What is Global Wafer CMP Retainer Rings Market?

The Global Wafer CMP Retainer Rings Market is a specialized segment within the semiconductor industry, focusing on the components used in the chemical mechanical planarization (CMP) process. CMP is a critical step in semiconductor manufacturing, where it is used to smooth and flatten the wafer surface, ensuring that subsequent layers are applied evenly. Retainer rings play a crucial role in this process by holding the wafer in place during polishing, preventing slippage, and ensuring uniform pressure distribution. These rings are typically made from high-performance materials that can withstand the rigorous conditions of the CMP process, such as high temperatures and abrasive environments. The market for these retainer rings is driven by the increasing demand for semiconductors across various industries, including consumer electronics, automotive, and telecommunications. As technology advances, the need for more precise and efficient manufacturing processes grows, further fueling the demand for high-quality CMP retainer rings. The market is characterized by continuous innovation, with manufacturers striving to develop rings that offer improved durability, performance, and compatibility with various wafer sizes and materials. This market's growth is closely tied to the overall health of the semiconductor industry, making it a vital component of the global technology landscape.

Polyphenylene Sulfide (PPS), Polyetheretherketone (PEEK), Polyethylene Terephthalate (PET), Others in the Global Wafer CMP Retainer Rings Market:

Polyphenylene Sulfide (PPS), Polyetheretherketone (PEEK), and Polyethylene Terephthalate (PET) are among the key materials used in the manufacturing of CMP retainer rings, each offering unique properties that make them suitable for different applications within the Global Wafer CMP Retainer Rings Market. PPS is a high-performance thermoplastic known for its exceptional chemical resistance, dimensional stability, and ability to withstand high temperatures. These properties make PPS an ideal choice for CMP retainer rings, as it can endure the harsh conditions of the CMP process without degrading. PPS rings are often used in applications where chemical exposure is a concern, providing reliable performance and longevity. PEEK, on the other hand, is renowned for its outstanding mechanical properties, including high strength, stiffness, and resistance to wear and fatigue. This makes PEEK an excellent material for retainer rings that require superior durability and performance under mechanical stress. PEEK rings are particularly favored in high-precision applications where maintaining tight tolerances is critical. PET, a more cost-effective option, offers good chemical resistance and mechanical properties, making it suitable for less demanding applications. While PET may not match the performance of PPS or PEEK in extreme conditions, it provides a viable alternative for applications where cost is a primary consideration. In addition to these materials, other advanced polymers and composites are also used in the production of CMP retainer rings, each selected based on the specific requirements of the application. The choice of material is influenced by factors such as the type of wafer being processed, the specific CMP process parameters, and the desired balance between performance and cost. As the semiconductor industry continues to evolve, the demand for materials that can meet the increasingly stringent requirements of CMP processes is expected to grow, driving further innovation and development in the Global Wafer CMP Retainer Rings Market.

300 mm Wafer, 200 mm Wafer, Others in the Global Wafer CMP Retainer Rings Market:

The usage of Global Wafer CMP Retainer Rings Market in different wafer sizes, such as 300 mm and 200 mm wafers, as well as other sizes, highlights the versatility and adaptability of these components in semiconductor manufacturing. The 300 mm wafer, being the largest standard size used in the industry, requires retainer rings that can accommodate its dimensions while ensuring precise and uniform polishing. The larger surface area of 300 mm wafers means that any imperfections during the CMP process can have a more significant impact on the final product, making the role of retainer rings even more critical. These rings must provide consistent pressure distribution and prevent any slippage or misalignment during polishing, ensuring that the wafer surface is perfectly planar. The demand for 300 mm wafers is driven by the need for higher production efficiency and cost-effectiveness, as larger wafers allow for more chips to be produced per batch. In contrast, 200 mm wafers, while smaller, still play a vital role in the semiconductor industry, particularly in the production of specialized and legacy devices. Retainer rings for 200 mm wafers must be designed to offer the same level of precision and reliability as those used for larger wafers, albeit on a smaller scale. The continued use of 200 mm wafers in certain applications underscores the importance of having a diverse range of retainer rings that can cater to different wafer sizes and manufacturing needs. Beyond the standard 300 mm and 200 mm wafers, the Global Wafer CMP Retainer Rings Market also addresses the requirements of other wafer sizes, which may be used in niche or emerging applications. These include smaller wafers used in research and development or specialized manufacturing processes, where the focus may be on innovation and experimentation rather than mass production. The ability to provide retainer rings for a wide range of wafer sizes demonstrates the market's commitment to supporting the diverse needs of the semiconductor industry. As technology continues to advance and new applications for semiconductors emerge, the demand for CMP retainer rings that can accommodate various wafer sizes and process requirements is expected to grow, further solidifying their role as an essential component in semiconductor manufacturing.

Global Wafer CMP Retainer Rings Market Outlook:

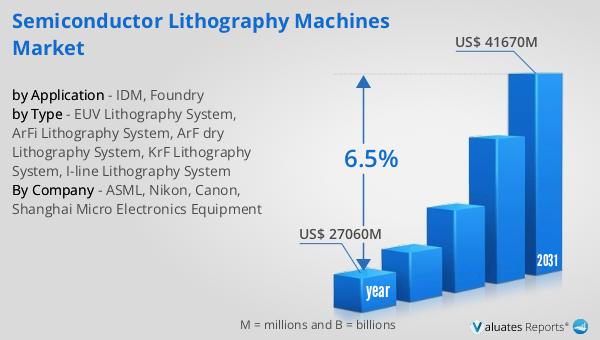

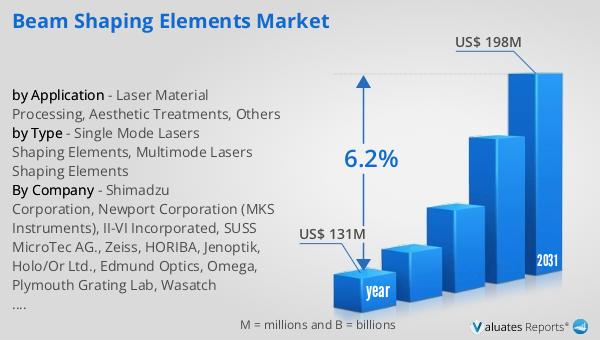

In 2024, the global market for Wafer CMP Retainer Rings was valued at approximately US$ 105 million, with projections indicating a growth to around US$ 162 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.5% over the forecast period. Despite this overall growth, the largest regional market, Asia Pacific, experienced a decline of 2.0%. In contrast, the Americas saw a significant increase in sales, reaching US$ 142.1 billion, which marked a 17.0% year-on-year growth. Similarly, Europe and Japan also experienced positive growth, with sales in Europe reaching US$ 53.8 billion, up 12.6% year-on-year, and sales in Japan totaling US$ 48.1 billion, reflecting a 10.0% year-on-year increase. However, the Asia Pacific region, despite being the largest market, saw a decline in sales, totaling US$ 336.2 billion, down 2.0% year-on-year. This mixed performance across different regions highlights the varying dynamics and challenges faced by the Global Wafer CMP Retainer Rings Market. Factors such as regional economic conditions, technological advancements, and shifts in semiconductor manufacturing trends all play a role in influencing market performance. As the industry continues to evolve, understanding these regional differences will be crucial for stakeholders looking to navigate the complexities of the global market.

| Report Metric | Details |

| Report Name | Wafer CMP Retainer Rings Market |

| Accounted market size in year | US$ 105 million |

| Forecasted market size in 2031 | US$ 162 million |

| CAGR | 6.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Akashi, Ensigner, Mitsubishi Chemical Advanced Materials, SPM Technology, SemPlastic, LLC, Victrex, Willbe S&T, TAK Materials Corporation, UIS Technologies, Calitech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |