What is Global Laser Hair Loss Treatment Market?

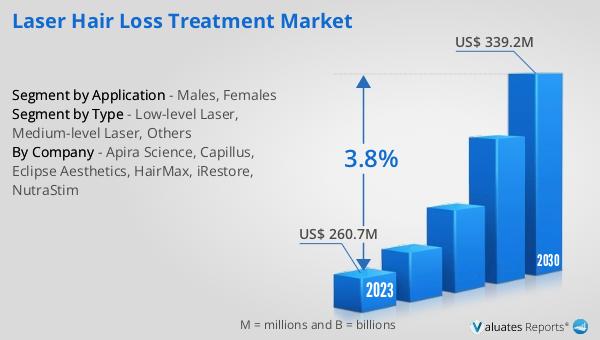

The Global Laser Hair Loss Treatment Market is an evolving sector that addresses a common concern among people worldwide: hair loss. This market focuses on innovative laser technologies designed to stimulate hair growth and reduce hair loss. Laser hair loss treatments use specific wavelengths of light to target hair follicles, promoting better blood flow and nutrient delivery to the scalp. This method is non-invasive, making it an attractive option for those seeking alternatives to surgical procedures or chemical treatments. As of 2023, the market was valued at US$ 260.7 million, showcasing its significant impact on the beauty and healthcare industries. With an expected growth to reach US$ 339.2 million by 2030, it's clear that this market is on an upward trajectory. This growth is driven by increasing awareness of hair loss issues, advancements in laser technology, and a growing acceptance of non-surgical treatment methods among both males and females. As research continues and technology advances, the Global Laser Hair Loss Treatment Market is set to offer more effective and accessible solutions for those looking to combat hair loss.

Low-level Laser, Medium-level Laser, Others in the Global Laser Hair Loss Treatment Market:

Diving into the specifics of the Global Laser Hair Loss Treatment Market, we find it segmented by the type of laser technology used, namely Low-level Laser, Medium-level Laser, and Others. Low-level laser therapy (LLLT) is a cornerstone of this market, utilizing red or near-infrared light to enhance scalp health and encourage hair growth without damaging the skin. This gentle approach is particularly appealing for its safety profile and efficacy in treating various stages of hair loss. Medium-level lasers, on the other hand, offer a more intense treatment option, targeting deeper layers of the scalp to stimulate hair follicles more aggressively. This category bridges the gap between mild and more severe hair loss treatments, providing a versatile solution for individuals with different needs. The "Others" segment includes emerging technologies and innovative approaches that are being developed to expand the market's offerings. Each of these segments plays a crucial role in the market's dynamics, catering to a wide range of consumers seeking effective hair loss solutions. With ongoing research and technological advancements, the landscape of laser hair loss treatments continues to evolve, promising more refined and targeted approaches to hair restoration in the future.

Males, Females in the Global Laser Hair Loss Treatment Market:

The usage of the Global Laser Hair Loss Treatment Market spans across two primary demographics: males and females, each facing unique challenges and seeking specific solutions for hair loss. For males, the market offers hope against common patterns of baldness, often linked to genetics and hormonal factors. Laser treatments for men are designed to slow down the shedding process, stimulate regrowth, and improve the overall health of the scalp. On the other hand, females experiencing hair thinning and loss due to hormonal changes, stress, or other factors find solace in these treatments as well. The non-invasive nature of laser therapy is particularly appealing, offering a painless and convenient option for women who are often more sensitive to the aesthetic implications of hair loss. The versatility of laser treatments, with options ranging from in-clinic sessions to at-home devices, ensures that both males and females can find a solution that fits their lifestyle and severity of hair loss. This broad applicability has significantly contributed to the market's growth, making laser hair loss treatments a popular choice for millions seeking to regain confidence and improve their appearance.

Global Laser Hair Loss Treatment Market Outlook:

The market outlook for the Global Laser Hair Loss Treatment sector presents a promising future. In 2023, the market's value was recorded at US$ 260.7 million, a figure that is expected to climb to US$ 339.2 million by the year 2030. This growth trajectory, marked by a Compound Annual Growth Rate (CAGR) of 3.8% from 2024 to 2030, underscores the increasing demand and confidence in laser-based treatments for hair loss. This optimistic forecast is fueled by several factors, including technological advancements in laser therapy, a growing global awareness of hair loss solutions, and a rising preference for non-invasive treatment options among the general population. As the market expands, it continues to offer new hope and solutions to individuals struggling with hair loss, reinforcing its position as a key player in the beauty and healthcare industries. This upward trend not only highlights the effectiveness of laser treatments in combating hair loss but also points to a future where these technologies become even more accessible and prevalent worldwide.

| Report Metric | Details |

| Report Name | Laser Hair Loss Treatment Market |

| Accounted market size in 2023 | US$ 260.7 million |

| Forecasted market size in 2030 | US$ 339.2 million |

| CAGR | 3.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Apira Science, Capillus, Eclipse Aesthetics, HairMax, iRestore, NutraStim |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |