What is Global PTFE Gasket for Fuel Cell Market?

The Global PTFE Gasket for Fuel Cell Market is a specialized segment within the broader fuel cell industry. PTFE, or polytetrafluoroethylene, is a high-performance material known for its excellent chemical resistance, low friction, and high-temperature tolerance. These properties make PTFE gaskets ideal for use in fuel cells, which require durable and reliable sealing solutions to maintain efficiency and safety. Fuel cells generate electricity through a chemical reaction between hydrogen and oxygen, and the gaskets play a crucial role in preventing leaks and ensuring the integrity of the cell. The market for PTFE gaskets in fuel cells is driven by the increasing adoption of fuel cell technology in various applications, including transportation, stationary power generation, and portable power devices. As the demand for clean and efficient energy solutions grows, the need for high-quality PTFE gaskets is expected to rise, making this market a key area of interest for manufacturers and investors alike.

Thickness below 0.1 Inches, Thickness above 0.1 Inches in the Global PTFE Gasket for Fuel Cell Market:

When discussing the thickness of PTFE gaskets for fuel cells, it's essential to understand the specific requirements of different applications. Gaskets with a thickness below 0.1 inches are typically used in applications where space is limited, and a thinner gasket can provide the necessary sealing without adding significant bulk. These thinner gaskets are often used in portable fuel cells, where compactness and lightweight design are critical. The thin PTFE gaskets offer excellent sealing properties while maintaining the overall efficiency and performance of the fuel cell. On the other hand, gaskets with a thickness above 0.1 inches are generally used in stationary fuel cells, where the primary concern is durability and long-term performance. Thicker gaskets can withstand higher pressures and temperatures, making them suitable for applications that require robust and reliable sealing solutions. The choice between thin and thick PTFE gaskets depends on various factors, including the specific requirements of the fuel cell, the operating conditions, and the desired performance characteristics. Both types of gaskets play a crucial role in ensuring the efficiency and reliability of fuel cells, and manufacturers must carefully consider these factors when selecting the appropriate gasket for their applications.

Stationary Fuel Cell, Portable Fuel Cell in the Global PTFE Gasket for Fuel Cell Market:

The usage of PTFE gaskets in stationary fuel cells is primarily focused on ensuring long-term reliability and performance. Stationary fuel cells are used in applications such as backup power systems, distributed power generation, and combined heat and power (CHP) systems. These applications require fuel cells to operate continuously for extended periods, often under harsh conditions. PTFE gaskets provide the necessary sealing to prevent leaks and maintain the integrity of the fuel cell, ensuring consistent performance and efficiency. The chemical resistance and high-temperature tolerance of PTFE make it an ideal material for these demanding applications. In portable fuel cells, PTFE gaskets are used to ensure compactness and lightweight design while providing effective sealing. Portable fuel cells are used in various applications, including portable power devices, military equipment, and remote sensing equipment. These applications require fuel cells to be lightweight and compact, making thin PTFE gaskets an ideal choice. The gaskets provide the necessary sealing to prevent leaks and ensure the efficient operation of the fuel cell, while their lightweight design helps to maintain the overall portability of the device. The versatility and performance of PTFE gaskets make them a critical component in both stationary and portable fuel cell applications, ensuring the reliability and efficiency of these advanced energy solutions.

Global PTFE Gasket for Fuel Cell Market Outlook:

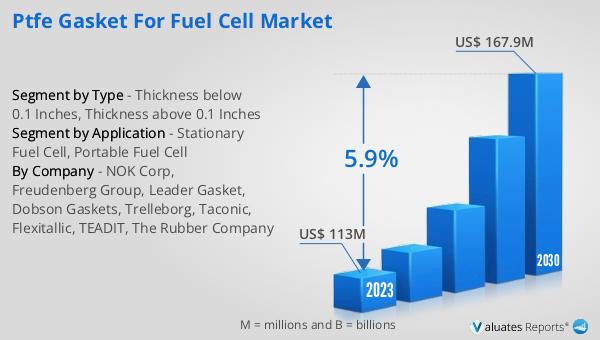

The global PTFE Gasket for Fuel Cell market was valued at US$ 113 million in 2023 and is anticipated to reach US$ 167.9 million by 2030, witnessing a CAGR of 5.9% during the forecast period 2024-2030. This growth is driven by the increasing adoption of fuel cell technology across various industries, including transportation, stationary power generation, and portable power devices. The demand for high-quality PTFE gaskets is expected to rise as more industries seek reliable and efficient sealing solutions for their fuel cell applications. The market outlook indicates a positive trend, with significant opportunities for manufacturers and investors to capitalize on the growing demand for PTFE gaskets in the fuel cell industry. The projected growth reflects the importance of PTFE gaskets in ensuring the efficiency and reliability of fuel cells, making this market a key area of interest for stakeholders in the energy sector.

| Report Metric | Details |

| Report Name | PTFE Gasket for Fuel Cell Market |

| Accounted market size in 2023 | US$ 113 million |

| Forecasted market size in 2030 | US$ 167.9 million |

| CAGR | 5.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | NOK Corp, Freudenberg Group, Leader Gasket, Dobson Gaskets, Trelleborg, Taconic, Flexitallic, TEADIT, The Rubber Company |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |