What is Global Electric Vehicle Range Extender Market?

The Global Electric Vehicle Range Extender Market is a fascinating sector that's gaining momentum in the automotive industry. This market focuses on technologies and solutions designed to increase the driving range of electric vehicles (EVs), addressing one of the most significant barriers to EV adoption: range anxiety. Essentially, range extenders are additional power sources that allow electric vehicles to cover longer distances without needing a recharge. They come in various forms, including internal combustion engines (ICE), fuel cells, and other innovative technologies, each offering a unique approach to extending the driving range of EVs. As environmental concerns and advancements in technology push the automotive industry towards more sustainable solutions, the demand for electric vehicles with extended range capabilities is on the rise. This market segment is crucial for the continued growth and acceptance of electric vehicles, providing a bridge between the current limitations of EV technology and the future of fully electric, long-distance travel. The importance of this market cannot be overstated, as it not only contributes to the reduction of greenhouse gas emissions but also plays a significant role in the global shift towards cleaner, more sustainable transportation options.

ICE Range Extender, Fuel Cell Range Extender, Others in the Global Electric Vehicle Range Extender Market:

Diving into the specifics, the Global Electric Vehicle Range Extender Market is segmented into ICE Range Extender, Fuel Cell Range Extender, and others, each offering distinct advantages and catering to different needs within the electric vehicle industry. ICE Range Extenders use a conventional internal combustion engine to generate electricity, which in turn charges the EV's battery, extending the vehicle's range. This solution is particularly appealing for its familiarity and existing infrastructure, making it a practical short-term solution for extending EV range. On the other hand, Fuel Cell Range Extenders represent a more forward-looking approach, utilizing hydrogen fuel cells to produce electricity through a chemical reaction between hydrogen and oxygen. This method emits only water vapor, making it an incredibly clean solution that aligns well with the long-term goals of reducing carbon emissions and promoting sustainable energy sources. The "others" category encompasses a variety of emerging technologies, including but not limited to, battery swapping systems, solar panels, and auxiliary removable batteries, each offering innovative ways to address the range limitations of electric vehicles. The diversity within this market segment highlights the dynamic nature of the EV industry and the ongoing efforts to develop practical, efficient, and environmentally friendly solutions to one of the most pressing challenges facing electric vehicles today.

Passenger Cars, Commercial Vehicles in the Global Electric Vehicle Range Extender Market:

The usage of the Global Electric Vehicle Range Extender Market spans across passenger cars and commercial vehicles, each benefiting uniquely from the advancements in range extender technology. In passenger cars, range extenders significantly alleviate the concern of running out of battery power on long trips, making electric vehicles a more viable option for a broader range of consumers. This not only enhances the practicality of EVs for everyday use but also plays a crucial role in accelerating their adoption among the general public. For commercial vehicles, the implications are even more profound. Businesses that rely on transportation for logistics, deliveries, or services can leverage electric vehicles with range extenders to reduce operational costs and minimize their environmental impact. The ability to cover longer distances without the need for frequent recharging opens up new possibilities for efficiency and sustainability in commercial operations. Moreover, as cities and countries implement stricter emissions regulations, the adoption of electric commercial vehicles with range extenders becomes an increasingly attractive proposition for businesses aiming to comply with these standards while maintaining or even improving their service levels. The integration of range extenders into electric vehicles represents a significant step forward in making EVs a practical choice for both personal and commercial transportation, marking a pivotal moment in the journey towards a more sustainable automotive landscape.

Global Electric Vehicle Range Extender Market Outlook:

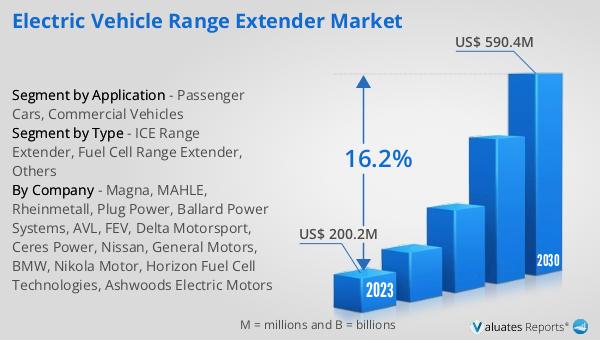

The market outlook for the Global Electric Vehicle Range Extender Market presents a promising future, with the market's value projected to escalate from US$ 200.2 million in 2023 to an impressive US$ 590.4 million by 2030. This growth trajectory, characterized by a compound annual growth rate (CAGR) of 16.2% during the forecast period from 2024 to 2030, underscores the increasing demand and potential for electric vehicle range extenders. This surge is indicative of the automotive industry's shift towards more sustainable and efficient transportation solutions, with range extenders playing a crucial role in mitigating one of the most significant hurdles to electric vehicle adoption: the anxiety over limited driving range. As technology advances and consumer awareness grows, the market for electric vehicle range extenders is set to expand, reflecting the broader trend towards electrification in the automotive sector. This optimistic outlook highlights the importance of continued innovation and investment in this area, as it holds the key to unlocking the full potential of electric vehicles, making them a more attractive and feasible option for a wider range of users across the globe.

| Report Metric | Details |

| Report Name | Electric Vehicle Range Extender Market |

| Accounted market size in 2023 | US$ 200.2 million |

| Forecasted market size in 2030 | US$ 590.4 million |

| CAGR | 16.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Magna, MAHLE, Rheinmetall, Plug Power, Ballard Power Systems, AVL, FEV, Delta Motorsport, Ceres Power, Nissan, General Motors, BMW, Nikola Motor, Horizon Fuel Cell Technologies, Ashwoods Electric Motors |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |