What is Global 3D-printed Medical Devices Market?

The Global 3D-printed Medical Devices Market is a rapidly evolving sector within the healthcare industry. This market involves the use of 3D printing technology to create medical devices that are tailored to the specific needs of patients. These devices can range from surgical instruments to implants and prosthetics. The technology allows for high precision and customization, which is particularly beneficial in medical applications where individual patient anatomy can vary significantly. The market is driven by advancements in 3D printing technology, increasing demand for personalized medical care, and the growing prevalence of chronic diseases that require long-term medical devices. Additionally, the ability to produce complex structures that are difficult or impossible to create using traditional manufacturing methods is a significant advantage. This market is not only transforming the way medical devices are produced but also improving patient outcomes by providing more effective and personalized treatment options. The global reach of this market means that innovations and advancements are being shared and implemented worldwide, leading to a more interconnected and advanced healthcare system.

Surgical Equipment, Organoids, Orthopedic Implants, Dental Implants, Other in the Global 3D-printed Medical Devices Market:

The Global 3D-printed Medical Devices Market encompasses a wide range of applications, including surgical equipment, organoids, orthopedic implants, dental implants, and other specialized devices. Surgical equipment produced through 3D printing includes instruments like forceps, hemostats, and scalpel handles, which can be customized to fit the surgeon's hand perfectly, enhancing precision and comfort during procedures. Organoids, which are miniature, simplified versions of organs created from stem cells, are another groundbreaking application. These can be used for research, drug testing, and even as a potential source for organ transplants in the future. Orthopedic implants, such as joint replacements and bone scaffolds, benefit immensely from 3D printing as it allows for the creation of implants that match the patient's anatomy precisely, reducing the risk of complications and improving recovery times. Dental implants, including crowns, bridges, and dentures, are another significant area where 3D printing is making a substantial impact. The technology allows for the rapid production of highly accurate and customized dental prosthetics, improving the fit and comfort for patients. Other applications of 3D-printed medical devices include custom prosthetics, hearing aids, and even bioprinted tissues and organs. The ability to produce these devices quickly and accurately is revolutionizing the medical field, providing patients with better, more personalized care. The versatility of 3D printing technology means that it can be applied to a wide range of medical needs, from simple surgical tools to complex organ structures, making it an invaluable tool in modern medicine.

Hospitals, Clinics, Other in the Global 3D-printed Medical Devices Market:

The usage of Global 3D-printed Medical Devices Market in hospitals, clinics, and other healthcare settings is transforming patient care and medical practices. In hospitals, 3D-printed medical devices are used extensively for surgical planning and execution. Surgeons can create precise models of a patient's anatomy to plan complex surgeries, reducing the risk of errors and improving outcomes. Custom surgical instruments and implants tailored to the patient's specific needs are also produced, enhancing the precision and effectiveness of surgical procedures. In clinics, 3D-printed devices are used for a variety of applications, including dental prosthetics, orthopedic braces, and hearing aids. The ability to produce these devices quickly and accurately means that patients can receive their custom-fitted devices in a shorter time frame, improving their overall experience and satisfaction. Additionally, clinics can use 3D printing technology to create models for patient education, helping them to better understand their conditions and treatment options. Other healthcare settings, such as research institutions and specialized medical centers, also benefit from the advancements in 3D printing technology. Researchers can create organoids and other complex structures for studying diseases and testing new treatments, accelerating the pace of medical research and innovation. Specialized medical centers can produce custom prosthetics and implants for patients with unique needs, providing them with better, more personalized care. The versatility and precision of 3D printing technology make it an invaluable tool in a wide range of healthcare settings, improving patient outcomes and advancing medical practices.

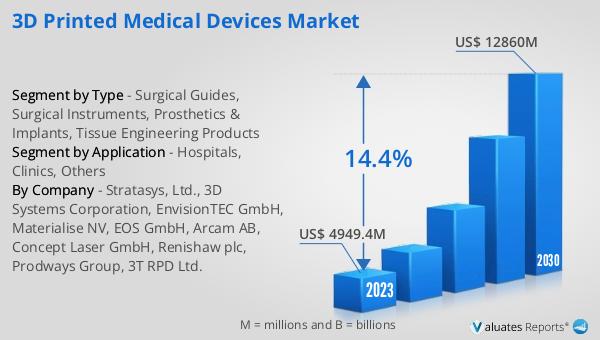

Global 3D-printed Medical Devices Market Outlook:

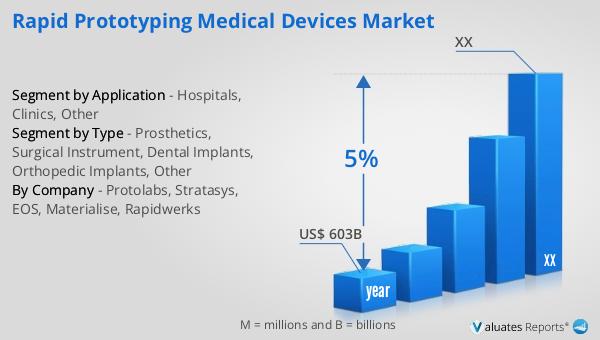

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This significant market size underscores the critical role that medical devices play in the healthcare industry. The steady growth rate reflects ongoing advancements in medical technology, increasing demand for healthcare services, and the continuous need for innovative solutions to address various medical conditions. The expansion of this market is driven by factors such as the aging global population, the rising prevalence of chronic diseases, and the increasing adoption of advanced medical devices in both developed and developing regions. As the market continues to grow, it is expected to bring about significant improvements in patient care, enhance the efficiency of healthcare delivery, and contribute to the overall advancement of the medical field. The projected growth also highlights the importance of continued investment in research and development to drive innovation and meet the evolving needs of patients and healthcare providers worldwide.

| Report Metric | Details |

| Report Name | 3D-printed Medical Devices Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Medtronic, Materialise, Stryker, Zimmer Biomet, Johnson & Johnson, Renishaw, Formlabs, Stratasys |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |