What is Global eMMC Storage Chips Market?

The Global eMMC Storage Chips Market refers to the worldwide industry focused on the production and distribution of embedded MultiMediaCard (eMMC) storage chips. These chips are a type of flash memory used primarily in portable electronic devices to store data. eMMC storage chips integrate the flash memory and the flash memory controller into a single package, simplifying the design and reducing the cost of devices. They are widely used in smartphones, tablets, smart TVs, and other consumer electronics due to their compact size, reliability, and ease of integration. The market for eMMC storage chips is driven by the increasing demand for high-performance, cost-effective storage solutions in various applications, including automotive and industrial sectors. As technology advances and the need for more storage capacity grows, the global eMMC storage chips market continues to expand, offering new opportunities for manufacturers and suppliers.

≤16GB, 32GB, 64GB, 128GB, ≥256GB in the Global eMMC Storage Chips Market:

In the Global eMMC Storage Chips Market, storage capacities are categorized into several segments: ≤16GB, 32GB, 64GB, 128GB, and ≥256GB. Each of these segments caters to different needs and applications. The ≤16GB segment is typically used in entry-level smartphones, basic tablets, and other low-cost devices where high storage capacity is not a primary requirement. These chips offer sufficient space for operating systems, essential applications, and basic user data. The 32GB segment is more common in mid-range smartphones and tablets, providing a balance between cost and storage capacity. This capacity is suitable for users who need more space for apps, photos, and videos but do not require extensive storage. The 64GB segment is popular in higher-end smartphones, tablets, and some smart TVs, offering ample space for a larger number of applications, high-resolution photos, and HD videos. This capacity is ideal for users who frequently download apps, games, and media content. The 128GB segment is often found in premium smartphones, tablets, and advanced smart TVs, providing substantial storage for users who need to store large amounts of data, including 4K videos, high-resolution images, and extensive app libraries. Finally, the ≥256GB segment caters to high-end devices and specialized applications, such as flagship smartphones, high-performance tablets, and automotive systems. These chips offer vast storage capacity, suitable for professional use, extensive media libraries, and advanced applications that require significant data storage. As the demand for higher storage capacities continues to grow, manufacturers are focusing on developing eMMC storage chips with larger capacities and improved performance to meet the evolving needs of consumers and industries.

Smartphones, Tablets, Smart TVs, Smart Wear, Automotive, Others in the Global eMMC Storage Chips Market:

The usage of Global eMMC Storage Chips Market spans across various areas, including smartphones, tablets, smart TVs, smart wear, automotive, and others. In smartphones, eMMC storage chips are essential for storing the operating system, applications, photos, videos, and other user data. They provide a reliable and cost-effective storage solution, enabling manufacturers to produce affordable yet high-performing devices. In tablets, eMMC storage chips offer similar benefits, allowing users to store a wide range of content, from apps and games to movies and documents. The compact size and integrated design of eMMC chips make them ideal for slim and lightweight tablets. Smart TVs also utilize eMMC storage chips to store the operating system, apps, and user data, ensuring smooth performance and quick access to content. The high storage capacity of eMMC chips allows smart TVs to support a wide range of applications and services, enhancing the user experience. In smart wear, such as smartwatches and fitness trackers, eMMC storage chips provide the necessary storage for operating systems, apps, and user data, while maintaining a compact and energy-efficient design. The automotive sector is another significant area of usage for eMMC storage chips. Modern vehicles rely on these chips for various applications, including infotainment systems, navigation, and advanced driver-assistance systems (ADAS). The reliability and durability of eMMC storage chips make them suitable for the demanding automotive environment. Other areas of usage include industrial applications, where eMMC storage chips are used in embedded systems, IoT devices, and other electronic equipment that require reliable and compact storage solutions. The versatility and wide range of applications for eMMC storage chips highlight their importance in the modern digital world.

Global eMMC Storage Chips Market Outlook:

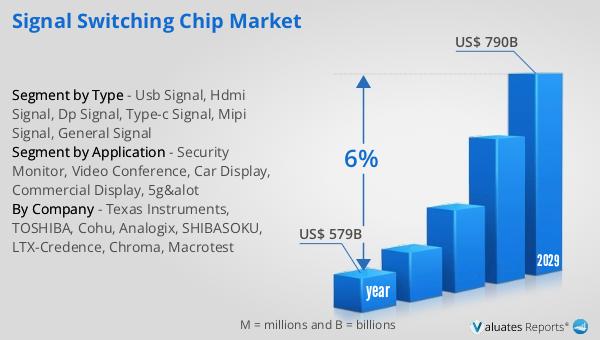

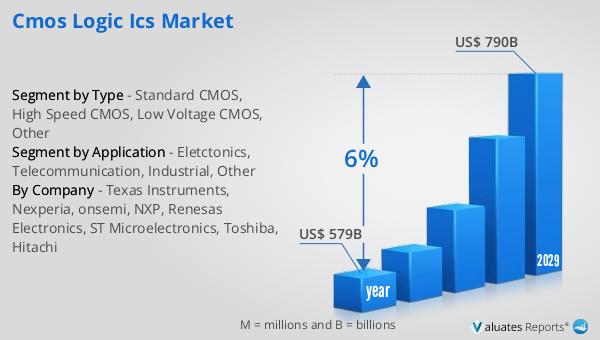

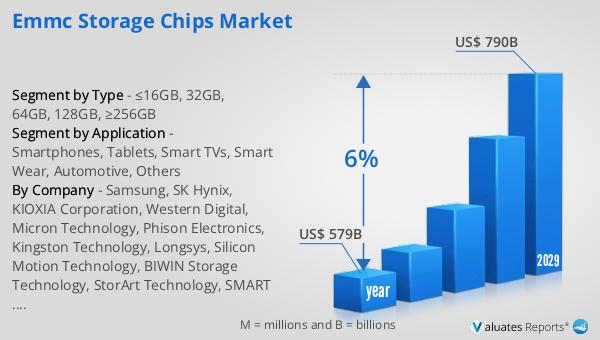

The global market for semiconductors was valued at approximately US$ 579 billion in 2022 and is anticipated to reach around US$ 790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is driven by the increasing demand for advanced electronic devices and the continuous innovation in semiconductor technology. The expanding applications of semiconductors in various industries, including consumer electronics, automotive, healthcare, and industrial sectors, contribute significantly to this market growth. As the world becomes more connected and reliant on digital technologies, the need for efficient and high-performance semiconductors continues to rise. The semiconductor market's robust growth trajectory underscores the critical role these components play in the development and functioning of modern electronic devices and systems.

| Report Metric | Details |

| Report Name | eMMC Storage Chips Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Samsung, SK Hynix, KIOXIA Corporation, Western Digital, Micron Technology, Phison Electronics, Kingston Technology, Longsys, Silicon Motion Technology, BIWIN Storage Technology, StorArt Technology, SMART Global Holdings, Transcend Information, Swissbit, Flexxon, Greenliant Systems, ATP Electronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |