What is Global Medical X-Ray Film Digital Scanning Market?

The Global Medical X-Ray Film Digital Scanning Market refers to the industry focused on converting traditional X-ray films into digital formats. This process involves using specialized scanners to digitize the images, making them easier to store, share, and analyze. The digital format offers numerous advantages over traditional film, including enhanced image quality, reduced physical storage space, and the ability to quickly share images with other healthcare professionals. This market is driven by the increasing demand for efficient and accurate diagnostic tools in the medical field. As healthcare facilities continue to modernize, the adoption of digital scanning technologies is becoming more prevalent. This shift not only improves patient care but also streamlines operations within medical institutions. The market encompasses a range of products and services, including scanners, software, and maintenance services, all aimed at facilitating the transition from analog to digital imaging.

Fixed, Portable in the Global Medical X-Ray Film Digital Scanning Market:

In the Global Medical X-Ray Film Digital Scanning Market, there are two primary types of scanners: fixed and portable. Fixed scanners are stationary devices typically installed in hospitals and large medical centers. These scanners are designed for high-volume scanning and are often integrated into the facility's existing IT infrastructure. They offer high-resolution scanning capabilities and are ideal for environments where a large number of X-ray films need to be digitized regularly. Fixed scanners are known for their durability and ability to handle continuous use, making them a reliable choice for busy medical facilities. On the other hand, portable scanners are designed for flexibility and mobility. These devices are compact and lightweight, allowing healthcare professionals to easily transport them between different locations. Portable scanners are particularly useful in clinics and smaller medical centers where space is limited, or in situations where on-site scanning is required, such as in remote or rural areas. Despite their smaller size, portable scanners still offer high-quality digital imaging, ensuring that the digitized X-ray films are clear and accurate. Both fixed and portable scanners play a crucial role in the digitization process, each catering to different needs within the healthcare industry. The choice between fixed and portable scanners depends on various factors, including the volume of X-ray films to be scanned, available space, and the specific requirements of the medical facility. As technology continues to advance, both types of scanners are becoming more efficient and user-friendly, further driving the adoption of digital scanning in the medical field.

Hospital, Clinic, Medical Center in the Global Medical X-Ray Film Digital Scanning Market:

The usage of Global Medical X-Ray Film Digital Scanning Market technologies in hospitals, clinics, and medical centers significantly enhances the efficiency and quality of patient care. In hospitals, the high volume of patients and the need for quick and accurate diagnostics make digital scanning an invaluable tool. By converting traditional X-ray films into digital formats, hospitals can easily store and retrieve patient images, reducing the time spent on manual handling and minimizing the risk of losing important records. This digital transformation also facilitates better collaboration among healthcare professionals, as images can be quickly shared and reviewed by specialists, leading to faster and more accurate diagnoses. In clinics, where space and resources may be more limited compared to larger hospitals, portable digital scanners offer a practical solution. These devices allow clinics to maintain high standards of diagnostic imaging without the need for extensive infrastructure. The ability to quickly digitize X-ray films on-site means that clinics can provide timely care to their patients, improving overall patient satisfaction and outcomes. Additionally, the digital format allows for easier integration with electronic health records (EHR) systems, streamlining the workflow and enhancing the clinic's operational efficiency. Medical centers, which often serve as specialized facilities for specific types of care, also benefit greatly from digital scanning technologies. Whether it's a center focused on orthopedics, cardiology, or oncology, the ability to digitize X-ray films ensures that high-quality images are readily available for detailed analysis and treatment planning. This is particularly important in specialized care, where precise imaging is crucial for effective treatment. The digital format also supports advanced imaging techniques, such as 3D reconstruction and image enhancement, providing medical professionals with more tools to deliver optimal care. Overall, the adoption of digital scanning technologies in hospitals, clinics, and medical centers represents a significant advancement in medical imaging, leading to improved patient care, enhanced operational efficiency, and better health outcomes.

Global Medical X-Ray Film Digital Scanning Market Outlook:

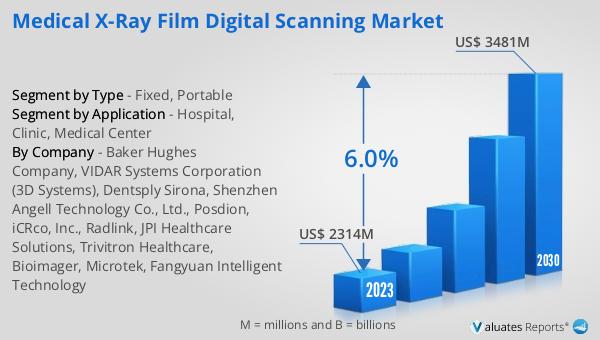

The global Medical X-Ray Film Digital Scanning market was valued at US$ 2314 million in 2023 and is anticipated to reach US$ 3481 million by 2030, witnessing a CAGR of 6.0% during the forecast period 2024-2030. This growth reflects the increasing demand for digital solutions in medical imaging, driven by the need for more efficient and accurate diagnostic tools. The transition from traditional X-ray films to digital formats offers numerous benefits, including improved image quality, easier storage and retrieval, and enhanced collaboration among healthcare professionals. As healthcare facilities continue to modernize, the adoption of digital scanning technologies is expected to rise, further driving the market's growth. The market encompasses a range of products and services, including scanners, software, and maintenance services, all aimed at facilitating the transition from analog to digital imaging. This shift not only improves patient care but also streamlines operations within medical institutions, making the Global Medical X-Ray Film Digital Scanning Market a critical component of the modern healthcare landscape.

| Report Metric | Details |

| Report Name | Medical X-Ray Film Digital Scanning Market |

| Accounted market size in 2023 | US$ 2314 million |

| Forecasted market size in 2030 | US$ 3481 million |

| CAGR | 6.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Baker Hughes Company, VIDAR Systems Corporation (3D Systems), Dentsply Sirona, Shenzhen Angell Technology Co., Ltd., Posdion, iCRco, Inc., Radlink, JPI Healthcare Solutions, Trivitron Healthcare, Bioimager, Microtek, Fangyuan Intelligent Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |