What is Global Glass Frit for Sealing Market?

The Global Glass Frit for Sealing Market is a specialized segment within the broader glass industry, focusing on the production and application of glass frits used for sealing purposes. Glass frits are finely ground glass powders that, when heated, melt and form a glassy layer, creating a seal between different materials. This market is driven by the demand for reliable and durable sealing solutions in various industries, including electronics, automotive, and renewable energy. The unique properties of glass frits, such as their ability to withstand high temperatures and provide excellent adhesion, make them ideal for applications where traditional sealing methods may fail. The market is characterized by a diverse range of products, each tailored to specific temperature requirements and applications. As industries continue to innovate and seek more efficient and sustainable solutions, the demand for glass frits for sealing is expected to grow, driven by advancements in technology and the increasing need for high-performance materials. The market's growth is also supported by the expansion of key industries in regions like Asia Pacific, where manufacturing and technological development are rapidly advancing.

Tg Below 430℃, Tg 430℃-500℃, Tg Above 500℃ in the Global Glass Frit for Sealing Market:

In the Global Glass Frit for Sealing Market, products are often categorized based on their glass transition temperature (Tg), which is a critical factor in determining their suitability for various applications. Tg Below 430℃ refers to glass frits that have a lower melting point, making them ideal for applications where lower processing temperatures are required. These frits are often used in industries where thermal sensitivity is a concern, such as in certain electronics and delicate components. The lower Tg allows for effective sealing without compromising the integrity of the materials being joined. On the other hand, Tg 430℃-500℃ glass frits are designed for applications that require a balance between thermal resistance and processing flexibility. This category is particularly popular in the electronics and semiconductor industries, where components must withstand moderate temperatures without degrading. The versatility of these frits makes them suitable for a wide range of applications, providing reliable seals in environments where both performance and cost-effectiveness are important. Lastly, Tg Above 500℃ glass frits are engineered for high-temperature applications, where durability and resistance to extreme conditions are paramount. These frits are commonly used in industries such as automotive and renewable energy, where components are exposed to harsh environments and must maintain their integrity over time. The ability of these frits to withstand high temperatures without losing their sealing properties makes them indispensable in applications where failure is not an option. Each of these categories plays a crucial role in the Global Glass Frit for Sealing Market, catering to the diverse needs of industries that rely on advanced materials for their operations. As technology continues to evolve, the demand for specialized glass frits is expected to increase, driving innovation and growth within the market.

Electronics & Semiconductors, LED & OLED, Home Appliances, Solar & Fuel Cells, Others in the Global Glass Frit for Sealing Market:

The usage of Global Glass Frit for Sealing Market products spans several key industries, each benefiting from the unique properties of glass frits. In the Electronics & Semiconductors sector, glass frits are essential for creating hermetic seals that protect sensitive components from environmental factors such as moisture and dust. The ability of glass frits to form strong, durable seals ensures the longevity and reliability of electronic devices, making them a critical component in the manufacturing process. Similarly, in the LED & OLED industry, glass frits are used to seal light-emitting components, enhancing their performance and lifespan. The precise sealing capabilities of glass frits help maintain the integrity of these components, ensuring consistent light output and energy efficiency. In the realm of Home Appliances, glass frits are employed to seal various components, providing thermal and chemical resistance that enhances the durability and safety of appliances. The use of glass frits in this industry contributes to the development of high-quality, long-lasting products that meet consumer demands for reliability and performance. In the Solar & Fuel Cells sector, glass frits play a crucial role in sealing photovoltaic cells and fuel cell components, protecting them from environmental degradation and ensuring optimal performance. The ability of glass frits to withstand harsh conditions and provide effective seals is vital for the efficiency and longevity of renewable energy systems. Lastly, in other industries, glass frits are used in a variety of applications, from automotive to aerospace, where their unique properties provide solutions to complex sealing challenges. The versatility and effectiveness of glass frits make them an indispensable material in the development of advanced technologies across multiple sectors.

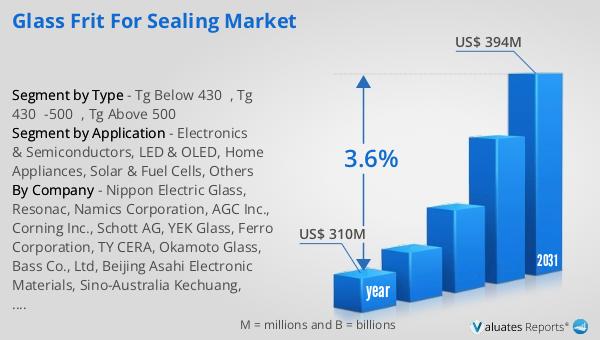

Global Glass Frit for Sealing Market Outlook:

The global market for Glass Frit for Sealing was valued at approximately US$ 310 million in 2024, with projections indicating a growth to around US$ 394 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.6% over the forecast period. The market is dominated by the top three manufacturers, who collectively hold about 40% of the market share. The Asia Pacific region emerges as the largest market for Glass Frit for Sealing, accounting for over 50% of the global share. This dominance is attributed to the region's robust manufacturing sector and technological advancements. In terms of product segmentation, the Tg 430℃-500℃ category holds a significant portion, with a share exceeding 55%. This segment's prominence is due to its versatility and suitability for a wide range of applications, particularly in the electronics and semiconductor industries. Speaking of applications, the Electronics & Semiconductors sector is the largest consumer of glass frits for sealing, with a share of over 55%. This sector's reliance on glass frits is driven by the need for reliable and durable sealing solutions that ensure the performance and longevity of electronic components. The market's growth is supported by ongoing technological advancements and the increasing demand for high-performance materials across various industries.

| Report Metric | Details |

| Report Name | Glass Frit for Sealing Market |

| Accounted market size in year | US$ 310 million |

| Forecasted market size in 2031 | US$ 394 million |

| CAGR | 3.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Nippon Electric Glass, Resonac, Namics Corporation, AGC Inc., Corning Inc., Schott AG, YEK Glass, Ferro Corporation, TY CERA, Okamoto Glass, Bass Co., Ltd, Beijing Asahi Electronic Materials, Sino-Australia Kechuang, Anywhere Powder |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |