What is Global Home Sauna Heaters Market?

The Global Home Sauna Heaters Market refers to the worldwide industry involved in the production, distribution, and sale of heaters specifically designed for home saunas. These heaters are essential components of home saunas, providing the necessary heat to create a relaxing and therapeutic environment. The market encompasses various types of sauna heaters, including electric and wood-burning models, catering to different consumer preferences and installation requirements. The demand for home sauna heaters is driven by the growing interest in wellness and self-care, as more people seek to create spa-like experiences in the comfort of their homes. Additionally, advancements in technology and design have made home sauna heaters more efficient, user-friendly, and aesthetically pleasing, further boosting their popularity. The market is characterized by a diverse range of products, from compact, wall-mounted units to larger, floor-mounted models, each offering unique features and benefits. As the trend towards home wellness continues to grow, the Global Home Sauna Heaters Market is expected to expand, offering consumers a variety of options to enhance their home relaxation spaces.

Electric Sauna Heaters, Woodburning Sauna Heaters in the Global Home Sauna Heaters Market:

Electric sauna heaters and wood-burning sauna heaters are two primary types of heaters available in the Global Home Sauna Heaters Market, each offering distinct advantages and catering to different user preferences. Electric sauna heaters are popular for their convenience and ease of use. They are typically powered by electricity and can be easily controlled with a thermostat, allowing users to set and maintain their desired temperature with precision. These heaters are often equipped with safety features such as automatic shut-off and overheat protection, making them a reliable choice for home use. Electric sauna heaters come in various sizes and designs, including wall-mounted and floor-mounted models, to fit different sauna configurations. They are also known for their quick heating capabilities, providing a consistent and even heat distribution throughout the sauna. On the other hand, wood-burning sauna heaters offer a more traditional and authentic sauna experience. These heaters use wood as fuel, creating a natural and soothing heat that many sauna enthusiasts prefer. The process of heating the sauna with a wood-burning heater involves lighting a fire and allowing the wood to burn, which can take longer to reach the desired temperature compared to electric heaters. However, the ambiance and aroma of burning wood add to the overall sauna experience, making it a popular choice for those who appreciate the rustic charm. Wood-burning sauna heaters require proper ventilation and regular maintenance to ensure safe operation, but they are highly regarded for their ability to create a unique and immersive sauna environment. Both electric and wood-burning sauna heaters have their own set of benefits and considerations, and the choice between the two often depends on personal preferences, installation requirements, and the desired sauna experience. As the Global Home Sauna Heaters Market continues to evolve, manufacturers are constantly innovating to improve the performance, efficiency, and design of both types of heaters, providing consumers with a wide range of options to suit their needs.

Floor Mounted, Wall Mounted in the Global Home Sauna Heaters Market:

The usage of home sauna heaters in the Global Home Sauna Heaters Market can be categorized into two main installation types: floor-mounted and wall-mounted. Floor-mounted sauna heaters are typically larger and more powerful, making them suitable for spacious saunas that require a significant amount of heat. These heaters are installed on the floor of the sauna and are often designed to be the focal point of the space. Floor-mounted heaters are known for their robust construction and high heat output, which can quickly and efficiently warm up the entire sauna. They are ideal for traditional sauna setups where ample space is available, and the heater can be prominently displayed. Additionally, floor-mounted heaters often come with advanced features such as programmable controls, timers, and remote operation, providing users with a high level of convenience and customization. On the other hand, wall-mounted sauna heaters are more compact and space-saving, making them an excellent choice for smaller saunas or home installations where space is limited. These heaters are mounted on the wall, freeing up floor space and allowing for more flexible sauna design options. Wall-mounted heaters are typically easier to install and maintain, and they offer a sleek and modern appearance that can complement contemporary sauna interiors. Despite their smaller size, wall-mounted heaters are capable of delivering efficient and consistent heat, ensuring a comfortable sauna experience. They are often equipped with user-friendly controls and safety features, making them a practical choice for home use. Both floor-mounted and wall-mounted sauna heaters have their own unique advantages, and the choice between the two depends on factors such as the size of the sauna, available space, and personal preferences. As the Global Home Sauna Heaters Market continues to grow, manufacturers are developing innovative solutions to enhance the functionality and aesthetics of both types of heaters, providing consumers with a diverse range of options to create their ideal sauna environment.

Global Home Sauna Heaters Market Outlook:

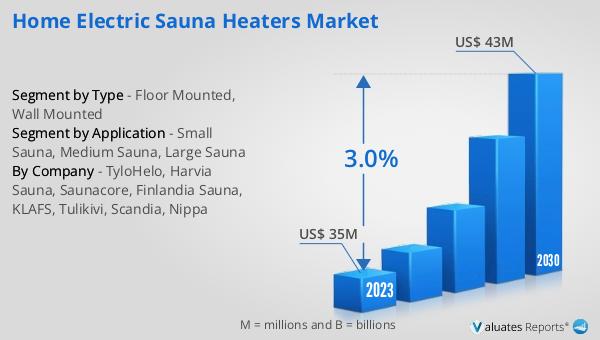

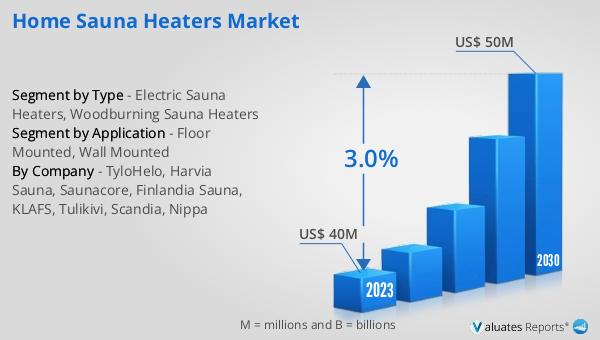

The global Home Sauna Heaters market was valued at US$ 40 million in 2023 and is anticipated to reach US$ 50 million by 2030, witnessing a CAGR of 3.0% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the home sauna heaters industry, driven by increasing consumer interest in home wellness and relaxation solutions. The projected growth reflects the rising demand for home sauna heaters as more individuals seek to create spa-like experiences within their homes. The market's expansion is also supported by advancements in heater technology, which have made these products more efficient, user-friendly, and aesthetically appealing. As consumers become more health-conscious and prioritize self-care, the adoption of home sauna heaters is expected to rise, contributing to the market's overall growth. The steady CAGR of 3.0% suggests a consistent increase in market value, highlighting the sustained interest and investment in home sauna heaters. This positive market outlook underscores the potential for continued innovation and development within the industry, offering consumers a wide range of options to enhance their home wellness routines. As the market evolves, manufacturers are likely to focus on improving product features, energy efficiency, and design to meet the diverse needs and preferences of consumers. Overall, the global Home Sauna Heaters market is poised for growth, driven by the ongoing trend towards home-based wellness solutions and the increasing popularity of home saunas.

| Report Metric | Details |

| Report Name | Home Sauna Heaters Market |

| Accounted market size in 2023 | US$ 40 million |

| Forecasted market size in 2030 | US$ 50 million |

| CAGR | 3.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TyloHelo, Harvia Sauna, Saunacore, Finlandia Sauna, KLAFS, Tulikivi, Scandia, Nippa |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |