What is Global SPL Meter Market?

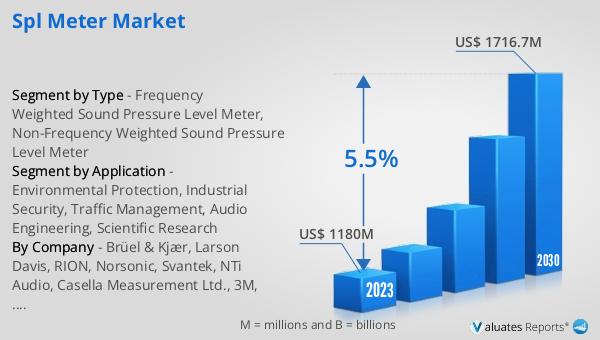

The global SPL (Sound Pressure Level) Meter market is a specialized segment within the broader field of acoustic measurement devices. SPL meters are instruments designed to measure the sound pressure level in decibels (dB), which is a logarithmic unit used to quantify sound intensity. These devices are crucial for various applications, including environmental noise monitoring, industrial noise control, and audio engineering. The market for SPL meters is driven by increasing awareness about noise pollution and its adverse effects on human health, as well as stringent regulations imposed by governments and environmental agencies. Technological advancements have also played a significant role in the market's growth, with modern SPL meters offering features like data logging, real-time monitoring, and wireless connectivity. The global SPL meter market was valued at US$ 1180 million in 2023 and is anticipated to reach US$ 1716.7 million by 2030, witnessing a CAGR of 5.5% during the forecast period 2024-2030. This growth can be attributed to the rising demand for accurate and reliable noise measurement tools across various sectors.

Frequency Weighted Sound Pressure Level Meter, Non-Frequency Weighted Sound Pressure Level Meter in the Global SPL Meter Market:

Frequency Weighted Sound Pressure Level Meters and Non-Frequency Weighted Sound Pressure Level Meters are two primary categories within the global SPL meter market. Frequency Weighted SPL Meters are designed to measure sound levels while taking into account the frequency of the sound. These meters use weighting filters like A-weighting, C-weighting, and Z-weighting to mimic the human ear's response to different frequencies. A-weighting is the most commonly used filter and is designed to reflect the sensitivity of human hearing, which is less sensitive to very low and very high frequencies. C-weighting is used for measuring peak sound levels and is more linear across the frequency spectrum, while Z-weighting is a flat response with no frequency weighting. These meters are essential in applications where the frequency content of the noise is a critical factor, such as in environmental noise assessments, workplace noise evaluations, and product noise testing. On the other hand, Non-Frequency Weighted SPL Meters measure the overall sound pressure level without considering the frequency of the sound. These meters provide a straightforward measurement of the total sound energy and are often used in applications where the frequency content is not as important, such as in basic noise surveys and general noise monitoring. Both types of SPL meters have their unique advantages and are chosen based on the specific requirements of the measurement task. The global market for these devices is expanding as industries and regulatory bodies increasingly recognize the importance of accurate noise measurement in protecting human health and ensuring compliance with noise regulations.

Environmental Protection, Industrial Security, Traffic Management, Audio Engineering, Scientific Research in the Global SPL Meter Market:

The usage of SPL meters spans across various critical areas, including Environmental Protection, Industrial Security, Traffic Management, Audio Engineering, and Scientific Research. In Environmental Protection, SPL meters are used to monitor and control noise pollution, which is a significant environmental concern. These devices help in assessing the impact of noise on communities and wildlife, ensuring compliance with noise regulations, and implementing noise mitigation measures. In Industrial Security, SPL meters play a crucial role in monitoring workplace noise levels to protect workers from hearing loss and other health issues caused by excessive noise exposure. They are used to conduct noise assessments, develop hearing conservation programs, and ensure compliance with occupational noise standards. In Traffic Management, SPL meters are used to measure and analyze traffic noise, which is a major source of urban noise pollution. These measurements help in designing noise barriers, implementing traffic noise control measures, and improving urban planning to reduce noise impact on residents. In Audio Engineering, SPL meters are essential tools for sound engineers and technicians to ensure optimal sound quality in various settings, including recording studios, concert halls, and public address systems. They help in calibrating audio equipment, setting appropriate sound levels, and maintaining sound quality standards. In Scientific Research, SPL meters are used in various studies related to acoustics, noise pollution, and human health. Researchers use these devices to collect accurate noise data, analyze noise patterns, and study the effects of noise on human health and behavior. The versatility and accuracy of SPL meters make them indispensable tools in these diverse fields, contributing to better noise management and improved quality of life.

Global SPL Meter Market Outlook:

The global SPL Meter market was valued at US$ 1180 million in 2023 and is projected to reach US$ 1716.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2024 to 2030. This growth trajectory underscores the increasing demand for SPL meters across various sectors, driven by heightened awareness of noise pollution and its detrimental effects on health and well-being. The market's expansion is also fueled by stringent regulatory frameworks that mandate noise monitoring and control in industrial, environmental, and urban settings. Technological advancements in SPL meters, such as enhanced accuracy, real-time data logging, and wireless connectivity, are further propelling market growth. These innovations make SPL meters more user-friendly and efficient, thereby broadening their application scope. The rising adoption of SPL meters in emerging economies, coupled with the growing emphasis on sustainable development and environmental protection, is expected to sustain the market's upward momentum. As industries and governments continue to prioritize noise management, the demand for reliable and precise SPL meters is set to increase, making them an essential tool in various noise-sensitive applications.

| Report Metric | Details |

| Report Name | SPL Meter Market |

| Accounted market size in 2023 | US$ 1180 million |

| Forecasted market size in 2030 | US$ 1716.7 million |

| CAGR | 5.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Brüel & Kjær, Larson Davis, RION, Norsonic, Svantek, NTi Audio, Casella Measurement Ltd., 3M, Cirrus Research, Testo, TES Electrical Electronic Corp., Extech Instruments, Delta OHM, PCE Instruments, CESVA Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |