What is Global Hypothermia Therapy Apparatus Market?

The Global Hypothermia Therapy Apparatus Market refers to the worldwide industry focused on the development, production, and distribution of devices designed to induce and maintain hypothermia in patients for therapeutic purposes. Hypothermia therapy, also known as targeted temperature management, involves lowering a patient's body temperature to help reduce the risk of ischemic injury to tissues following a period of insufficient blood flow. This technique is particularly useful in treating patients who have suffered cardiac arrest, stroke, or traumatic brain injury. The market encompasses a variety of apparatuses, including cooling blankets, ice packs, and advanced cooling systems that can precisely control body temperature. These devices are used in hospitals, clinics, and other healthcare settings to improve patient outcomes and reduce the risk of long-term neurological damage. The market is driven by advancements in medical technology, increasing awareness of the benefits of hypothermia therapy, and the growing prevalence of conditions that can benefit from this treatment.

Desktop, Portable in the Global Hypothermia Therapy Apparatus Market:

In the Global Hypothermia Therapy Apparatus Market, devices can be broadly categorized into desktop and portable types, each serving distinct needs and settings. Desktop hypothermia therapy apparatuses are typically larger, more complex systems designed for use in hospital settings where they can be integrated into existing medical infrastructure. These systems often feature advanced cooling technologies, such as water or air-based cooling, and can provide precise temperature control to ensure optimal therapeutic outcomes. They are usually equipped with sophisticated monitoring systems that allow healthcare professionals to continuously track a patient's temperature and adjust the cooling process as needed. Desktop systems are ideal for intensive care units (ICUs) and emergency departments where patients require constant monitoring and immediate intervention. On the other hand, portable hypothermia therapy apparatuses are designed for flexibility and ease of use in various settings, including ambulances, clinics, and even home care environments. These devices are typically smaller, lighter, and easier to transport, making them suitable for use in emergency situations where rapid cooling is necessary. Portable systems often use simpler cooling methods, such as ice packs or cooling pads, but some advanced models also incorporate sophisticated cooling technologies similar to their desktop counterparts. The portability of these devices allows for early intervention, which is crucial in improving patient outcomes, especially in cases of cardiac arrest or traumatic brain injury where time is of the essence. Both desktop and portable hypothermia therapy apparatuses play a crucial role in the overall market, catering to different needs and scenarios. Desktop systems are essential for providing comprehensive care in controlled environments, ensuring that patients receive the most effective and precise treatment possible. These systems are often used in conjunction with other advanced medical equipment, such as ventilators and monitoring devices, to provide a holistic approach to patient care. The integration of desktop hypothermia therapy apparatuses into hospital settings also facilitates research and development, allowing healthcare professionals to refine and improve treatment protocols based on real-world data and outcomes. Portable hypothermia therapy apparatuses, meanwhile, extend the reach of hypothermia therapy beyond the confines of the hospital. Their versatility and ease of use make them invaluable tools for first responders and healthcare providers in various settings. For instance, in emergency medical services (EMS), portable devices can be used to initiate cooling during patient transport, potentially improving outcomes by reducing the time to treatment. In clinics and home care settings, these devices provide a practical solution for patients who require ongoing temperature management but do not need to be hospitalized. The ability to deliver hypothermia therapy in diverse environments underscores the importance of portable apparatuses in the global market. In summary, the Global Hypothermia Therapy Apparatus Market is characterized by a range of devices designed to meet the needs of different healthcare settings. Desktop systems offer advanced, precise temperature control for critical care environments, while portable devices provide flexibility and rapid intervention capabilities for emergency and outpatient care. Both types of apparatuses are essential for delivering effective hypothermia therapy, improving patient outcomes, and expanding the reach of this life-saving treatment. As the market continues to evolve, advancements in technology and increased awareness of the benefits of hypothermia therapy will likely drive further innovation and adoption of both desktop and portable systems.

Hospital, Cnilic, Others in the Global Hypothermia Therapy Apparatus Market:

The usage of Global Hypothermia Therapy Apparatus Market spans across various healthcare settings, including hospitals, clinics, and other specialized environments. In hospitals, hypothermia therapy apparatuses are primarily used in intensive care units (ICUs) and emergency departments. These settings require advanced, reliable equipment to manage critically ill patients who have suffered from cardiac arrest, stroke, or traumatic brain injury. In the ICU, hypothermia therapy is often part of a comprehensive treatment plan that includes other life-support measures such as mechanical ventilation and continuous monitoring. The precise temperature control offered by advanced hypothermia therapy systems is crucial in these settings, as it allows healthcare professionals to maintain the patient's body temperature within a narrow therapeutic range, thereby minimizing the risk of further injury and improving overall outcomes. Clinics also utilize hypothermia therapy apparatuses, albeit on a smaller scale compared to hospitals. In these settings, the focus is often on providing early intervention and ongoing care for patients who may not require hospitalization but still benefit from temperature management. Portable hypothermia therapy devices are particularly useful in clinics, as they offer the flexibility needed to treat patients in various stages of recovery. For example, a patient who has been discharged from the hospital but still requires temperature management can receive treatment in a clinic setting, reducing the need for readmission and allowing for more efficient use of healthcare resources. Clinics may also use hypothermia therapy apparatuses for outpatient procedures that involve a risk of ischemic injury, providing an added layer of protection for patients undergoing such treatments. Beyond hospitals and clinics, hypothermia therapy apparatuses find applications in other specialized environments, including ambulances, sports facilities, and even home care settings. In emergency medical services (EMS), portable hypothermia therapy devices are invaluable tools for first responders. These devices can be used to initiate cooling during patient transport, potentially improving outcomes by reducing the time to treatment. For instance, in cases of cardiac arrest, early initiation of hypothermia therapy can help preserve neurological function and increase the chances of survival. Similarly, in sports facilities, hypothermia therapy apparatuses can be used to treat athletes who suffer from heat stroke or other conditions that require rapid cooling. The portability and ease of use of these devices make them ideal for such applications, where immediate intervention is crucial. In home care settings, hypothermia therapy apparatuses provide a practical solution for patients who require ongoing temperature management but do not need to be hospitalized. These devices allow patients to receive treatment in the comfort of their own homes, improving their quality of life and reducing the burden on healthcare facilities. Home care providers can use portable hypothermia therapy devices to manage conditions such as multiple sclerosis or other neurological disorders that benefit from temperature regulation. The ability to deliver hypothermia therapy in a home setting also supports the trend towards more personalized and patient-centered care, allowing for tailored treatment plans that meet the unique needs of each patient. In summary, the Global Hypothermia Therapy Apparatus Market serves a wide range of healthcare settings, from hospitals and clinics to specialized environments like ambulances and home care. In hospitals, advanced hypothermia therapy systems are essential for managing critically ill patients in ICUs and emergency departments. Clinics benefit from the flexibility of portable devices, which allow for early intervention and ongoing care. Specialized environments such as EMS and sports facilities rely on portable hypothermia therapy apparatuses for rapid, on-the-spot treatment. Finally, home care settings offer a practical solution for patients requiring long-term temperature management, supporting a more personalized approach to healthcare. The diverse applications of hypothermia therapy apparatuses highlight their importance in improving patient outcomes and expanding the reach of this life-saving treatment.

Global Hypothermia Therapy Apparatus Market Outlook:

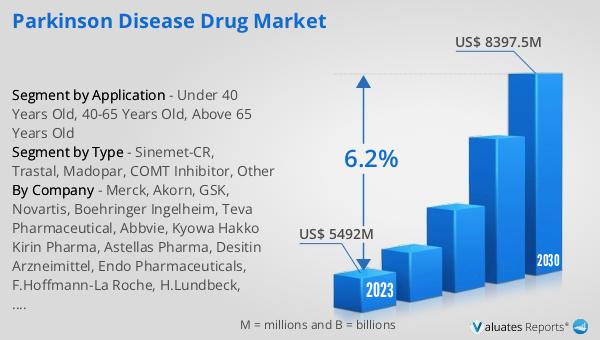

The global pharmaceutical market was valued at approximately 1,475 billion USD in 2022, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth trajectory underscores the robust expansion and increasing demand within the pharmaceutical sector. In comparison, the chemical drug market has shown a steady increase, growing from 1,005 billion USD in 2018 to an estimated 1,094 billion USD in 2022. This comparison highlights the significant role that chemical drugs continue to play within the broader pharmaceutical landscape. The growth in both markets reflects ongoing advancements in medical research, the development of new therapies, and the increasing global demand for effective healthcare solutions. These trends are indicative of a dynamic and evolving industry that is poised for continued growth and innovation.

| Report Metric | Details |

| Report Name | Hypothermia Therapy Apparatus Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Hirtz, Zhuhai Hema Medical Instrument, Zhuhai Hokai, Zhuhai Funiya Medical, Suzhou Zede Medical Equipment, Anhui USTC Zonkia Scientific Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

https://reports.valuates.com/market-reports/QYRE-Auto-6T17609/global-99-8-ammonium-nitrate-pure

https://reports.valuates.com/market-reports/QYRE-Auto-6T17609/global-99-8-ammonium-nitrate-pure