What is Global Industrial Road Roller Market?

The Global Industrial Road Roller Market is a significant segment within the construction machinery industry, focusing on the production and utilization of road rollers. These machines are essential for compacting soil, gravel, concrete, or asphalt in the construction of roads and foundations. The market encompasses a variety of road rollers, including vibratory rollers, static road rollers, and pneumatic rollers, each designed for specific applications and terrain types. The demand for road rollers is driven by the need for infrastructure development, urbanization, and the maintenance of existing road networks. The market is characterized by technological advancements, such as the integration of GPS and telematics for better operational efficiency and safety. Key players in the market are continuously innovating to offer more efficient, durable, and environmentally friendly machines. The global reach of this market includes regions like North America, Europe, Asia-Pacific, and the Middle East, each with its unique set of requirements and regulations. The market's growth is also influenced by government investments in infrastructure projects and the increasing adoption of advanced construction techniques. Overall, the Global Industrial Road Roller Market plays a crucial role in supporting the construction industry's efforts to build and maintain essential infrastructure.

Vibratory Roller, Static Road Roller in the Global Industrial Road Roller Market:

Vibratory rollers and static road rollers are two primary types of machines within the Global Industrial Road Roller Market, each serving distinct purposes in construction projects. Vibratory rollers are equipped with a vibrating drum that compacts materials through a combination of static pressure and dynamic force. This type of roller is particularly effective for compacting granular and mixed soils, making it ideal for tasks such as road construction, airport runways, and large-scale industrial projects. The vibration mechanism enhances the compaction process, ensuring a denser and more stable base. On the other hand, static road rollers rely solely on the weight of the machine to achieve compaction. These rollers are typically used for finishing tasks, where a smooth and even surface is required. Static rollers are less effective on granular soils but excel in compacting cohesive materials like clay and silt. Both types of rollers are integral to the construction process, with their usage determined by the specific requirements of the project. The choice between vibratory and static rollers depends on factors such as soil type, project scale, and desired compaction quality. Manufacturers in the Global Industrial Road Roller Market are continually innovating to improve the efficiency, durability, and environmental impact of these machines. For instance, advancements in engine technology have led to more fuel-efficient and lower-emission rollers, aligning with global sustainability goals. Additionally, the integration of smart technologies, such as GPS and telematics, allows for better monitoring and optimization of roller operations. This not only enhances productivity but also ensures greater safety on construction sites. The market for vibratory and static road rollers is highly competitive, with key players focusing on expanding their product portfolios and geographic presence. Companies are investing in research and development to introduce new features and capabilities that meet the evolving needs of the construction industry. The demand for these machines is also influenced by government infrastructure projects, urbanization trends, and the need for regular maintenance of existing road networks. In summary, vibratory rollers and static road rollers are essential components of the Global Industrial Road Roller Market, each offering unique benefits and applications. Their continued development and adoption are crucial for the efficient and sustainable construction of infrastructure worldwide.

Highway, Airport Road, Industrial Park in the Global Industrial Road Roller Market:

The usage of road rollers in the Global Industrial Road Roller Market spans various critical areas, including highways, airport roads, and industrial parks. Highways are the lifelines of modern transportation, facilitating the movement of goods and people across vast distances. Road rollers play a pivotal role in highway construction by ensuring a stable and durable road surface. Vibratory rollers are often used in the initial stages to compact the sub-base and base layers, providing a solid foundation for the asphalt or concrete surface. Static rollers are then employed to achieve a smooth and even finish, enhancing the road's longevity and performance. The construction of airport roads is another significant application of road rollers. Airports require highly durable and stable surfaces to withstand the heavy loads and constant traffic of aircraft and ground vehicles. Vibratory rollers are particularly effective in compacting the various layers of materials used in runway and taxiway construction, ensuring a dense and stable base. Static rollers are used in the final stages to achieve a smooth and even surface, essential for the safe and efficient operation of aircraft. Industrial parks, which house manufacturing plants, warehouses, and other industrial facilities, also benefit from the use of road rollers. These areas require robust and durable road surfaces to support the movement of heavy machinery and vehicles. Vibratory rollers are used to compact the sub-base and base layers, providing a stable foundation for the road surface. Static rollers are then employed to achieve a smooth and even finish, ensuring the road can withstand the heavy loads and constant traffic typical of industrial environments. The use of road rollers in these areas is driven by the need for durable and stable road surfaces that can withstand heavy loads and constant traffic. The Global Industrial Road Roller Market continues to evolve, with manufacturers focusing on developing more efficient, durable, and environmentally friendly machines. Advancements in engine technology, smart technologies, and materials science are driving the development of new and improved road rollers that meet the evolving needs of the construction industry. In conclusion, the usage of road rollers in highways, airport roads, and industrial parks is essential for the construction and maintenance of durable and stable road surfaces. The Global Industrial Road Roller Market plays a crucial role in supporting these efforts, with ongoing innovations and advancements driving the development of more efficient and sustainable machines.

Global Industrial Road Roller Market Outlook:

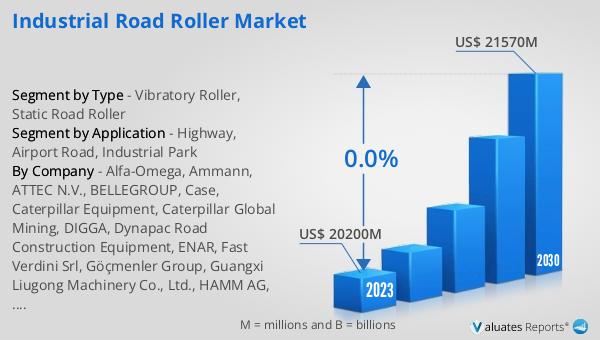

The global Industrial Road Roller market was valued at US$ 20,200 million in 2023 and is expected to reach US$ 21,570 million by 2030, maintaining a steady CAGR of 0.0% during the forecast period from 2024 to 2030. According to our Construction Machinery research center, sales of construction machinery in Europe saw a significant increase of 24% in 2021. In 2022, the construction machinery revenue in Europe was approximately US$ 22 billion. Meanwhile, the US market recorded sales of about US$ 36 billion in construction machinery in 2022. This data highlights the robust demand for construction machinery, including road rollers, driven by ongoing infrastructure projects and urbanization trends. The steady growth in the Industrial Road Roller market reflects the essential role these machines play in the construction industry, ensuring the development and maintenance of critical infrastructure.

| Report Metric | Details |

| Report Name | Industrial Road Roller Market |

| Accounted market size in 2023 | US$ 20200 million |

| Forecasted market size in 2030 | US$ 21570 million |

| CAGR | 0.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Alfa-Omega, Ammann, ATTEC N.V., BELLEGROUP, Case, Caterpillar Equipment, Caterpillar Global Mining, DIGGA, Dynapac Road Construction Equipment, ENAR, Fast Verdini Srl, Göçmenler Group, Guangxi Liugong Machinery Co., Ltd., HAMM AG, HYUNDAI HEAVY INDUSTRIES |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |