What is Global Mannitol Powder Market?

The Global Mannitol Powder Market is a segment of the broader sugar alcohol market, focusing on the production and distribution of mannitol powder. Mannitol is a type of sugar alcohol used as a low-calorie sweetener and is known for its unique properties, such as being non-hygroscopic, which means it does not absorb moisture from the air. This makes it particularly useful in various applications, including food, pharmaceuticals, and industrial uses. The market for mannitol powder is driven by its demand in the food industry as a sugar substitute, especially in products aimed at diabetic and health-conscious consumers. Additionally, its role in the pharmaceutical industry as an excipient and in medical applications, such as a diuretic and renal diagnostic aid, further fuels its market growth. The global market is characterized by a diverse range of applications and a steady demand across different regions, with manufacturers focusing on innovation and sustainability to meet the evolving needs of consumers and industries. As a result, the Global Mannitol Powder Market continues to expand, offering opportunities for growth and development in various sectors.

Food Grade, Industrial Grade in the Global Mannitol Powder Market:

In the Global Mannitol Powder Market, the product is categorized into different grades based on its intended use, primarily food grade and industrial grade. Food grade mannitol powder is extensively used in the food and beverage industry due to its sweetening properties and low-calorie content. It is particularly popular in sugar-free and low-calorie products, catering to the growing demand for healthier food options. Mannitol's non-hygroscopic nature makes it ideal for use in products like chewing gum, candies, and baked goods, where moisture control is crucial. Additionally, it is used as a bulking agent and stabilizer in various food products, enhancing texture and shelf life. The food grade segment is driven by the increasing consumer preference for low-calorie and sugar-free products, as well as the rising awareness of health and wellness. On the other hand, industrial grade mannitol powder finds its applications in a variety of non-food industries. In the pharmaceutical industry, it is used as an excipient in tablet formulations, providing bulk and stability to the final product. Its osmotic diuretic properties make it valuable in medical applications, such as reducing intracranial pressure and treating acute renal failure. The industrial grade segment also includes applications in the chemical industry, where mannitol is used as a precursor for the synthesis of various chemical compounds. Furthermore, it is employed in the production of resins and plastics, where it acts as a plasticizer, improving the flexibility and durability of the final product. The demand for both food grade and industrial grade mannitol powder is influenced by various factors, including technological advancements, regulatory frameworks, and consumer preferences. Manufacturers are focusing on improving production processes to enhance the quality and efficiency of mannitol powder, ensuring compliance with stringent regulatory standards. The market is also witnessing a shift towards sustainable and eco-friendly production methods, driven by the increasing emphasis on environmental conservation and corporate social responsibility. In conclusion, the Global Mannitol Powder Market is segmented into food grade and industrial grade, each catering to specific applications and industries. The food grade segment is driven by the demand for low-calorie and sugar-free products, while the industrial grade segment finds its applications in pharmaceuticals, chemicals, and other industries. The market is characterized by continuous innovation and development, with manufacturers striving to meet the evolving needs of consumers and industries. As the demand for mannitol powder continues to grow, the market offers significant opportunities for growth and expansion across various sectors.

Bioindustry and Fermentation, Plant Care, Food, Other in the Global Mannitol Powder Market:

The Global Mannitol Powder Market finds its applications in various areas, including bioindustry and fermentation, plant care, food, and other sectors. In the bioindustry and fermentation sector, mannitol powder is used as a carbon source in microbial fermentation processes. It serves as a substrate for the production of various biochemicals and biofuels, contributing to the development of sustainable and eco-friendly production methods. Mannitol's role in fermentation processes is crucial, as it enhances the efficiency and yield of the final product, making it a valuable component in the bioindustry. In plant care, mannitol powder is used as a plant growth regulator and osmoprotectant. It helps plants to cope with abiotic stress conditions, such as drought and salinity, by stabilizing cellular structures and maintaining osmotic balance. Mannitol's ability to improve plant resilience and productivity makes it an essential component in agricultural practices, particularly in regions prone to adverse environmental conditions. Its application in plant care is driven by the increasing need for sustainable and efficient agricultural practices, aimed at enhancing crop yield and quality. In the food industry, mannitol powder is widely used as a sugar substitute and bulking agent. Its low-calorie content and non-hygroscopic nature make it ideal for use in sugar-free and low-calorie products, catering to the growing demand for healthier food options. Mannitol is used in a variety of food products, including chewing gum, candies, baked goods, and dairy products, where it enhances texture, stability, and shelf life. The food industry's demand for mannitol powder is driven by the increasing consumer preference for low-calorie and sugar-free products, as well as the rising awareness of health and wellness. Apart from these sectors, mannitol powder is also used in other applications, such as pharmaceuticals and cosmetics. In the pharmaceutical industry, it is used as an excipient in tablet formulations, providing bulk and stability to the final product. Its osmotic diuretic properties make it valuable in medical applications, such as reducing intracranial pressure and treating acute renal failure. In the cosmetics industry, mannitol is used as a humectant and moisturizer, enhancing the texture and feel of cosmetic products. In summary, the Global Mannitol Powder Market is characterized by its diverse applications across various sectors, including bioindustry and fermentation, plant care, food, and other industries. Its role in enhancing efficiency, productivity, and sustainability makes it a valuable component in these sectors, driving the demand for mannitol powder. As the market continues to grow, it offers significant opportunities for innovation and development, catering to the evolving needs of consumers and industries.

Global Mannitol Powder Market Outlook:

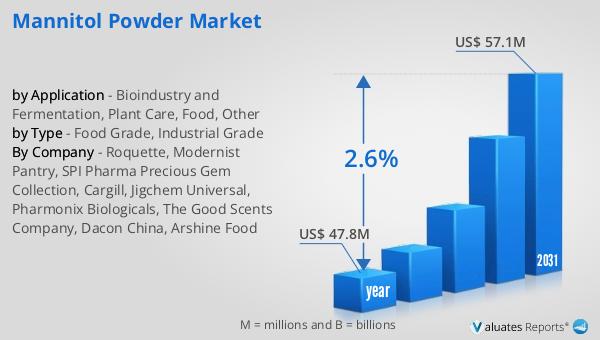

The outlook for the Global Mannitol Powder Market indicates a steady growth trajectory over the coming years. In 2024, the market was valued at approximately $47.8 million. By 2031, it is anticipated to expand to a revised valuation of $57.1 million. This growth is expected to occur at a compound annual growth rate (CAGR) of 2.6% throughout the forecast period. This steady increase reflects the rising demand for mannitol powder across various industries, driven by its unique properties and diverse applications. The market's growth is supported by the increasing consumer preference for low-calorie and sugar-free products, as well as the expanding applications of mannitol powder in pharmaceuticals, bioindustry, and other sectors. As manufacturers continue to innovate and develop new applications for mannitol powder, the market is poised for further expansion, offering opportunities for growth and development in various sectors. The Global Mannitol Powder Market's outlook is positive, with a focus on sustainability, innovation, and meeting the evolving needs of consumers and industries.

| Report Metric | Details |

| Report Name | Mannitol Powder Market |

| Accounted market size in year | US$ 47.8 million |

| Forecasted market size in 2031 | US$ 57.1 million |

| CAGR | 2.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Roquette, Modernist Pantry, SPI Pharma Precious Gem Collection, Cargill, Jigchem Universal, Pharmonix Biologicals, The Good Scents Company, Dacon China, Arshine Food |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |