What is Global Angiography Machine Market?

The Global Angiography Machine Market refers to the worldwide industry focused on the production, distribution, and utilization of angiography machines. These machines are essential in medical imaging, allowing healthcare professionals to visualize the inside of blood vessels and organs, primarily to identify blockages or abnormalities. Angiography machines use various imaging techniques, such as X-ray, CT (Computed Tomography), and MRI (Magnetic Resonance Imaging), to provide detailed images of the vascular system. The market encompasses a wide range of products, including traditional X-ray angiography machines, advanced CT and MRI angiography systems, and hybrid machines that combine multiple imaging modalities. The demand for these machines is driven by the increasing prevalence of cardiovascular diseases, technological advancements in imaging techniques, and the growing need for minimally invasive diagnostic procedures. The market is also influenced by factors such as healthcare infrastructure development, government initiatives to improve healthcare services, and the rising awareness about early diagnosis and treatment of vascular diseases.

X-ray Angiography, CT Angiography, Magnetic Resonance Angiography, MR-CT Angiography in the Global Angiography Machine Market:

X-ray Angiography, CT Angiography, Magnetic Resonance Angiography, and MR-CT Angiography are different types of imaging techniques used in the Global Angiography Machine Market. X-ray Angiography is the traditional method that uses X-rays to visualize blood vessels. It involves injecting a contrast dye into the bloodstream and taking X-ray images to detect blockages or abnormalities. This technique is widely used due to its high-resolution images and relatively low cost. CT Angiography, on the other hand, uses computed tomography to create detailed cross-sectional images of blood vessels. It also involves the use of a contrast dye but provides more detailed images compared to X-ray angiography. CT Angiography is particularly useful for detecting aneurysms, blood clots, and other vascular conditions. Magnetic Resonance Angiography (MRA) uses magnetic fields and radio waves to create detailed images of blood vessels without the need for a contrast dye. MRA is non-invasive and provides high-resolution images, making it ideal for patients who are allergic to contrast dyes. MR-CT Angiography combines the benefits of both MRI and CT imaging techniques. It provides highly detailed images of blood vessels and surrounding tissues, making it useful for complex cases where precise imaging is required. The Global Angiography Machine Market includes a wide range of machines that cater to these different imaging techniques, each with its own advantages and applications. The choice of technique depends on various factors, including the patient's condition, the area being examined, and the specific requirements of the healthcare provider.

Cardiology, Oncology, Neurology, Peripheral Vascular Intervention in the Global Angiography Machine Market:

The Global Angiography Machine Market finds extensive usage in various medical fields, including Cardiology, Oncology, Neurology, and Peripheral Vascular Intervention. In Cardiology, angiography machines are used to diagnose and treat heart-related conditions such as coronary artery disease, heart attacks, and congenital heart defects. These machines help cardiologists visualize the coronary arteries and identify blockages or abnormalities that may require intervention, such as angioplasty or stent placement. In Oncology, angiography machines are used to detect and monitor tumors and other cancer-related conditions. They help oncologists visualize the blood supply to tumors, which is crucial for planning treatments such as surgery, radiation therapy, or chemotherapy. In Neurology, angiography machines are used to diagnose and treat conditions affecting the brain and spinal cord. They help neurologists visualize blood vessels in the brain and detect abnormalities such as aneurysms, arteriovenous malformations, and strokes. This information is vital for planning surgical interventions or other treatments. In Peripheral Vascular Intervention, angiography machines are used to diagnose and treat conditions affecting blood vessels outside the heart and brain, such as peripheral artery disease, deep vein thrombosis, and varicose veins. These machines help vascular surgeons visualize the affected blood vessels and plan appropriate interventions, such as angioplasty, stent placement, or surgical bypass. The use of angiography machines in these medical fields has significantly improved the diagnosis and treatment of various vascular conditions, leading to better patient outcomes and reduced healthcare costs.

Global Angiography Machine Market Outlook:

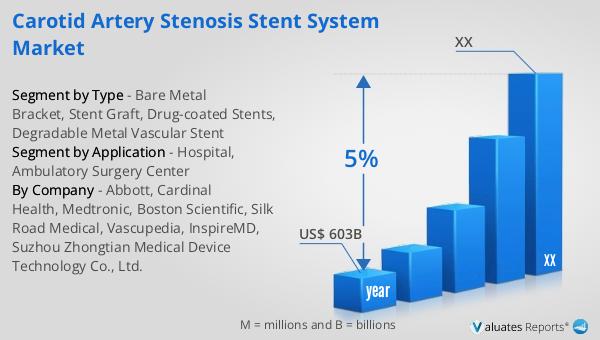

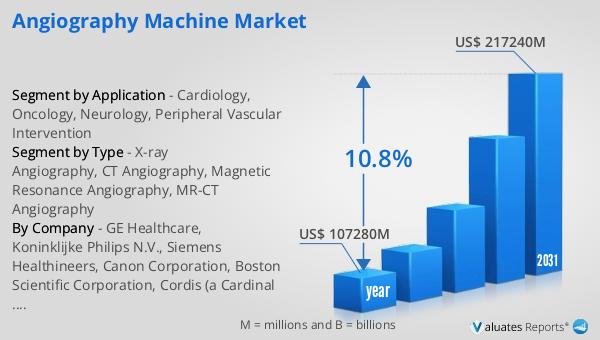

The global Angiography Machine market was valued at US$ 83,570 million in 2023 and is anticipated to reach US$ 180,580 million by 2030, witnessing a CAGR of 10.8% during the forecast period 2024-2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% during the next six years. This significant growth in the angiography machine market can be attributed to the increasing prevalence of cardiovascular diseases, advancements in imaging technology, and the growing demand for minimally invasive diagnostic procedures. The market is also driven by the development of healthcare infrastructure, government initiatives to improve healthcare services, and the rising awareness about early diagnosis and treatment of vascular diseases. The adoption of advanced angiography machines in various medical fields, such as cardiology, oncology, neurology, and peripheral vascular intervention, has further fueled the market growth. The increasing focus on research and development activities, along with strategic collaborations and partnerships among key market players, is expected to create new opportunities for market expansion. Overall, the global angiography machine market is poised for substantial growth in the coming years, driven by technological advancements, increasing healthcare expenditure, and the rising demand for advanced diagnostic and therapeutic solutions.

| Report Metric | Details |

| Report Name | Angiography Machine Market |

| Accounted market size in 2023 | US$ 83570 million |

| Forecasted market size in 2030 | US$ 180580 million |

| CAGR | 10.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | GE Healthcare, Koninklijke Philips N.V., Siemens Healthineers, Canon Corporation, Boston Scientific Corporation, Cordis (a Cardinal Health Company, U.S.), Shimadzu Corporation, Medtronic, Braun Melsungen, Abbott Laboratories, Terumo |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |