What is Global MOSFET for Lithium Battery Protection Market?

The Global MOSFET for Lithium Battery Protection Market is a specialized segment within the broader semiconductor industry, focusing on the use of Metal-Oxide-Semiconductor Field-Effect Transistors (MOSFETs) to safeguard lithium batteries. These batteries are widely used in various electronic devices due to their high energy density and long life cycle. However, they are also prone to issues like overcharging, overheating, and short-circuiting, which can lead to safety hazards. MOSFETs play a crucial role in mitigating these risks by acting as switches that control the flow of electricity within the battery. They ensure that the battery operates within safe parameters, thereby enhancing its reliability and lifespan. The market for these specialized MOSFETs is growing, driven by the increasing demand for lithium batteries in consumer electronics, electric vehicles, and renewable energy storage systems. As technology advances, the need for more efficient and reliable battery protection solutions is becoming increasingly critical, making this market an essential component of the modern electronics landscape.

12V MOSFET, 20V MOSFET, 24V MOSFET, Others in the Global MOSFET for Lithium Battery Protection Market:

In the Global MOSFET for Lithium Battery Protection Market, different voltage ratings of MOSFETs are used to cater to various applications and requirements. The 12V MOSFETs are typically employed in low-power devices where the voltage requirements are minimal. These are commonly found in small electronic gadgets and some types of wearable devices. The 20V MOSFETs, on the other hand, are used in slightly more demanding applications such as tablets and certain types of mobile phones. They offer a balance between power efficiency and protection, ensuring that the devices operate safely without compromising on performance. The 24V MOSFETs are designed for even more demanding applications, often found in high-performance tablets, advanced wearable devices, and some industrial applications. These MOSFETs provide robust protection against overcharging and overheating, making them ideal for devices that require higher power levels. Other voltage ratings, beyond the standard 12V, 20V, and 24V, are also available to meet specific needs in specialized applications. These could include anything from high-end consumer electronics to specialized industrial equipment. Each voltage rating serves a unique purpose, ensuring that the lithium batteries in these devices are adequately protected, thereby enhancing their performance and longevity. The choice of MOSFET voltage rating depends on various factors, including the power requirements of the device, the operating environment, and the specific safety standards that need to be met. As the demand for more efficient and reliable electronic devices continues to grow, the need for specialized MOSFETs in lithium battery protection is also expected to increase. This makes the Global MOSFET for Lithium Battery Protection Market a dynamic and evolving sector, constantly adapting to meet the changing needs of the electronics industry.

Mobile Phones, Tablets, Wearable Devices in the Global MOSFET for Lithium Battery Protection Market:

The usage of Global MOSFETs for Lithium Battery Protection is particularly significant in mobile phones, tablets, and wearable devices. In mobile phones, MOSFETs are essential for managing the battery's charging and discharging cycles. They help prevent overcharging, which can lead to overheating and potential battery failure. By ensuring that the battery operates within safe limits, MOSFETs enhance the phone's overall performance and longevity. In tablets, the role of MOSFETs is equally crucial. Tablets often have larger batteries compared to mobile phones, and they require more robust protection mechanisms. MOSFETs in tablets help manage the higher power demands and ensure that the battery remains safe during intensive usage, such as gaming or video streaming. Wearable devices, such as smartwatches and fitness trackers, also rely heavily on MOSFETs for battery protection. These devices are often used in various environments, including during physical activities, which can put additional stress on the battery. MOSFETs help maintain the battery's integrity by preventing issues like overcharging and short-circuiting, ensuring that the wearable device remains reliable and safe to use. The importance of MOSFETs in these devices cannot be overstated, as they play a critical role in maintaining the safety and efficiency of the battery, which in turn affects the overall performance and user experience of the device. As the demand for mobile phones, tablets, and wearable devices continues to grow, the need for effective battery protection solutions like MOSFETs is also expected to increase, making them an integral part of the modern electronics landscape.

Global MOSFET for Lithium Battery Protection Market Outlook:

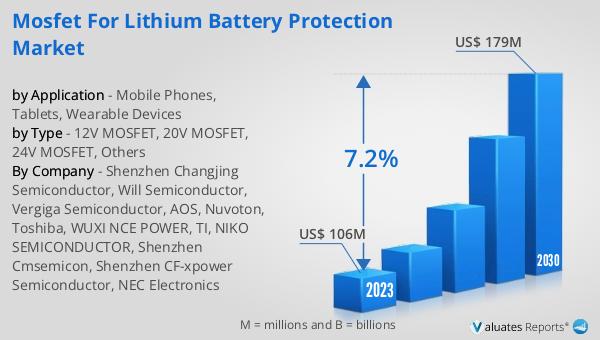

The global MOSFET for Lithium Battery Protection market was valued at US$ 106 million in 2023 and is anticipated to reach US$ 179 million by 2030, witnessing a CAGR of 7.2% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of MOSFETs in the lithium battery protection sector. The increasing demand for consumer electronics, electric vehicles, and renewable energy storage systems is driving this growth. As technology continues to advance, the need for more efficient and reliable battery protection solutions becomes increasingly critical. MOSFETs play a crucial role in ensuring the safety and longevity of lithium batteries, making them an essential component in various applications. The projected growth of this market underscores the importance of MOSFETs in the evolving electronics landscape, as they help mitigate risks associated with lithium batteries, such as overcharging, overheating, and short-circuiting. This market outlook provides valuable insights into the future trends and opportunities in the Global MOSFET for Lithium Battery Protection Market, emphasizing the growing importance of these components in ensuring the safety and efficiency of modern electronic devices.

| Report Metric | Details |

| Report Name | MOSFET for Lithium Battery Protection Market |

| Accounted market size in 2023 | US$ 106 million |

| Forecasted market size in 2030 | US$ 179 million |

| CAGR | 7.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Shenzhen Changjing Semiconductor, Will Semiconductor, Vergiga Semiconductor, AOS, Nuvoton, Toshiba, WUXI NCE POWER, TI, NIKO SEMICONDUCTOR, Shenzhen Cmsemicon, Shenzhen CF-xpower Semiconductor, NEC Electronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |