What is Global Crank Drive Motor Market?

The Global Crank Drive Motor Market refers to the worldwide industry focused on the production, distribution, and sale of crank drive motors. These motors are primarily used in electric bicycles (e-bikes) and other light electric vehicles. Crank drive motors are known for their efficiency and ability to provide a more natural riding experience by delivering power directly to the bike's crankshaft. This type of motor is typically mounted at the bike's bottom bracket, which allows for better weight distribution and improved handling. The market encompasses various stakeholders, including manufacturers, suppliers, distributors, and end-users. It is driven by factors such as increasing environmental awareness, the rising popularity of e-bikes, and advancements in motor technology. The market is also influenced by regional regulations, consumer preferences, and economic conditions. As the demand for sustainable and efficient transportation solutions grows, the Global Crank Drive Motor Market is expected to expand, offering numerous opportunities for innovation and growth.

Below 250w, Above 250w in the Global Crank Drive Motor Market:

In the Global Crank Drive Motor Market, motors are generally categorized based on their power output, with two primary segments being Below 250W and Above 250W. Motors Below 250W are typically used in e-bikes designed for urban commuting and recreational purposes. These motors are favored for their lightweight and energy-efficient characteristics, making them ideal for city riding where speed limits and regulations often restrict higher power outputs. They provide sufficient assistance for daily commuting, helping riders tackle inclines and longer distances without excessive physical exertion. On the other hand, motors Above 250W are more powerful and are often found in e-bikes intended for off-road, mountain biking, and high-performance applications. These motors offer greater torque and speed, enabling riders to navigate challenging terrains and steep hills with ease. They are also suitable for cargo e-bikes, which require additional power to carry heavy loads. The choice between Below 250W and Above 250W motors depends on the intended use of the e-bike, with each segment catering to different rider needs and preferences. The market for these motors is influenced by factors such as technological advancements, regulatory frameworks, and consumer demand for specific performance characteristics. As the e-bike market continues to grow, the demand for both Below 250W and Above 250W crank drive motors is expected to increase, driven by the diverse needs of urban commuters, recreational riders, and adventure enthusiasts.

OEM, Aftermarket in the Global Crank Drive Motor Market:

The usage of Global Crank Drive Motor Market can be broadly categorized into Original Equipment Manufacturer (OEM) and Aftermarket segments. OEMs are companies that produce e-bikes and other light electric vehicles, integrating crank drive motors into their products during the manufacturing process. These manufacturers rely on crank drive motors to enhance the performance, efficiency, and appeal of their e-bikes. By incorporating high-quality motors, OEMs can offer products that meet consumer expectations for reliability, power, and smooth riding experience. The OEM segment is crucial for the growth of the crank drive motor market, as it drives innovation and sets industry standards. On the other hand, the Aftermarket segment involves the sale of crank drive motors as replacement parts or upgrades for existing e-bikes. This segment caters to consumers who wish to enhance the performance of their current e-bikes or replace faulty motors. The Aftermarket segment is essential for maintaining the longevity and functionality of e-bikes, providing consumers with options to customize and improve their rides. Both OEM and Aftermarket segments play a vital role in the overall growth and development of the Global Crank Drive Motor Market, addressing the diverse needs of manufacturers and end-users.

Global Crank Drive Motor Market Outlook:

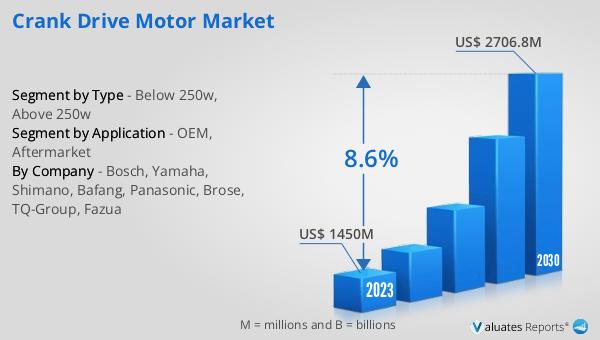

The global Crank Drive Motor market was valued at US$ 1450 million in 2023 and is anticipated to reach US$ 2706.8 million by 2030, witnessing a CAGR of 8.6% during the forecast period 2024-2030. This significant growth reflects the increasing demand for efficient and sustainable transportation solutions, particularly in urban areas where e-bikes are becoming a popular alternative to traditional vehicles. The market's expansion is driven by factors such as technological advancements in motor design, growing environmental awareness, and supportive government policies promoting the use of electric vehicles. As more consumers recognize the benefits of e-bikes, including cost savings, reduced carbon footprint, and improved health, the demand for crank drive motors is expected to rise. This growth trajectory highlights the potential for innovation and investment in the crank drive motor industry, offering opportunities for manufacturers, suppliers, and other stakeholders to capitalize on the expanding market.

| Report Metric | Details |

| Report Name | Crank Drive Motor Market |

| Accounted market size in 2023 | US$ 1450 million |

| Forecasted market size in 2030 | US$ 2706.8 million |

| CAGR | 8.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bosch, Yamaha, Shimano, Bafang, Panasonic, Brose, TQ-Group, Fazua |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |