What is Global GLP-1 Drug Market?

The Global GLP-1 Drug Market refers to the worldwide market for drugs that target the glucagon-like peptide-1 (GLP-1) receptor. GLP-1 is a hormone that plays a crucial role in regulating blood sugar levels by enhancing insulin secretion, inhibiting glucagon release, and slowing gastric emptying. These drugs are primarily used in the treatment of Type 2 Diabetes Mellitus (T2DM) but have also shown promise in addressing other conditions such as obesity, cardiovascular diseases, and even Alzheimer's disease. The market for GLP-1 drugs has been expanding rapidly due to the increasing prevalence of diabetes and obesity, coupled with advancements in drug formulations and delivery mechanisms. Pharmaceutical companies are investing heavily in research and development to create more effective and longer-lasting GLP-1 drugs, which has led to a surge in new product launches and approvals. The global GLP-1 drug market is characterized by intense competition among key players, each striving to gain a larger market share through innovation and strategic partnerships.

Short-acting GLP-1 Drug, Long-acting GLP-1 Drug in the Global GLP-1 Drug Market:

Short-acting GLP-1 drugs and long-acting GLP-1 drugs are two primary categories within the Global GLP-1 Drug Market, each with distinct characteristics and applications. Short-acting GLP-1 drugs, such as exenatide and lixisenatide, are designed to be administered multiple times a day or once daily. These drugs have a rapid onset of action and are particularly effective in controlling postprandial blood glucose levels, which are the spikes in blood sugar that occur after meals. Short-acting GLP-1 drugs work by mimicking the natural incretin hormones that the body releases in response to food intake, thereby enhancing insulin secretion and inhibiting glucagon release. They also slow down gastric emptying, which helps to reduce appetite and promote weight loss. On the other hand, long-acting GLP-1 drugs, such as liraglutide, dulaglutide, and semaglutide, are designed to be administered less frequently, ranging from once a week to once a month. These drugs have a prolonged duration of action, which provides more consistent blood glucose control over an extended period. Long-acting GLP-1 drugs are particularly beneficial for patients who have difficulty adhering to a daily medication regimen, as they offer the convenience of less frequent dosing. Additionally, long-acting GLP-1 drugs have been shown to provide significant cardiovascular benefits, including reduced risk of major adverse cardiovascular events such as heart attack and stroke. Both short-acting and long-acting GLP-1 drugs have their unique advantages and are chosen based on the specific needs and preferences of the patient. The development of these drugs has been driven by extensive research and clinical trials, which have demonstrated their efficacy and safety in managing Type 2 Diabetes Mellitus and other related conditions. As the Global GLP-1 Drug Market continues to grow, it is expected that new formulations and delivery methods will be introduced, further enhancing the therapeutic options available to patients.

Obesity, Type 2 Diabetes (T2DM), Cardiovascular and Cerebrovascular Diseases (CVD), Non-alcoholic Steatohepatitis (NASH), Alzheimer's Disease (AD) in the Global GLP-1 Drug Market:

The usage of GLP-1 drugs in the Global GLP-1 Drug Market extends beyond Type 2 Diabetes Mellitus (T2DM) to include several other medical conditions such as obesity, cardiovascular and cerebrovascular diseases (CVD), non-alcoholic steatohepatitis (NASH), and Alzheimer's disease (AD). In the context of obesity, GLP-1 drugs have been found to be highly effective in promoting weight loss. These drugs work by slowing gastric emptying and increasing feelings of satiety, which helps to reduce overall calorie intake. Clinical studies have shown that patients treated with GLP-1 drugs experience significant weight loss compared to those on placebo, making these drugs a valuable tool in the management of obesity. In addition to weight loss, GLP-1 drugs have also been shown to improve various metabolic parameters, such as reducing waist circumference and improving lipid profiles. In the realm of cardiovascular and cerebrovascular diseases (CVD), GLP-1 drugs have demonstrated substantial benefits. Several large-scale clinical trials have shown that GLP-1 drugs can reduce the risk of major adverse cardiovascular events, including heart attack, stroke, and cardiovascular death. These benefits are thought to be mediated through multiple mechanisms, including improved glycemic control, weight loss, and direct effects on the cardiovascular system. For patients with non-alcoholic steatohepatitis (NASH), a condition characterized by liver inflammation and damage due to fat accumulation, GLP-1 drugs have shown promise in reducing liver fat content and improving liver function. This is particularly important as NASH can progress to more severe liver diseases such as cirrhosis and liver cancer. Lastly, emerging research suggests that GLP-1 drugs may have potential benefits in the treatment of Alzheimer's disease (AD). Preclinical studies have indicated that GLP-1 drugs can cross the blood-brain barrier and exert neuroprotective effects, potentially slowing the progression of neurodegenerative diseases. While more research is needed to fully understand the impact of GLP-1 drugs on Alzheimer's disease, these preliminary findings are encouraging and highlight the broad therapeutic potential of GLP-1 drugs in various medical conditions.

Global GLP-1 Drug Market Outlook:

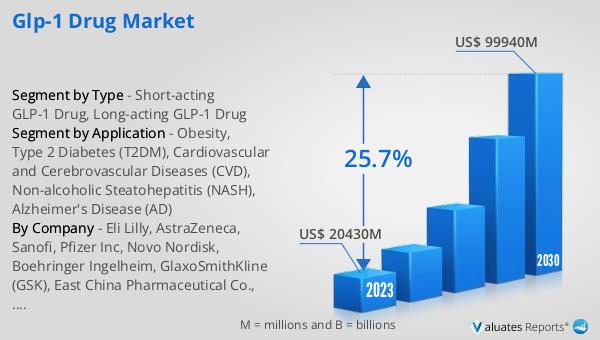

The global GLP-1 drug market was valued at approximately $20.43 billion in 2023 and is projected to reach around $99.94 billion by 2030, reflecting a compound annual growth rate (CAGR) of 25.7% during the forecast period from 2024 to 2030. This significant growth is driven by several factors, including the rising prevalence of Type 2 Diabetes Mellitus (T2DM) and obesity, which are major public health concerns worldwide. The increasing awareness about the benefits of GLP-1 drugs in managing these conditions, coupled with advancements in drug formulations and delivery mechanisms, has further fueled market expansion. Pharmaceutical companies are investing heavily in research and development to create more effective and longer-lasting GLP-1 drugs, leading to a surge in new product launches and approvals. Additionally, the growing recognition of the cardiovascular benefits associated with GLP-1 drugs has contributed to their increased adoption among patients and healthcare providers. The competitive landscape of the global GLP-1 drug market is characterized by intense competition among key players, each striving to gain a larger market share through innovation and strategic partnerships. As the market continues to evolve, it is expected that new formulations and delivery methods will be introduced, further enhancing the therapeutic options available to patients and driving market growth.

| Report Metric | Details |

| Report Name | GLP-1 Drug Market |

| Accounted market size in 2023 | US$ 20430 million |

| Forecasted market size in 2030 | US$ 99940 million |

| CAGR | 25.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Eli Lilly, AstraZeneca, Sanofi, Pfizer Inc, Novo Nordisk, Boehringer Ingelheim, GlaxoSmithKline (GSK), East China Pharmaceutical Co., Ltd., Gan & Lee Pharmaceuticals, Tonghua Dongbao, Shanghai Renhui Biopharmaceutical Co., Ltd., Jiangsu Hansoh Pharmaceutical Group Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |