$ 14990 million |

| CAGR | 8.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | NXP, Infineon (Cypress), Renesas, Texas Instrument, STMicroelectronics, Bosch, onsemi, Mitsubishi Electric, Rapidus, Rohm, ADI, Microchip (Microsemi), Amkor, ASE (SPIL), UTAC, JCET (STATS ChipPAC), Carsem, King Yuan Electronics Corp. (KYEC), KINGPAK Technology Inc, Powertech Technology Inc. (PTI), SFA Semicon, Unisem Group, Chipbond Technology Corporation, ChipMOS TECHNOLOGIES, OSE CORP., Sigurd Microelectronics, Natronix Semiconductor Technology, Nepes, KESM Industries Berhad, Forehope Electronic (Ningbo) Co.,Ltd., Union Semiconductor(Hefei)Co., Ltd., Tongfu Microelectronics (TFME), Hefei Chipmore Technology Co.,Ltd., HT-tech, China Wafer Level CSP Co., Ltd, Ningbo ChipEx Semiconductor Co., Ltd, Guangdong Leadyo IC Testing, Unimos Microelectronics (Shanghai), Sino Technology, Taiji Semiconductor (Suzhou) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |