What is Global Precision Fluid Dispensing System & Equipment Market?

The Global Precision Fluid Dispensing System & Equipment Market refers to the industry that manufactures and supplies equipment designed to dispense precise amounts of fluids in various applications. These systems are crucial in industries where accuracy and consistency in fluid application are paramount. The market encompasses a wide range of equipment, including fully automatic, semi-automatic, and manual dispensing systems. These systems are used in numerous sectors such as electronics, automotive, medical, and more. The precision fluid dispensing systems ensure that the right amount of fluid is applied, reducing waste and improving the quality of the final product. This market is driven by the increasing demand for high-precision manufacturing processes and the need for automation in various industries.

Fully Automatic Dispensing System, Semi-automatic Dispensing System, Manual Dispensing System in the Global Precision Fluid Dispensing System & Equipment Market:

Fully Automatic Dispensing Systems are advanced machines designed to dispense fluids with high precision and minimal human intervention. These systems are equipped with sophisticated software and sensors that ensure accurate fluid delivery. They are ideal for high-volume production environments where consistency and speed are crucial. Fully automatic systems can handle complex dispensing tasks, such as applying adhesives, lubricants, or coatings, with high repeatability. They are commonly used in industries like electronics, where tiny amounts of fluid need to be applied to small components with great accuracy. Semi-automatic Dispensing Systems, on the other hand, require some level of human intervention. These systems are typically used in applications where flexibility and adaptability are needed. Operators can control the dispensing process, making adjustments as necessary to ensure the correct amount of fluid is applied. Semi-automatic systems are often used in smaller production runs or in situations where the dispensing requirements may vary from one task to another. Manual Dispensing Systems are the most basic type of fluid dispensing equipment. These systems rely entirely on human operators to control the dispensing process. While they may lack the precision and speed of automated systems, manual dispensers are highly versatile and can be used in a wide range of applications. They are particularly useful in situations where the volume of fluid to be dispensed is small, or where the dispensing process needs to be highly controlled by a skilled operator. In the Global Precision Fluid Dispensing System & Equipment Market, each type of system has its own set of advantages and is suited to different applications. Fully automatic systems offer the highest level of precision and efficiency, making them ideal for large-scale production environments. Semi-automatic systems provide a balance between automation and human control, offering flexibility for various dispensing tasks. Manual systems, while less advanced, offer unmatched versatility and control, making them suitable for specialized applications. The choice of system depends on factors such as the volume of production, the complexity of the dispensing task, and the level of precision required.

Electronic Components, Automobile, Monitor, Battery, Medical in the Global Precision Fluid Dispensing System & Equipment Market:

The Global Precision Fluid Dispensing System & Equipment Market finds extensive usage in various industries, including electronic components, automobiles, monitors, batteries, and medical devices. In the electronics industry, precision fluid dispensing systems are used to apply small amounts of adhesives, solder paste, and other materials to tiny components on circuit boards. This ensures that each component is securely attached and functions correctly. The high precision of these systems is crucial in preventing defects and ensuring the reliability of electronic devices. In the automotive industry, these systems are used to apply lubricants, sealants, and adhesives to various parts of a vehicle. This helps in improving the performance and durability of automotive components. For instance, precision fluid dispensing systems are used to apply sealants to engine components, ensuring that they are properly sealed and protected from contaminants. In the monitor manufacturing industry, these systems are used to apply adhesives and coatings to display panels. This ensures that the panels are securely attached and have a high-quality finish. Precision fluid dispensing systems are also used in the production of batteries, where they are used to apply electrolytes and other materials to battery cells. This ensures that the cells are properly filled and function correctly. In the medical industry, precision fluid dispensing systems are used to apply adhesives, coatings, and other materials to medical devices. This ensures that the devices are securely assembled and function correctly. For instance, these systems are used to apply adhesives to catheters, ensuring that they are securely attached and do not leak. The high precision of these systems is crucial in ensuring the safety and reliability of medical devices. Overall, the Global Precision Fluid Dispensing System & Equipment Market plays a vital role in various industries, ensuring that fluids are applied with high precision and consistency. This helps in improving the quality and reliability of products, reducing waste, and increasing efficiency in manufacturing processes.

Global Precision Fluid Dispensing System & Equipment Market Outlook:

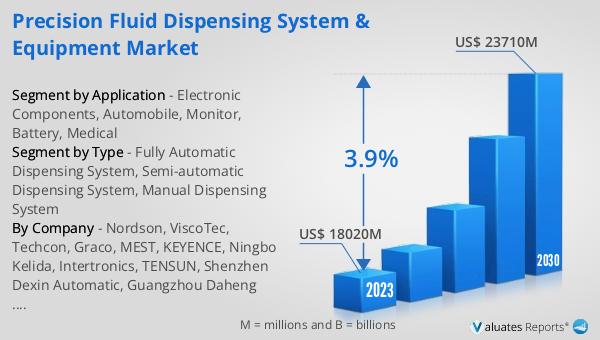

The global Precision Fluid Dispensing System & Equipment market was valued at US$ 18,020 million in 2023 and is anticipated to reach US$ 23,710 million by 2030, witnessing a CAGR of 3.9% during the forecast period 2024-2030. This market growth is driven by the increasing demand for high-precision manufacturing processes and the need for automation in various industries. Precision fluid dispensing systems are essential in ensuring that the right amount of fluid is applied in various applications, reducing waste and improving the quality of the final product. The market encompasses a wide range of equipment, including fully automatic, semi-automatic, and manual dispensing systems, each with its own set of advantages and suited to different applications. The electronics, automotive, medical, and other industries are increasingly adopting these systems to improve their manufacturing processes and ensure the reliability and quality of their products. The growing demand for miniaturized electronic components, the increasing complexity of automotive systems, and the need for high-quality medical devices are some of the key factors driving the growth of the Precision Fluid Dispensing System & Equipment market. As industries continue to evolve and require more precise and efficient manufacturing processes, the demand for precision fluid dispensing systems is expected to grow, further driving the market's expansion.

| Report Metric | Details |

| Report Name | Precision Fluid Dispensing System & Equipment Market |

| Accounted market size in 2023 | US$ 18020 million |

| Forecasted market size in 2030 | US$ 23710 million |

| CAGR | 3.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Nordson, ViscoTec, Techcon, Graco, MEST, KEYENCE, Ningbo Kelida, Intertronics, TENSUN, Shenzhen Dexin Automatic, Guangzhou Daheng Automation Equipment, Tianhao Dispensing Robot, IEI, SAEJONG, Venison, Lampda, Twin Engineers, Second Intelligent, MUSASHI, SMART VISION |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |