What is Global 3D TSV Package Market?

The Global 3D TSV (Through-Silicon Via) Package Market is a rapidly evolving sector within the semiconductor industry, focusing on advanced packaging technologies that enhance the performance and efficiency of electronic devices. This market revolves around the use of TSV technology, which involves creating vertical electrical connections through silicon wafers, enabling the stacking of multiple semiconductor dies. This approach significantly improves the speed, power efficiency, and miniaturization of electronic components, making it a crucial innovation for modern electronics. The 3D TSV technology is particularly beneficial for applications requiring high bandwidth and low power consumption, such as smartphones, data centers, and high-performance computing. As the demand for more compact and efficient electronic devices continues to rise, the Global 3D TSV Package Market is poised for substantial growth. This growth is driven by the increasing adoption of advanced technologies like artificial intelligence, the Internet of Things (IoT), and 5G, which require more sophisticated and efficient semiconductor solutions. The market's expansion is further supported by ongoing research and development efforts aimed at overcoming technical challenges and reducing production costs, making 3D TSV technology more accessible to a broader range of applications and industries.

Via-First, Via-Middle, Via-Last in the Global 3D TSV Package Market:

In the realm of 3D TSV packaging, the processes of Via-First, Via-Middle, and Via-Last play pivotal roles, each offering distinct advantages and challenges. Via-First is a process where the TSVs are created before the front-end-of-line (FEOL) processes, which include the formation of transistors and other active components. This approach allows for better alignment and integration of the TSVs with the active devices, leading to improved electrical performance. However, it can be challenging to manage the thermal and mechanical stresses introduced during subsequent processing steps. Via-Middle, on the other hand, involves creating the TSVs after the FEOL processes but before the back-end-of-line (BEOL) processes, which include the formation of interconnects and other passive components. This method strikes a balance between the alignment benefits of Via-First and the flexibility of Via-Last, allowing for more efficient integration of the TSVs with both active and passive components. Via-Middle is often favored for its ability to optimize the trade-offs between performance, cost, and complexity. Lastly, Via-Last is a process where the TSVs are created after the BEOL processes, making it the most flexible approach in terms of integration with existing manufacturing processes. This method is particularly advantageous for applications where the TSVs need to be added to existing designs without significant modifications. However, it can introduce additional challenges in terms of alignment and electrical performance, as the TSVs must be carefully integrated with the existing interconnects and other components. Each of these processes has its own set of advantages and challenges, and the choice of process depends on the specific requirements of the application, including factors such as performance, cost, and manufacturing complexity. As the Global 3D TSV Package Market continues to evolve, these processes will play a crucial role in enabling the development of more advanced and efficient semiconductor solutions.

Logic and Memory Devices, MEMS and Sensors, Power and Analog Components, Other in the Global 3D TSV Package Market:

The Global 3D TSV Package Market finds extensive applications across various domains, including Logic and Memory Devices, MEMS and Sensors, Power and Analog Components, and other areas. In the realm of Logic and Memory Devices, 3D TSV technology is instrumental in enhancing the performance and efficiency of processors and memory modules. By enabling the stacking of multiple dies, TSVs allow for increased bandwidth and reduced latency, which are critical for high-performance computing applications. This technology is particularly beneficial for data centers and cloud computing environments, where the demand for faster and more efficient processing capabilities is ever-increasing. In MEMS and Sensors, 3D TSV technology facilitates the integration of multiple sensor components into a single package, reducing size and improving performance. This is especially important for applications in consumer electronics, automotive, and industrial sectors, where compact and efficient sensor solutions are in high demand. For Power and Analog Components, 3D TSV technology enables the development of more efficient power management solutions by allowing for the integration of multiple power components into a single package. This results in improved power efficiency and reduced heat generation, which are crucial for applications in mobile devices, automotive, and industrial electronics. Additionally, 3D TSV technology is finding increasing use in other areas, such as RF components and optoelectronics, where the need for compact and efficient solutions is driving the adoption of advanced packaging technologies. As the Global 3D TSV Package Market continues to grow, its applications across these diverse domains will expand, driven by the increasing demand for more efficient and compact electronic solutions.

Global 3D TSV Package Market Outlook:

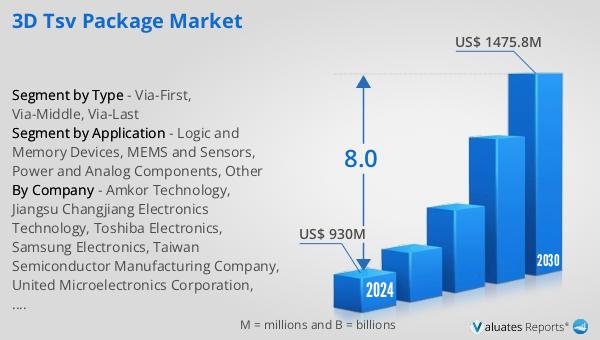

The outlook for the Global 3D TSV Package Market is promising, with projections indicating significant growth in the coming years. The market is expected to expand from approximately $930 million in 2024 to around $1,475.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 8.0% during this period. This growth is indicative of the increasing demand for advanced semiconductor packaging solutions that offer improved performance and efficiency. The broader semiconductor market, which was valued at approximately $579 billion in 2022, is also projected to grow, reaching an estimated $790 billion by 2029, with a CAGR of 6% during the forecast period. This growth in the semiconductor market underscores the rising demand for more sophisticated and efficient electronic components, driven by advancements in technologies such as artificial intelligence, the Internet of Things (IoT), and 5G. As these technologies continue to evolve, the need for more advanced packaging solutions like 3D TSV will become increasingly critical, driving further growth in the market. The expansion of the Global 3D TSV Package Market is also supported by ongoing research and development efforts aimed at overcoming technical challenges and reducing production costs, making this technology more accessible to a wider range of applications and industries.

| Report Metric | Details |

| Report Name | 3D TSV Package Market |

| Accounted market size in 2024 | US$ 930 million |

| Forecasted market size in 2030 | US$ 1475.8 million |

| CAGR | 8.0 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Amkor Technology, Jiangsu Changjiang Electronics Technology, Toshiba Electronics, Samsung Electronics, Taiwan Semiconductor Manufacturing Company, United Microelectronics Corporation, Xilinx, Teledyne DALSA, Tezzaron Semiconductor Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |