What is Global Remotely Operated Vehicle (ROV) Profiling Sonar Market?

The Global Remotely Operated Vehicle (ROV) Profiling Sonar Market is a specialized segment within the broader marine technology industry. ROVs are underwater robots that are controlled remotely, often used for deep-sea exploration, underwater inspections, and various industrial applications. Profiling sonar is a key component of these ROVs, enabling them to create detailed maps and profiles of underwater environments. This technology is crucial for tasks such as pipeline inspections, underwater construction, and marine research. The market for ROV profiling sonar is driven by the increasing demand for underwater exploration and the need for precise underwater mapping. With advancements in sonar technology, these systems are becoming more efficient and capable, further fueling their adoption across various industries. The market is characterized by a mix of established players and emerging companies, all striving to innovate and offer more advanced and reliable sonar systems.

2D Imaging, 3D Imaging in the Global Remotely Operated Vehicle (ROV) Profiling Sonar Market:

2D imaging and 3D imaging are two critical technologies in the Global Remotely Operated Vehicle (ROV) Profiling Sonar Market. 2D imaging involves capturing flat, two-dimensional images of underwater environments. This type of imaging is useful for basic mapping and inspection tasks, providing a straightforward view of the underwater terrain. It is often used in applications where detailed depth information is not required, such as in shallow water surveys or for quick inspections. 2D imaging systems are generally more affordable and easier to deploy, making them a popular choice for many users. On the other hand, 3D imaging provides a more comprehensive view by capturing three-dimensional data. This allows for the creation of detailed, volumetric maps of underwater environments, which are essential for more complex tasks such as underwater construction, archaeological surveys, and detailed inspections of underwater structures. 3D imaging systems use advanced sonar technology to measure the distance and shape of objects, creating a more accurate and detailed representation of the underwater world. These systems are typically more expensive and require more sophisticated equipment and expertise to operate. However, the benefits of 3D imaging, such as improved accuracy and the ability to visualize complex underwater structures, make them invaluable for certain applications. The choice between 2D and 3D imaging depends on the specific needs of the task at hand. For example, in the oil and gas industry, 3D imaging is often preferred for inspecting underwater pipelines and structures, as it provides a more detailed view that can help identify potential issues. In contrast, 2D imaging might be sufficient for routine inspections or for mapping large areas where detailed depth information is not as critical. Both 2D and 3D imaging technologies are continually evolving, with ongoing advancements in sonar technology leading to improved resolution, accuracy, and ease of use. As a result, the Global ROV Profiling Sonar Market is seeing increased adoption of both types of imaging systems, with users selecting the technology that best meets their specific needs. The integration of these imaging systems with other technologies, such as GPS and data analytics, is also enhancing their capabilities and expanding their range of applications. Overall, 2D and 3D imaging are both essential components of the ROV profiling sonar market, each offering unique benefits and serving different purposes. As technology continues to advance, we can expect to see even more innovative and capable imaging systems being developed, further driving the growth and evolution of this market.

National Defense and Millitary, Energy, Transpotation, Others in the Global Remotely Operated Vehicle (ROV) Profiling Sonar Market:

The Global Remotely Operated Vehicle (ROV) Profiling Sonar Market finds extensive usage across various sectors, including National Defense and Military, Energy, Transportation, and others. In the realm of National Defense and Military, ROV profiling sonar systems are indispensable for underwater surveillance, mine detection, and reconnaissance missions. These systems enable military forces to conduct detailed inspections of underwater environments, identify potential threats, and ensure the safety of naval operations. The ability to create accurate maps and profiles of underwater terrains is crucial for strategic planning and mission execution. In the Energy sector, particularly in the oil and gas industry, ROV profiling sonar systems play a vital role in the inspection and maintenance of underwater pipelines, rigs, and other infrastructure. These systems help in detecting potential issues such as leaks or structural damage, ensuring the integrity and safety of critical assets. The detailed imaging capabilities of ROV profiling sonar systems are also essential for the exploration and development of new underwater resources. In the Transportation sector, these systems are used for the inspection and maintenance of underwater tunnels, bridges, and other infrastructure. They help in identifying potential issues and ensuring the safety and reliability of transportation networks. Additionally, ROV profiling sonar systems are used in the inspection of ship hulls and other maritime structures, contributing to the overall safety and efficiency of maritime operations. Beyond these primary sectors, ROV profiling sonar systems are also used in various other applications, such as underwater archaeology, environmental monitoring, and scientific research. In underwater archaeology, these systems enable researchers to create detailed maps of submerged sites, aiding in the discovery and preservation of historical artifacts. In environmental monitoring, ROV profiling sonar systems help in assessing the health of underwater ecosystems and identifying potential environmental threats. In scientific research, these systems provide valuable data for studying underwater geology, marine biology, and other fields. Overall, the versatility and advanced capabilities of ROV profiling sonar systems make them indispensable tools across a wide range of industries and applications.

Global Remotely Operated Vehicle (ROV) Profiling Sonar Market Outlook:

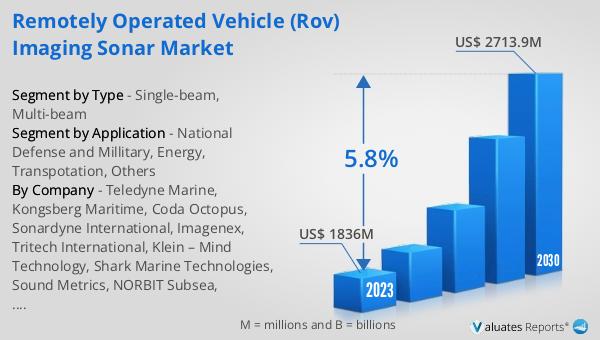

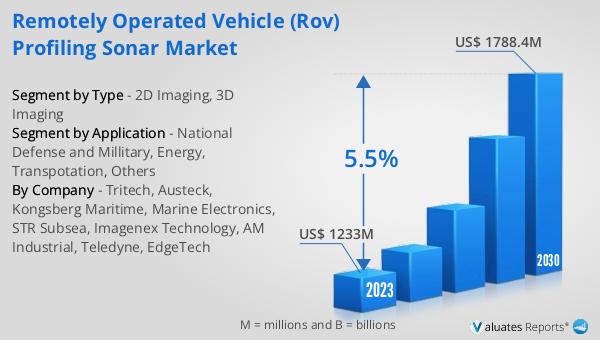

The global market for Remotely Operated Vehicle (ROV) Profiling Sonar was valued at approximately $1,233 million in 2023. Projections indicate that this market is expected to grow significantly, reaching around $1,788.4 million by the year 2030. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2024 to 2030. This upward trend reflects the increasing demand for advanced underwater exploration and mapping technologies across various industries. The market's expansion is driven by the continuous advancements in sonar technology, which enhance the efficiency and capabilities of ROV profiling sonar systems. As industries such as national defense, energy, and transportation increasingly rely on these systems for critical operations, the demand for more sophisticated and reliable sonar solutions is expected to rise. The market is characterized by a mix of established players and emerging companies, all striving to innovate and offer cutting-edge technologies. This competitive landscape is likely to foster further advancements and improvements in ROV profiling sonar systems, contributing to the market's growth. Overall, the global ROV profiling sonar market is poised for substantial growth, driven by technological advancements and the increasing need for precise underwater mapping and inspection solutions.

| Report Metric | Details |

| Report Name | Remotely Operated Vehicle (ROV) Profiling Sonar Market |

| Accounted market size in 2023 | US$ 1233 million |

| Forecasted market size in 2030 | US$ 1788.4 million |

| CAGR | 5.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Tritech, Austeck, Kongsberg Maritime, Marine Electronics, STR Subsea, Imagenex Technology, AM Industrial, Teledyne, EdgeTech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |