What is Global Diaphragm Pumps Market?

The Global Diaphragm Pumps Market refers to the worldwide industry focused on the production, distribution, and utilization of diaphragm pumps. These pumps are a type of positive displacement pump that uses a combination of the reciprocating action of a rubber, thermoplastic, or Teflon diaphragm and suitable valves on either side of the diaphragm to pump a fluid. Diaphragm pumps are known for their versatility and are used in a wide range of applications, including water and wastewater treatment, oil and gas, chemicals, and food and beverages. They are particularly valued for their ability to handle a variety of fluids, including those that are viscous, abrasive, or corrosive. The market is driven by the increasing demand for efficient and reliable pumping solutions across various industries, as well as advancements in pump technology that enhance performance and durability. The global market is characterized by a diverse range of products and a competitive landscape with numerous players striving to innovate and capture market share.

Air Operated, Electrically Operated, Others in the Global Diaphragm Pumps Market:

In the Global Diaphragm Pumps Market, diaphragm pumps can be categorized based on their mode of operation into air-operated, electrically operated, and others. Air-operated diaphragm pumps, also known as AODD pumps, are powered by compressed air and are widely used due to their ability to handle a variety of fluids, including those with high viscosity or containing solids. They are particularly popular in industries where electricity is not readily available or where explosion-proof equipment is required, such as in the chemical and oil and gas industries. Electrically operated diaphragm pumps, on the other hand, are powered by an electric motor. These pumps are known for their efficiency and are often used in applications where a consistent and reliable power source is available. They are commonly found in water and wastewater treatment plants, as well as in the food and beverage industry, where precise control over the pumping process is essential. The "others" category includes diaphragm pumps that are powered by hydraulic or manual means. Hydraulic diaphragm pumps are typically used in high-pressure applications, while manual diaphragm pumps are often used in smaller-scale or portable applications. Each type of diaphragm pump has its own set of advantages and is chosen based on the specific requirements of the application. The versatility and adaptability of diaphragm pumps make them a valuable asset in a wide range of industries, contributing to the growth and development of the global diaphragm pumps market.

Water & Wastewater, Oil & Gas, Chemicals, Food & Beverages, Others in the Global Diaphragm Pumps Market:

The usage of diaphragm pumps in the Global Diaphragm Pumps Market spans several key areas, including water and wastewater, oil and gas, chemicals, food and beverages, and others. In the water and wastewater sector, diaphragm pumps are used for various applications such as sludge transfer, chemical dosing, and dewatering. Their ability to handle abrasive and corrosive fluids makes them ideal for these tasks. In the oil and gas industry, diaphragm pumps are used for transferring crude oil, injecting chemicals, and handling drilling mud. Their robust construction and ability to operate in hazardous environments make them a preferred choice in this sector. In the chemical industry, diaphragm pumps are used for transferring and dosing a wide range of chemicals, including acids, alkalis, and solvents. Their ability to handle aggressive and hazardous fluids safely and efficiently is a key advantage. In the food and beverage industry, diaphragm pumps are used for transferring and dosing ingredients, as well as for cleaning and sanitizing processes. Their sanitary design and ability to handle viscous and shear-sensitive fluids make them suitable for these applications. Other areas where diaphragm pumps are used include pharmaceuticals, mining, and construction. In the pharmaceutical industry, diaphragm pumps are used for transferring and dosing active ingredients and solvents. In the mining industry, they are used for dewatering and transferring slurries. In the construction industry, diaphragm pumps are used for dewatering and transferring concrete. The versatility and reliability of diaphragm pumps make them a valuable tool in a wide range of applications, contributing to the growth and development of the global diaphragm pumps market.

Global Diaphragm Pumps Market Outlook:

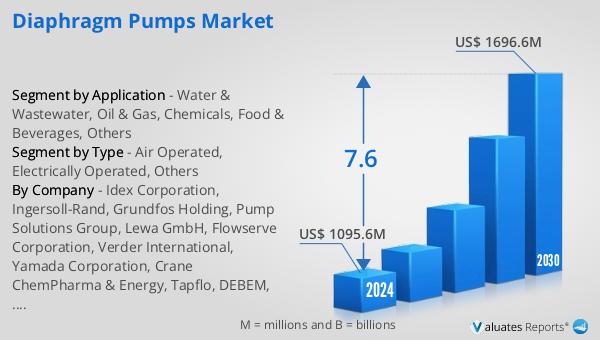

The global diaphragm pumps market is anticipated to expand from USD 1,095.6 million in 2024 to USD 1,696.6 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 7.6% over the forecast period. The market is dominated by the top four players, who collectively hold over 47% of the market share. Idex Corporation stands as the largest producer, commanding approximately 19% of the market. The Asia-Pacific region is the largest market for diaphragm pumps, accounting for about 42% of the global share, followed by North America and Europe, which hold shares of approximately 24% and 22%, respectively. When it comes to product types, air-operated diaphragm pumps represent the largest segment, making up about 80% of the market. In terms of application, the water and wastewater sector is the most significant, constituting around 30% of the market. These figures highlight the robust growth and widespread adoption of diaphragm pumps across various industries and regions.

| Report Metric | Details |

| Report Name | Diaphragm Pumps Market |

| Accounted market size in 2024 | US$ 1095.6 million |

| Forecasted market size in 2030 | US$ 1696.6 million |

| CAGR | 7.6 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Idex Corporation, Ingersoll-Rand, Grundfos Holding, Pump Solutions Group, Lewa GmbH, Flowserve Corporation, Verder International, Yamada Corporation, Crane ChemPharma & Energy, Tapflo, DEBEM, Xylem |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |