What is Cashless Self-Checkout Devices - Global Market?

Cashless self-checkout devices are revolutionizing the retail landscape by offering a seamless and efficient shopping experience. These devices allow customers to scan, bag, and pay for their purchases without the need for a cashier, using digital payment methods such as credit cards, mobile wallets, or contactless payment systems. The global market for these devices is expanding rapidly as retailers seek to enhance customer satisfaction and reduce operational costs. With the rise of e-commerce and the increasing demand for quick and convenient shopping experiences, cashless self-checkout devices are becoming a staple in various retail environments. They not only streamline the checkout process but also help in managing store traffic, reducing wait times, and minimizing human errors. As technology continues to advance, these devices are expected to become more sophisticated, offering features like AI-driven product recognition and personalized shopping experiences. Retailers are increasingly adopting these systems to stay competitive and meet the evolving expectations of tech-savvy consumers. The global market for cashless self-checkout devices is poised for significant growth, driven by the widespread adoption of digital payment solutions and the ongoing shift towards automation in the retail sector.

Vertical Type, Desktop Type in the Cashless Self-Checkout Devices - Global Market:

In the realm of cashless self-checkout devices, two prominent types are the vertical type and the desktop type, each catering to different retail needs and environments. Vertical type devices are typically designed to be integrated into the store's existing infrastructure, often resembling traditional checkout lanes but without the need for a cashier. These devices are ideal for larger retail spaces like supermarkets and hypermarkets, where they can handle a high volume of transactions efficiently. They are equipped with advanced scanning technology, large touchscreens, and multiple payment options, allowing customers to complete their purchases quickly and independently. Vertical type devices are often preferred in settings where space is not a constraint, and there is a need to manage large crowds effectively. On the other hand, desktop type cashless self-checkout devices are compact and versatile, making them suitable for smaller retail environments such as convenience stores and boutique shops. These devices are designed to sit on a countertop, offering a space-saving solution that still provides the full functionality of a self-checkout system. Desktop type devices are equipped with user-friendly interfaces, intuitive navigation, and support for various digital payment methods, ensuring a smooth and hassle-free checkout experience for customers. They are particularly beneficial in stores with limited floor space, where maximizing every inch is crucial. Both vertical and desktop type devices are integral to the global market for cashless self-checkout systems, each offering unique advantages that cater to different retail scenarios. As retailers continue to embrace digital transformation, the demand for these devices is expected to grow, driven by the need for efficient, customer-centric solutions that enhance the shopping experience. The choice between vertical and desktop type devices often depends on factors such as store size, customer volume, and specific operational requirements. Retailers must carefully evaluate their needs and choose the type of device that best aligns with their business goals and customer expectations. As technology evolves, both vertical and desktop type cashless self-checkout devices are likely to incorporate more advanced features, such as biometric authentication, personalized promotions, and real-time inventory management, further enhancing their appeal and functionality in the global market.

Shopping Mall, Convenience Store, Hypermarket, Others in the Cashless Self-Checkout Devices - Global Market:

Cashless self-checkout devices are increasingly being utilized in various retail settings, including shopping malls, convenience stores, hypermarkets, and other retail environments, each benefiting from the unique advantages these systems offer. In shopping malls, these devices are often deployed in anchor stores and large retail outlets to streamline the checkout process and reduce wait times. By allowing customers to scan and pay for their items independently, cashless self-checkout devices help manage foot traffic, enhance customer satisfaction, and free up staff to focus on other tasks, such as customer service and inventory management. In convenience stores, where speed and efficiency are paramount, cashless self-checkout devices provide a quick and hassle-free way for customers to complete their purchases. These devices are particularly beneficial during peak hours, helping to alleviate congestion and ensure a smooth flow of customers. The compact design of desktop type devices makes them an ideal fit for the limited space available in convenience stores, while still offering the full range of payment options that modern consumers expect. Hypermarkets, with their vast product offerings and high customer volume, benefit significantly from the implementation of cashless self-checkout devices. These systems enable hypermarkets to handle large numbers of transactions efficiently, reducing the need for extensive cashier staffing and minimizing human errors. By offering a self-service option, hypermarkets can cater to tech-savvy consumers who prefer a more autonomous shopping experience, while also providing traditional checkout lanes for those who need assistance. In other retail environments, such as specialty stores and boutique shops, cashless self-checkout devices offer a modern and convenient alternative to traditional checkout methods. These devices can be customized to fit the unique needs of each store, providing a seamless integration with existing systems and enhancing the overall shopping experience. As the global market for cashless self-checkout devices continues to grow, their usage in diverse retail settings is expected to expand, driven by the increasing demand for efficient, customer-centric solutions that align with the evolving expectations of today's consumers.

Cashless Self-Checkout Devices - Global Market Outlook:

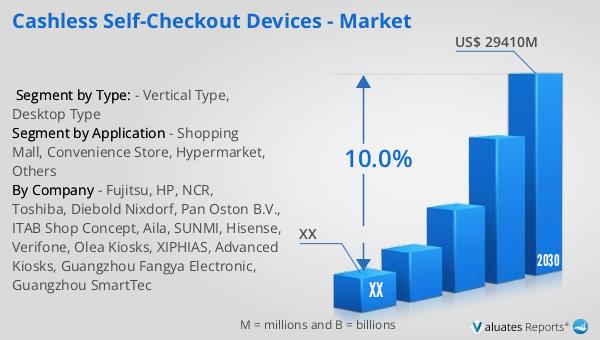

The global market for cashless self-checkout devices was valued at approximately $15.2 billion in 2023 and is projected to reach an adjusted size of $29.41 billion by 2030, reflecting a compound annual growth rate (CAGR) of 10.0% during the forecast period from 2024 to 2030. This growth is largely attributed to the rapid advancement of technology and the widespread adoption of digital payment methods, which have transformed consumer expectations and shopping behaviors. As more consumers seek faster and more convenient shopping experiences, retailers are increasingly turning to cashless self-checkout devices to meet these demands. These devices not only enhance the efficiency of the checkout process but also offer a level of convenience that aligns with the lifestyle of today's tech-savvy consumers. The shift towards cashless transactions is further fueled by the growing popularity of mobile wallets, contactless payments, and other digital payment solutions, which have become integral to the modern shopping experience. As a result, the global market for cashless self-checkout devices is poised for significant growth, driven by the need for innovative solutions that enhance customer satisfaction and streamline retail operations. Retailers who embrace these technologies are likely to gain a competitive edge, as they can offer a more personalized and efficient shopping experience that meets the evolving needs of their customers.

| Report Metric | Details |

| Report Name | Cashless Self-Checkout Devices - Market |

| Forecasted market size in 2030 | US$ 29410 million |

| CAGR | 10.0% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Fujitsu, HP, NCR, Toshiba, Diebold Nixdorf, Pan Oston B.V., ITAB Shop Concept, Aila, SUNMI, Hisense, Verifone, Olea Kiosks, XIPHIAS, Advanced Kiosks, Guangzhou Fangya Electronic, Guangzhou SmartTec |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |