What is Global Vessel Integrated Bridge System Market?

The Global Vessel Integrated Bridge System Market refers to the industry focused on the development, production, and implementation of advanced bridge systems for maritime vessels. These systems integrate various navigational and operational tools into a single, cohesive interface, enhancing the efficiency and safety of maritime operations. The market encompasses a wide range of technologies, including radar, GPS, automatic identification systems (AIS), electronic chart display and information systems (ECDIS), and other navigational aids. These integrated systems are designed to streamline the management of vessel operations, reduce human error, and improve situational awareness for ship crews. The market is driven by the increasing demand for advanced maritime safety solutions, the growing complexity of modern vessels, and stringent regulatory requirements. As global trade and maritime activities continue to expand, the need for sophisticated bridge systems is expected to rise, making this market a critical component of the maritime industry.

Integrated Bridge and Navigation System, Integrated Bridge and Control System, Others in the Global Vessel Integrated Bridge System Market:

Integrated Bridge and Navigation Systems (IBNS) are comprehensive solutions that combine various navigational tools and systems into a unified interface, allowing for seamless operation and enhanced situational awareness. These systems typically include radar, GPS, AIS, ECDIS, and other navigational aids, all integrated into a single console. The primary goal of IBNS is to improve the efficiency and safety of maritime operations by providing ship crews with a centralized platform for monitoring and controlling all navigational aspects of the vessel. This integration reduces the likelihood of human error and enhances decision-making capabilities, particularly in complex or high-traffic maritime environments. Integrated Bridge and Control Systems (IBCS) take this concept a step further by incorporating additional control functionalities, such as engine and propulsion management, into the bridge system. This allows for a more holistic approach to vessel operation, where navigational and operational controls are seamlessly integrated. IBCS are particularly beneficial for larger vessels, such as tankers and container ships, where the complexity of operations requires a more sophisticated control system. Other integrated systems in the Global Vessel Integrated Bridge System Market include specialized solutions tailored to specific types of vessels or operational requirements. For example, some systems may focus on enhancing the capabilities of megayachts, providing advanced navigational and control features that cater to the unique needs of luxury vessels. Similarly, systems designed for cruise ships may prioritize passenger safety and comfort, integrating advanced monitoring and control features to ensure smooth and efficient operations. Overall, the Global Vessel Integrated Bridge System Market encompasses a wide range of technologies and solutions, each designed to meet the specific needs of different types of vessels and maritime operations.

Megayachts, Tankers, Container Ships, Cruise Ships, Others in the Global Vessel Integrated Bridge System Market:

The usage of Global Vessel Integrated Bridge System Market technologies varies significantly across different types of vessels, each with its unique operational requirements and challenges. For megayachts, integrated bridge systems provide a seamless and sophisticated interface that enhances navigational accuracy and operational efficiency. These systems often include advanced features such as dynamic positioning, automated route planning, and real-time weather updates, ensuring a smooth and luxurious experience for passengers. The integration of various navigational and control systems into a single console also allows for easier management of the vessel, reducing the workload on the crew and enhancing overall safety. In the case of tankers, integrated bridge systems play a crucial role in ensuring the safe and efficient transport of hazardous materials. These systems provide real-time monitoring and control of the vessel's position, speed, and course, allowing for precise navigation in challenging maritime environments. The integration of engine and propulsion management systems also ensures optimal fuel efficiency and reduces the risk of accidents or spills. For container ships, integrated bridge systems are essential for managing the complex logistics of cargo transport. These systems provide real-time tracking and monitoring of the vessel's position and cargo, allowing for efficient route planning and timely delivery of goods. The integration of navigational and operational controls also enhances the safety and efficiency of the vessel, reducing the risk of accidents and delays. Cruise ships, on the other hand, require integrated bridge systems that prioritize passenger safety and comfort. These systems provide advanced monitoring and control features, such as real-time weather updates, automated route planning, and dynamic positioning, ensuring a smooth and enjoyable experience for passengers. The integration of various navigational and control systems also allows for efficient management of the vessel, reducing the workload on the crew and enhancing overall safety. Other types of vessels, such as fishing boats and research vessels, also benefit from integrated bridge systems, which provide advanced navigational and operational capabilities tailored to their specific needs. Overall, the usage of Global Vessel Integrated Bridge System Market technologies varies significantly across different types of vessels, each with its unique operational requirements and challenges.

Global Vessel Integrated Bridge System Market Outlook:

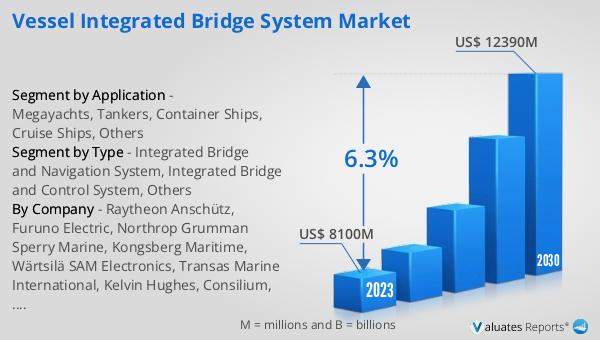

The global Vessel Integrated Bridge System market was valued at US$ 8100 million in 2023 and is anticipated to reach US$ 12390 million by 2030, witnessing a CAGR of 6.3% during the forecast period 2024-2030. This market growth is driven by the increasing demand for advanced maritime safety solutions, the growing complexity of modern vessels, and stringent regulatory requirements. As global trade and maritime activities continue to expand, the need for sophisticated bridge systems is expected to rise, making this market a critical component of the maritime industry. The integration of various navigational and operational tools into a single, cohesive interface enhances the efficiency and safety of maritime operations, reducing the likelihood of human error and improving situational awareness for ship crews. The market encompasses a wide range of technologies, including radar, GPS, AIS, ECDIS, and other navigational aids, all designed to streamline the management of vessel operations. The increasing adoption of these advanced systems across different types of vessels, such as megayachts, tankers, container ships, and cruise ships, further drives the market growth. Overall, the Global Vessel Integrated Bridge System Market is poised for significant growth in the coming years, driven by the increasing demand for advanced maritime safety solutions and the growing complexity of modern vessels.

| Report Metric | Details |

| Report Name | Vessel Integrated Bridge System Market |

| Accounted market size in 2023 | US$ 8100 million |

| Forecasted market size in 2030 | US$ 12390 million |

| CAGR | 6.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Raytheon Anschütz, Furuno Electric, Northrop Grumman Sperry Marine, Kongsberg Maritime, Wärtsilä SAM Electronics, Transas Marine International, Kelvin Hughes, Consilium, NORIS, Libra-Plast AS, Alphatron Marine, Raytheon, TOKYO KEIKI, NAUDEQ, Elpro, Marine Technologies, Praxis Automation Technology, Radio Zeeland DMP, Syberg, Brunvoll |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |