What is Global Brain Neurointerventional Device Market?

The Global Brain Neurointerventional Device Market refers to the worldwide industry focused on the development, production, and distribution of medical devices used in neurointerventional procedures. These devices are specifically designed to treat various neurological conditions, such as aneurysms, arteriovenous malformations (AVMs), and ischemic strokes, by accessing the brain's vascular system through minimally invasive techniques. The market encompasses a wide range of products, including stents, coils, embolic agents, and thrombectomy devices, which are used by neurosurgeons and interventional radiologists to improve patient outcomes. The increasing prevalence of neurological disorders, advancements in medical technology, and growing awareness about minimally invasive procedures are driving the demand for these devices globally. Additionally, the aging population and rising healthcare expenditures in both developed and developing countries contribute to the market's expansion. As a result, the Global Brain Neurointerventional Device Market is experiencing significant growth, with numerous companies investing in research and development to introduce innovative and effective solutions for the treatment of complex brain conditions.

Ischemia, Hemorrhagic, Pathway in the Global Brain Neurointerventional Device Market:

Ischemia and hemorrhagic pathways are critical areas of focus within the Global Brain Neurointerventional Device Market. Ischemia refers to a condition where there is a restriction in blood supply to tissues, causing a shortage of oxygen and glucose needed for cellular metabolism. In the context of the brain, ischemic strokes occur when a blood clot obstructs the flow of blood to the brain, leading to potential brain damage. Neurointerventional devices such as thrombectomy devices and stent retrievers are used to remove these clots and restore normal blood flow, thereby minimizing brain damage and improving patient outcomes. On the other hand, hemorrhagic strokes are caused by the rupture of a blood vessel in the brain, leading to bleeding within or around the brain tissue. This type of stroke can be life-threatening and requires immediate medical intervention. Neurointerventional devices like coils and embolic agents are used to treat hemorrhagic strokes by sealing off the ruptured blood vessels and preventing further bleeding. The pathway-based approach in the Global Brain Neurointerventional Device Market involves the use of advanced imaging techniques and navigation systems to accurately target the affected areas in the brain. This ensures precise delivery of the neurointerventional devices, reducing the risk of complications and enhancing the effectiveness of the treatment. The integration of artificial intelligence and machine learning in these imaging and navigation systems further enhances the accuracy and efficiency of neurointerventional procedures. Additionally, the development of biocompatible materials and drug-eluting devices has significantly improved the safety and efficacy of neurointerventional treatments. These advancements have led to a paradigm shift in the management of ischemic and hemorrhagic strokes, with minimally invasive procedures becoming the preferred choice for both patients and healthcare providers. The Global Brain Neurointerventional Device Market is also witnessing a growing trend towards personalized medicine, where treatments are tailored to the individual patient's condition and genetic profile. This approach not only improves the success rate of neurointerventional procedures but also reduces the risk of adverse effects. Furthermore, the increasing collaboration between medical device manufacturers, research institutions, and healthcare providers is fostering innovation and accelerating the development of new and improved neurointerventional devices. As a result, the Global Brain Neurointerventional Device Market is poised for continued growth, driven by the rising demand for effective and minimally invasive treatments for ischemic and hemorrhagic strokes.

Hospital, Clinic in the Global Brain Neurointerventional Device Market:

The usage of Global Brain Neurointerventional Device Market in hospitals and clinics is pivotal in the treatment of various neurological conditions. Hospitals, being the primary healthcare facilities, are equipped with advanced neurointerventional devices and technologies to provide comprehensive care to patients with complex brain disorders. These devices are used in the neurology and neurosurgery departments to perform minimally invasive procedures, such as thrombectomies, aneurysm coilings, and AVM embolizations. The availability of state-of-the-art imaging systems, such as MRI and CT scanners, in hospitals enables precise diagnosis and treatment planning for neurointerventional procedures. Moreover, hospitals often have multidisciplinary teams of neurologists, neurosurgeons, interventional radiologists, and other specialists who collaborate to deliver optimal patient care. The integration of neurointerventional devices in hospital settings has significantly improved patient outcomes, reduced recovery times, and minimized the risk of complications. Clinics, on the other hand, play a crucial role in providing outpatient care and follow-up services for patients undergoing neurointerventional treatments. These facilities are often equipped with essential neurointerventional devices and imaging systems to perform diagnostic evaluations and minor procedures. Clinics serve as the first point of contact for patients experiencing neurological symptoms, where initial assessments and referrals to specialized hospitals are made. The use of neurointerventional devices in clinics allows for early detection and intervention, which is critical in preventing the progression of neurological conditions. Additionally, clinics provide post-procedure care and rehabilitation services to ensure patients achieve optimal recovery and quality of life. The collaboration between hospitals and clinics is essential in creating a seamless continuum of care for patients with neurological disorders. This integrated approach ensures that patients receive timely and appropriate interventions, from initial diagnosis to post-procedure follow-up. The Global Brain Neurointerventional Device Market is also witnessing an increasing adoption of telemedicine and remote monitoring technologies in both hospitals and clinics. These innovations enable healthcare providers to remotely assess and manage patients, particularly in rural and underserved areas where access to specialized care may be limited. The use of telemedicine in neurointerventional care has been particularly beneficial during the COVID-19 pandemic, allowing for continued patient care while minimizing the risk of virus transmission. Overall, the usage of neurointerventional devices in hospitals and clinics is transforming the landscape of neurological care, offering patients effective and minimally invasive treatment options for a wide range of brain conditions.

Global Brain Neurointerventional Device Market Outlook:

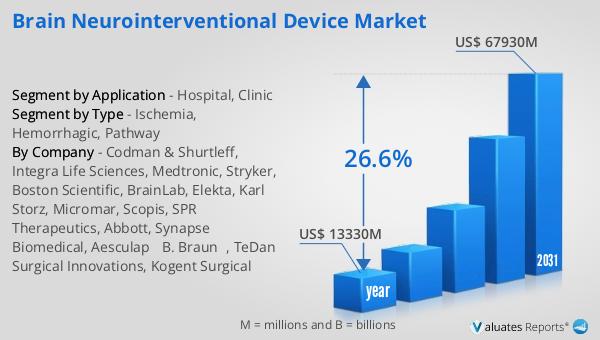

The global Brain Neurointerventional Device market was valued at US$ 6994.5 million in 2023 and is anticipated to reach US$ 44230 million by 2030, witnessing a CAGR of 26.6% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced neurointerventional devices and the rising prevalence of neurological disorders worldwide. The market's expansion is driven by several factors, including technological advancements in medical devices, growing awareness about minimally invasive procedures, and the aging population. As more healthcare providers adopt neurointerventional techniques, the market is expected to continue its upward trajectory, offering innovative solutions for the treatment of complex brain conditions. The substantial increase in market value over the forecast period underscores the importance of ongoing research and development efforts in this field. Companies are investing heavily in the development of new and improved neurointerventional devices to meet the evolving needs of patients and healthcare providers. The collaboration between medical device manufacturers, research institutions, and healthcare facilities is fostering innovation and accelerating the introduction of cutting-edge technologies in the market. As a result, the global Brain Neurointerventional Device market is poised for remarkable growth, providing effective and minimally invasive treatment options for patients with neurological disorders.

| Report Metric | Details |

| Report Name | Brain Neurointerventional Device Market |

| Accounted market size in 2023 | US$ 6994.5 million |

| Forecasted market size in 2030 | US$ 44230 million |

| CAGR | 26.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Codman & Shurtleff, Integra Life Sciences, Medtronic, Stryker, Boston Scientific, BrainLab, Elekta, Karl Storz, Micromar, Scopis, SPR Therapeutics, Abbott, Synapse Biomedical, Aesculap (B. Braun), TeDan Surgical Innovations, Kogent Surgical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |