What is Global Onshore Wind Turbine(Above 2.5MW) Market?

The Global Onshore Wind Turbine Market, specifically focusing on turbines with a capacity above 2.5MW, represents a significant segment within the renewable energy sector. This market encompasses the development, manufacturing, and installation of wind turbines on land, rather than offshore locations, with each unit capable of generating more than 2.5 megawatts of power. These turbines are designed to harness wind energy and convert it into electricity, contributing to the global efforts of reducing carbon emissions and promoting sustainable energy sources. The importance of this market lies in its potential to provide large-scale, renewable power solutions that can support the energy needs of various regions around the world. With advancements in technology and increasing governmental support for green energy, the onshore wind turbine market is poised for substantial growth. This segment plays a crucial role in the transition towards more sustainable energy systems, offering a cleaner alternative to fossil fuels and helping to mitigate the impacts of climate change.

Horizontal Axis Wind Turbine, Vertical Axis Wind Turbine in the Global Onshore Wind Turbine(Above 2.5MW) Market:

In the realm of the Global Onshore Wind Turbine Market, particularly turbines with a capacity above 2.5MW, two main types stand out: Horizontal Axis Wind Turbines (HAWTs) and Vertical Axis Wind Turbines (VAWTs). HAWTs, the more common of the two, feature blades that rotate around a horizontal axis. These turbines are typically mounted on a tower to capture the higher wind speeds available at greater heights, making them highly efficient for onshore wind projects. Their design allows for larger blade sizes, which translates to a higher power output, suitable for the demands of the above 2.5MW market segment. On the other hand, VAWTs rotate around a vertical axis and are considered less common in large-scale wind projects. Despite this, they offer unique advantages, such as the ability to catch wind from any direction without the need for yaw mechanisms and potentially lower maintenance costs since their main components can be located at ground level. Each type of turbine has its specific applications and benefits within the onshore wind energy sector, influenced by factors such as local wind conditions, land availability, and installation costs. The choice between HAWTs and VAWTs for projects within the Global Onshore Wind Turbine Market is determined by a combination of efficiency, cost-effectiveness, and environmental considerations, ensuring that each installation maximizes its potential for clean energy production.

Below 3 MW, 3-4 MW, Above 4 MW in the Global Onshore Wind Turbine(Above 2.5MW) Market:

The Global Onshore Wind Turbine Market, focusing on turbines with a capacity above 2.5MW, finds its application across various power output ranges, including below 3 MW, 3-4 MW, and above 4 MW categories. Turbines below 3 MW are typically suited for smaller onshore projects or those in regions with lower wind speeds, offering a balance between efficiency and adaptability to diverse environmental conditions. This category serves as an entry point for communities and businesses looking to invest in wind energy without the need for large-scale infrastructure. Moving up, the 3-4 MW range represents the mid-tier of the market, catering to a broad spectrum of onshore wind projects. These turbines are designed for higher efficiency and are often utilized in areas with moderate to high wind speeds, making them a popular choice for commercial wind farms. They strike a balance between power output and cost, providing a viable option for many developers. Lastly, turbines with a capacity of above 4 MW are at the forefront of wind technology, engineered for maximum efficiency and output. These are typically deployed in large-scale projects with the aim of maximizing energy production from each turbine. They are most suitable for areas with consistently high wind speeds and represent the cutting edge in wind turbine technology, pushing the boundaries of what is possible in onshore wind energy generation. Each category plays a vital role in the diversification and growth of the Global Onshore Wind Turbine Market, offering solutions tailored to varying needs and conditions.

Global Onshore Wind Turbine(Above 2.5MW) Market Outlook:

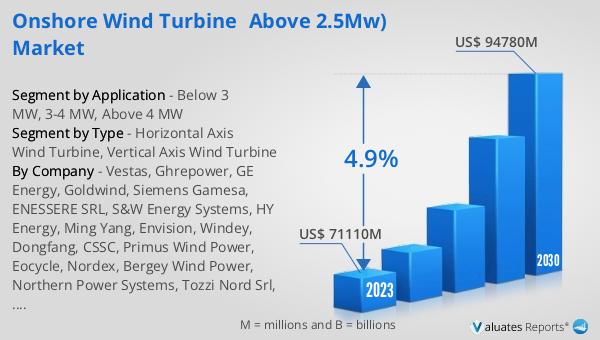

The market outlook for the Global Onshore Wind Turbine Market, specifically for turbines with a capacity above 2.5MW, presents a promising future. In 2023, the market's value stood at approximately 71,110 million US dollars. Looking ahead, projections indicate a growth trajectory that could see the market's worth escalate to around 94,780 million US dollars by the year 2030. This anticipated growth, marked by a compound annual growth rate (CAGR) of 4.9% over the period from 2024 to 2030, underscores the increasing demand and positive sentiment towards onshore wind energy solutions. Such growth is reflective of the global shift towards sustainable energy sources, with onshore wind turbines playing a pivotal role in this transition. The expansion of the market is supported by technological advancements, favorable government policies, and an increasing awareness of the need to transition away from fossil fuels to combat climate change. This outlook highlights the significant potential for investment and development within the onshore wind sector, pointing towards a future where wind energy is a cornerstone of global energy systems.

| Report Metric | Details |

| Report Name | Onshore Wind Turbine(Above 2.5MW) Market |

| Accounted market size in 2023 | US$ 71110 million |

| Forecasted market size in 2030 | US$ 94780 million |

| CAGR | 4.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Vestas, Ghrepower, GE Energy, Goldwind, Siemens Gamesa, ENESSERE SRL, S&W Energy Systems, HY Energy, Ming Yang, Envision, Windey, Dongfang, CSSC, Primus Wind Power, Eocycle, Nordex, Bergey Wind Power, Northern Power Systems, Tozzi Nord Srl, Xzeres Wind, Enercon, Gamesa |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |