What is Global Clothing Checkout Software Market?

The Global Clothing Checkout Software Market refers to the industry that develops and provides software solutions specifically designed to streamline the checkout process in clothing retail. This market encompasses a variety of software applications that facilitate transactions, manage inventory, and enhance customer experience both online and in physical stores. These software solutions are crucial for retailers to efficiently handle sales, returns, and exchanges, ensuring a smooth and seamless shopping experience for customers. The market includes a range of products from simple point-of-sale (POS) systems to comprehensive retail management solutions that integrate with other business systems like inventory management, customer relationship management (CRM), and e-commerce platforms. As the retail landscape evolves with increasing consumer expectations for convenience and speed, the demand for advanced checkout software continues to grow. This market is driven by technological advancements, the rise of e-commerce, and the need for retailers to stay competitive by offering efficient and user-friendly checkout processes.

On-Premises, Cloud Computing, Mobile Applications in the Global Clothing Checkout Software Market:

The Global Clothing Checkout Software Market can be categorized based on deployment methods such as On-Premises, Cloud Computing, and Mobile Applications. On-Premises solutions are installed and run on the retailer's own hardware and servers. This traditional approach offers greater control over the software and data security, as everything is managed internally. However, it requires significant upfront investment in hardware and ongoing maintenance costs. Retailers with large operations and specific security needs often prefer On-Premises solutions because they can customize the software to fit their unique requirements. On the other hand, Cloud Computing solutions are hosted on remote servers and accessed via the internet. This model offers several advantages, including lower initial costs, scalability, and ease of updates and maintenance. Retailers can quickly adapt to changing business needs without the need for extensive IT infrastructure. Cloud-based solutions also facilitate better data integration and real-time analytics, enabling retailers to make informed decisions. Mobile Applications represent another significant segment in the Global Clothing Checkout Software Market. These apps are designed to run on smartphones and tablets, providing flexibility and convenience for both retailers and customers. Mobile checkout solutions can be used in-store to assist sales associates, reducing wait times and enhancing the shopping experience. They also support mobile payments, which are increasingly popular among consumers. Additionally, mobile apps can be integrated with loyalty programs and personalized marketing, further driving customer engagement and sales. Each of these deployment methods has its own set of benefits and challenges, and the choice depends on the retailer's specific needs, budget, and strategic goals. As technology continues to evolve, we can expect to see further innovations in how clothing checkout software is deployed and utilized.

Online Platform, Physical Store in the Global Clothing Checkout Software Market:

The usage of Global Clothing Checkout Software Market in online platforms and physical stores varies significantly, yet both aim to enhance the customer experience and streamline operations. In online platforms, checkout software plays a crucial role in ensuring a smooth and secure transaction process. It integrates with e-commerce websites to manage shopping carts, process payments, and handle shipping and returns. Advanced features like one-click checkout, multiple payment options, and automated tax calculations help reduce cart abandonment rates and improve customer satisfaction. Additionally, online checkout software often includes fraud detection and prevention mechanisms to protect both the retailer and the customer. It also provides valuable insights through analytics, helping retailers understand customer behavior and optimize their online sales strategies. In physical stores, checkout software is typically part of a broader point-of-sale (POS) system. These systems not only process transactions but also manage inventory, track sales, and generate reports. Modern POS systems are often integrated with other retail technologies such as barcode scanners, receipt printers, and customer displays. They support various payment methods, including cash, credit/debit cards, and mobile payments, offering convenience to customers. Some advanced POS systems also feature customer relationship management (CRM) capabilities, allowing retailers to collect and analyze customer data to personalize the shopping experience. Mobile POS solutions are becoming increasingly popular in physical stores, enabling sales associates to assist customers and complete transactions anywhere within the store. This flexibility helps reduce wait times and enhances customer service. Overall, whether in online platforms or physical stores, the primary goal of clothing checkout software is to provide a seamless, efficient, and secure shopping experience for customers while helping retailers manage their operations effectively.

Global Clothing Checkout Software Market Outlook:

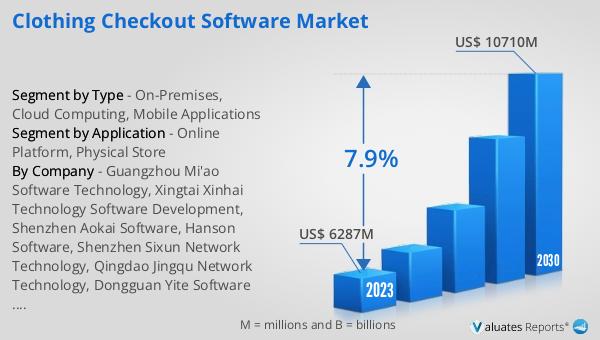

The global Clothing Checkout Software market was valued at US$ 6,287 million in 2023 and is anticipated to reach US$ 10,710 million by 2030, witnessing a CAGR of 7.9% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for advanced checkout solutions in the retail industry. As consumer expectations for convenience and speed continue to rise, retailers are investing in sophisticated software to enhance the shopping experience both online and in physical stores. The market's expansion is driven by technological advancements, the proliferation of e-commerce, and the need for efficient and user-friendly checkout processes. Retailers are seeking solutions that not only streamline transactions but also integrate with other business systems like inventory management and customer relationship management (CRM). The shift towards cloud-based and mobile solutions is also contributing to the market's growth, offering retailers flexibility, scalability, and real-time data insights. As the retail landscape evolves, the demand for innovative and efficient clothing checkout software is expected to continue its upward trajectory.

| Report Metric | Details |

| Report Name | Clothing Checkout Software Market |

| Accounted market size in 2023 | US$ 6287 million |

| Forecasted market size in 2030 | US$ 10710 million |

| CAGR | 7.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Guangzhou Mi'ao Software Technology, Xingtai Xinhai Technology Software Development, Shenzhen Aokai Software, Hanson Software, Shenzhen Sixun Network Technology, Qingdao Jingqu Network Technology, Dongguan Yite Software Development, Shenzhen Qinsilk Technology, Hubei Yunpu Network Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |