What is Global Dual Tech Occupancy Sensors Market?

The Global Dual Tech Occupancy Sensors Market is a rapidly evolving segment within the broader field of smart building technologies. These sensors are designed to enhance energy efficiency and improve the automation of lighting systems by detecting the presence or absence of people in a given space. Dual technology sensors typically combine passive infrared (PIR) and ultrasonic sensing technologies to accurately determine occupancy. This combination allows for more reliable detection, reducing false positives and negatives that can occur when using a single technology. The market for these sensors is driven by the increasing demand for energy-efficient solutions in both residential and commercial buildings. As energy costs rise and environmental concerns become more pressing, building owners and managers are increasingly looking for ways to reduce energy consumption. Dual tech occupancy sensors offer a practical solution by ensuring that lights and other systems are only active when needed. This not only helps in cutting down electricity bills but also contributes to the sustainability goals of organizations. The market is also influenced by advancements in sensor technology, which have made these devices more affordable and easier to integrate into existing building management systems. As a result, the adoption of dual tech occupancy sensors is expected to grow steadily in the coming years.

Ceiling Mount Occupancy Sensors, Wall Mount Occupancy Sensors in the Global Dual Tech Occupancy Sensors Market:

Ceiling mount occupancy sensors and wall mount occupancy sensors are two prevalent types of devices within the Global Dual Tech Occupancy Sensors Market, each offering unique advantages and applications. Ceiling mount occupancy sensors are typically installed on the ceiling of a room or space, providing a wide coverage area that can effectively monitor large spaces such as open-plan offices, conference rooms, and classrooms. These sensors are particularly useful in environments where the layout is open and unobstructed, allowing the sensor to detect motion across a broad area. The ceiling mount design ensures that the sensor has a clear line of sight to detect movement, which is crucial for accurate occupancy detection. Additionally, ceiling mount sensors are often equipped with advanced features such as adjustable sensitivity and time delay settings, allowing users to customize the sensor's performance to suit specific needs. On the other hand, wall mount occupancy sensors are installed on the walls of a room and are ideal for spaces where ceiling installation is not feasible or where targeted detection is required. These sensors are often used in smaller rooms, corridors, and restrooms, where the sensor can be positioned to monitor specific areas. Wall mount sensors are designed to detect motion within a defined range, making them suitable for applications where precise detection is necessary. Both ceiling and wall mount sensors utilize dual technology, combining passive infrared (PIR) and ultrasonic sensing to enhance accuracy and reliability. PIR sensors detect the heat emitted by moving objects, while ultrasonic sensors emit sound waves that bounce off objects and return to the sensor, allowing it to detect motion. The combination of these technologies ensures that the sensors can accurately detect occupancy, even in challenging environments with varying temperatures and obstructions. The choice between ceiling and wall mount sensors depends on the specific requirements of the space and the desired coverage area. In some cases, a combination of both types of sensors may be used to achieve optimal coverage and detection accuracy. The versatility and adaptability of these sensors make them a valuable addition to any building management system, providing energy savings and improved automation. As the demand for energy-efficient solutions continues to grow, the market for ceiling and wall mount occupancy sensors is expected to expand, driven by advancements in sensor technology and increasing awareness of the benefits of smart building solutions.

Residential, Non-residential in the Global Dual Tech Occupancy Sensors Market:

The Global Dual Tech Occupancy Sensors Market finds significant applications in both residential and non-residential settings, each with its unique requirements and benefits. In residential areas, dual tech occupancy sensors are primarily used to enhance energy efficiency and convenience. Homeowners can install these sensors in various rooms, such as living rooms, bedrooms, and bathrooms, to automate lighting and HVAC systems. By detecting the presence or absence of occupants, the sensors can automatically turn lights on or off, adjust heating or cooling settings, and even control other smart home devices. This automation not only reduces energy consumption but also adds a layer of convenience for homeowners, who no longer need to manually control these systems. Additionally, dual tech occupancy sensors can contribute to home security by detecting unexpected movement and triggering alarms or notifications. In non-residential settings, such as commercial buildings, offices, and educational institutions, the use of dual tech occupancy sensors is driven by the need for energy savings and improved building management. In office environments, these sensors can be used to control lighting and HVAC systems in individual workspaces, conference rooms, and common areas. By ensuring that these systems are only active when needed, businesses can significantly reduce their energy costs and carbon footprint. In educational institutions, occupancy sensors can be used to manage lighting and climate control in classrooms, lecture halls, and libraries, providing a comfortable learning environment while minimizing energy waste. The sensors can also be integrated with building management systems to provide data on space utilization, helping facility managers optimize the use of available resources. In both residential and non-residential applications, the adoption of dual tech occupancy sensors is supported by the growing awareness of the environmental and economic benefits of energy-efficient solutions. As energy costs continue to rise and sustainability becomes a priority for many organizations, the demand for these sensors is expected to increase. The versatility and reliability of dual tech occupancy sensors make them an attractive option for a wide range of applications, from small homes to large commercial complexes. By providing accurate occupancy detection and seamless integration with existing systems, these sensors offer a practical solution for reducing energy consumption and enhancing the overall efficiency of buildings.

Global Dual Tech Occupancy Sensors Market Outlook:

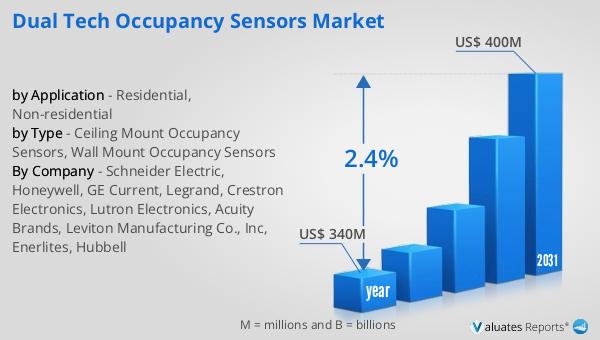

The outlook for the Global Dual Tech Occupancy Sensors Market indicates a steady growth trajectory over the coming years. In 2024, the market was valued at approximately $340 million, and it is anticipated to expand to a revised size of $400 million by 2031. This growth represents a compound annual growth rate (CAGR) of 2.4% during the forecast period. The market's expansion is driven by several factors, including the increasing demand for energy-efficient solutions and the growing awareness of the benefits of smart building technologies. As energy costs continue to rise and environmental concerns become more pressing, building owners and managers are increasingly looking for ways to reduce energy consumption and improve sustainability. Dual tech occupancy sensors offer a practical solution by ensuring that lights and other systems are only active when needed, helping to cut down electricity bills and contribute to sustainability goals. Additionally, advancements in sensor technology have made these devices more affordable and easier to integrate into existing building management systems, further driving their adoption. The market's growth is also supported by the increasing adoption of smart home and building automation systems, which rely on accurate occupancy detection to optimize energy use and enhance convenience. As the demand for these solutions continues to grow, the Global Dual Tech Occupancy Sensors Market is expected to expand, providing opportunities for manufacturers and suppliers to innovate and meet the evolving needs of consumers.

| Report Metric | Details |

| Report Name | Dual Tech Occupancy Sensors Market |

| Accounted market size in year | US$ 340 million |

| Forecasted market size in 2031 | US$ 400 million |

| CAGR | 2.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Schneider Electric, Honeywell, GE Current, Legrand, Crestron Electronics, Lutron Electronics, Acuity Brands, Leviton Manufacturing Co., Inc, Enerlites, Hubbell |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |