What is Global Ophthalmic Lathe Market?

The Global Ophthalmic Lathe Market refers to a specialized segment within the medical equipment industry, focusing on the production and distribution of lathes used in ophthalmology. These lathes are precision tools designed for crafting and shaping ophthalmic products, such as contact lenses and intraocular lenses (IOLs), with utmost accuracy. The demand for these lathes is driven by the need for high-quality ophthalmic products that meet the stringent standards of the healthcare industry. As eye-related conditions and diseases become more prevalent worldwide, the requirement for effective and precise ophthalmic solutions is on the rise. This, in turn, propels the growth of the ophthalmic lathe market. Manufacturers in this market are continuously innovating and improving their products to cater to the evolving needs of ophthalmologists and optometrists, ensuring that the lenses produced offer optimal vision correction and comfort to the end-users. The global reach of this market is expanding, with significant growth opportunities in both developed and emerging economies, where awareness and access to eye care services are increasing.

Surface Roughness ≤6nm, Surface Roughness ≤2nm in the Global Ophthalmic Lathe Market:

In the realm of the Global Ophthalmic Lathe Market, the distinction between Surface Roughness ≤6nm and Surface Roughness ≤2nm is of paramount importance, particularly when it comes to the precision and quality of ophthalmic products such as contact lenses and intraocular lenses (IOLs). Surface roughness is a critical parameter in the manufacturing process, influencing not only the performance and comfort of the final product but also its optical clarity and durability. Lathes that can achieve a surface roughness of ≤2nm are at the forefront of technology, offering unparalleled precision that results in lenses with superior quality. These high-precision lathes are essential for producing advanced ophthalmic products that meet the increasing demands for better vision correction solutions. On the other hand, lathes with a surface roughness of ≤6nm, while still providing a high level of precision, are more commonly used for a broader range of ophthalmic products. The choice between these two categories depends on the specific requirements of the lens being produced, including the level of precision needed and the intended use of the product. Manufacturers in the Global Ophthalmic Lathe Market invest heavily in research and development to push the boundaries of what's possible in lens manufacturing technology, striving to achieve even lower levels of surface roughness. This relentless pursuit of perfection ensures that the ophthalmic products available to consumers and healthcare providers continue to improve in quality, offering better vision correction options and enhancing the quality of life for individuals with vision impairments.

Contact Lenses Production, Intraocular Lens (IOLs) Production in the Global Ophthalmic Lathe Market:

The Global Ophthalmic Lathe Market plays a crucial role in the production of contact lenses and intraocular lenses (IOLs), two of the most important products in the field of vision correction and eye care. In the production of contact lenses, precision and accuracy are paramount, as these lenses must fit comfortably on the eye's surface while correcting a wide range of vision problems. Ophthalmic lathes enable manufacturers to shape and polish lenses to exact specifications, ensuring each lens offers the correct curvature, thickness, and optical power. This precision manufacturing process is essential for producing contact lenses that provide clear vision and do not cause irritation or discomfort to the wearer. Similarly, in the production of intraocular lenses (IOLs), which are implanted inside the eye to replace the eye's natural lens during cataract surgery, the role of ophthalmic lathes is indispensable. These lathes allow for the creation of IOLs with precise dimensions and optical properties, ensuring that each lens can provide the patient with the best possible vision post-surgery. The ability to produce lenses with such high levels of accuracy and consistency has made the Global Ophthalmic Lathe Market a key player in the advancement of eye care and vision correction technologies. As the demand for more sophisticated and effective vision correction solutions grows, the importance of this market continues to rise, driving innovation and improving outcomes for patients worldwide.

Global Ophthalmic Lathe Market Outlook:

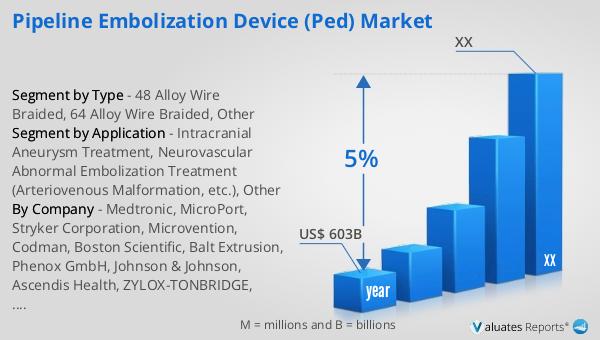

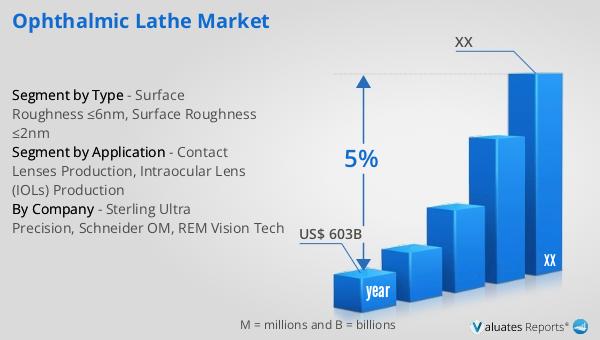

Our research indicates that the global market for medical devices is currently valued at approximately US$ 603 billion as of the year 2023. This market is on a trajectory of steady growth, with expectations to expand at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is reflective of the increasing demand for medical devices across various healthcare sectors, driven by technological advancements, an aging global population, and a rising focus on healthcare quality and accessibility. The medical device market encompasses a wide range of products, including those found in the Global Ophthalmic Lathe Market, which are essential for producing high-quality ophthalmic products such as contact lenses and intraocular lenses. As the healthcare industry continues to evolve, the demand for innovative and effective medical devices is expected to rise, further propelling the growth of this market. This expansion signifies not only the growing importance of medical devices in modern healthcare but also the potential for significant advancements in medical technology and patient care in the coming years.

| Report Metric | Details |

| Report Name | Ophthalmic Lathe Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Sterling Ultra Precision, Schneider OM, REM Vision Tech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |