What is Global Cu Electroplating Material Market?

The Global Cu Electroplating Material Market refers to the worldwide industry focused on the production and distribution of copper electroplating materials. These materials are essential in the process of electroplating, where a thin layer of copper is deposited onto the surface of a substrate, typically to enhance its appearance, improve corrosion resistance, or increase electrical conductivity. Copper electroplating is widely used across various industries, including electronics, automotive, and general manufacturing. The market for these materials is driven by the growing demand for electronic devices, advancements in semiconductor technology, and the need for durable and efficient components in various applications. As industries continue to innovate and expand, the demand for high-quality copper electroplating materials is expected to rise, making this market a critical component of the global manufacturing landscape. The market is characterized by a diverse range of products, including copper sulfate, copper anodes, and various additives that enhance the electroplating process. Companies operating in this market are continually investing in research and development to improve the efficiency and environmental sustainability of their products, ensuring they meet the evolving needs of their customers.

Organic, Inorganic in the Global Cu Electroplating Material Market:

In the Global Cu Electroplating Material Market, materials are primarily categorized into organic and inorganic types, each with distinct properties and applications. Organic copper electroplating materials typically involve the use of organic additives that enhance the plating process. These additives can improve the brightness, leveling, and overall quality of the copper deposit. Organic materials are often preferred in applications where a high degree of precision and aesthetic quality is required, such as in the production of decorative items or intricate electronic components. The use of organic additives can also help in reducing the internal stress of the plated layer, thereby enhancing the durability and performance of the final product. On the other hand, inorganic copper electroplating materials are based on inorganic compounds, such as copper sulfate, which is one of the most commonly used copper salts in electroplating. Inorganic materials are typically used in applications where high conductivity and corrosion resistance are paramount, such as in the production of electrical connectors and circuit boards. The choice between organic and inorganic materials often depends on the specific requirements of the application, including factors such as cost, environmental impact, and desired properties of the plated layer. In recent years, there has been a growing emphasis on developing environmentally friendly electroplating materials, leading to innovations in both organic and inorganic categories. For instance, researchers are exploring the use of biodegradable organic additives and more efficient inorganic compounds that reduce waste and energy consumption. This trend is driven by increasing regulatory pressures and consumer demand for sustainable manufacturing practices. As a result, companies in the Global Cu Electroplating Material Market are investing heavily in research and development to create products that not only meet performance standards but also align with environmental goals. The competition between organic and inorganic materials is also influenced by technological advancements in related fields, such as nanotechnology and surface engineering. These advancements are opening up new possibilities for enhancing the properties of electroplated layers, such as increased hardness, improved adhesion, and enhanced thermal stability. As the market continues to evolve, the interplay between organic and inorganic materials will likely shape the future of copper electroplating, with each category offering unique advantages and challenges. Ultimately, the choice of material will depend on a careful consideration of the specific needs of the application, as well as broader industry trends and regulatory requirements.

General Hardware, Semiconductor, Others in the Global Cu Electroplating Material Market:

The Global Cu Electroplating Material Market finds extensive usage in various sectors, including general hardware, semiconductors, and other industries. In the realm of general hardware, copper electroplating is employed to enhance the durability and aesthetic appeal of metal components. This includes items such as fasteners, tools, and decorative hardware, where a copper-plated finish can provide both corrosion resistance and a visually appealing surface. The use of copper electroplating in general hardware is driven by the need for long-lasting and reliable components that can withstand harsh environmental conditions. In the semiconductor industry, copper electroplating plays a crucial role in the fabrication of integrated circuits and other electronic components. Copper's excellent electrical conductivity makes it an ideal material for creating the intricate wiring and connections required in modern electronic devices. The demand for copper electroplating materials in this sector is fueled by the rapid advancement of semiconductor technology and the increasing complexity of electronic devices. As devices become smaller and more powerful, the precision and quality of copper electroplating become even more critical. Beyond general hardware and semiconductors, copper electroplating materials are also used in a variety of other applications. This includes the automotive industry, where copper-plated components are used in electrical systems and decorative trims. The aerospace industry also utilizes copper electroplating for its ability to provide reliable electrical connections and protect components from corrosion. Additionally, copper electroplating is used in the production of consumer goods, such as jewelry and household items, where it provides an attractive and durable finish. The versatility of copper electroplating materials makes them an essential component in a wide range of industries, each with its unique requirements and challenges. As the Global Cu Electroplating Material Market continues to grow, the development of new applications and technologies will likely drive further innovation and expansion in this field.

Global Cu Electroplating Material Market Outlook:

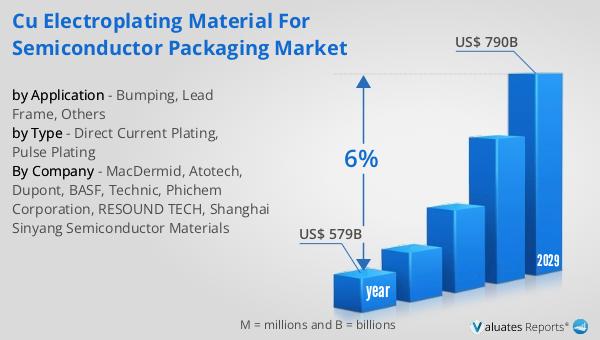

The global semiconductor market, which was valued at approximately $579 billion in 2022, is anticipated to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is indicative of the increasing demand for semiconductors across various industries, driven by technological advancements and the proliferation of electronic devices. The semiconductor industry is a critical component of the global economy, underpinning the development of a wide range of products, from consumer electronics to industrial machinery. The projected growth in the semiconductor market is expected to have a significant impact on related industries, including the Global Cu Electroplating Material Market. As the demand for semiconductors rises, so too does the need for high-quality copper electroplating materials, which are essential in the manufacturing of semiconductor components. The growth of the semiconductor market is also likely to spur innovation and investment in the development of new electroplating technologies and materials, as companies seek to meet the evolving needs of their customers. This dynamic interplay between the semiconductor and electroplating markets highlights the interconnected nature of modern manufacturing and the importance of continued research and development in these fields.

| Report Metric | Details |

| Report Name | Cu Electroplating Material Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | DuPont, BASF, Shanghai Sinyang Semiconductor Materials, ADEKA, Merck KGaA, Atotech, RESOUND TECH, PhiChem |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |