What is Global Rapid Prototyping Medical Devices Market?

The Global Rapid Prototyping Medical Devices Market refers to the industry focused on the development and production of medical devices using rapid prototyping technologies. Rapid prototyping involves creating physical models or prototypes quickly using 3D printing and other advanced manufacturing techniques. This market is crucial for the healthcare sector as it allows for the swift development and testing of medical devices, ensuring they meet the necessary standards and requirements before mass production. The market encompasses a wide range of medical devices, including prosthetics, surgical instruments, dental implants, and orthopedic implants. The ability to rapidly prototype these devices accelerates innovation, reduces time-to-market, and enhances the overall quality and functionality of medical products. This market is driven by the increasing demand for personalized medical solutions, advancements in 3D printing technology, and the growing need for efficient and cost-effective healthcare solutions. As a result, the Global Rapid Prototyping Medical Devices Market plays a pivotal role in advancing medical technology and improving patient care worldwide.

Prosthetics, Surgical Instrument, Dental Implants, Orthopedic Implants, Other in the Global Rapid Prototyping Medical Devices Market:

Prosthetics, surgical instruments, dental implants, orthopedic implants, and other medical devices are integral components of the Global Rapid Prototyping Medical Devices Market. Prosthetics, for instance, benefit immensely from rapid prototyping as it allows for the creation of customized limb replacements tailored to the specific needs of individual patients. This customization ensures a better fit, improved functionality, and enhanced comfort for the user. Surgical instruments, on the other hand, can be rapidly prototyped to test new designs and functionalities, ensuring they meet the stringent requirements of surgical procedures. This process not only speeds up the development of innovative surgical tools but also allows for the testing of ergonomics and usability before mass production. Dental implants are another critical area where rapid prototyping plays a significant role. By using 3D printing technology, dental professionals can create precise and customized implants that fit perfectly into a patient's mouth, improving the success rate of dental procedures and patient satisfaction. Orthopedic implants, such as hip and knee replacements, also benefit from rapid prototyping. The ability to create patient-specific implants ensures a better fit and reduces the risk of complications during surgery. Additionally, rapid prototyping allows for the testing of new materials and designs, leading to the development of more durable and effective orthopedic solutions. Other medical devices, including hearing aids, braces, and diagnostic tools, also leverage rapid prototyping to enhance their design and functionality. The ability to quickly create and test prototypes accelerates the innovation process, allowing for the development of cutting-edge medical devices that improve patient outcomes. Overall, the use of rapid prototyping in the development of prosthetics, surgical instruments, dental implants, orthopedic implants, and other medical devices is revolutionizing the healthcare industry by enabling the creation of highly customized, efficient, and effective solutions.

Hospitals, Clinics, Other in the Global Rapid Prototyping Medical Devices Market:

The usage of Global Rapid Prototyping Medical Devices Market in hospitals, clinics, and other healthcare settings is transforming the way medical devices are developed and utilized. In hospitals, rapid prototyping is used to create customized surgical instruments and implants that cater to the specific needs of patients. This customization ensures that the devices fit perfectly and function optimally, leading to better surgical outcomes and faster recovery times. Additionally, rapid prototyping allows hospitals to quickly develop and test new medical devices, ensuring they meet the necessary standards and requirements before being used in clinical settings. This accelerates the innovation process and allows hospitals to stay at the forefront of medical technology. In clinics, rapid prototyping is used to create personalized medical devices such as dental implants, hearing aids, and braces. The ability to quickly produce customized devices ensures that patients receive the best possible care and treatment. For example, dental clinics can use rapid prototyping to create precise and customized dental implants that fit perfectly into a patient's mouth, improving the success rate of dental procedures and patient satisfaction. Similarly, hearing aids and braces can be tailored to the specific needs of individual patients, ensuring a better fit and improved functionality. Other healthcare settings, such as research laboratories and medical device manufacturing companies, also benefit from rapid prototyping. Research laboratories can use rapid prototyping to develop and test new medical devices, accelerating the innovation process and ensuring that new products are safe and effective. Medical device manufacturing companies can use rapid prototyping to create prototypes of new devices, allowing them to test and refine their designs before mass production. This reduces the risk of costly errors and ensures that the final products meet the highest standards of quality and functionality. Overall, the usage of rapid prototyping in hospitals, clinics, and other healthcare settings is revolutionizing the development and utilization of medical devices, leading to improved patient care and outcomes.

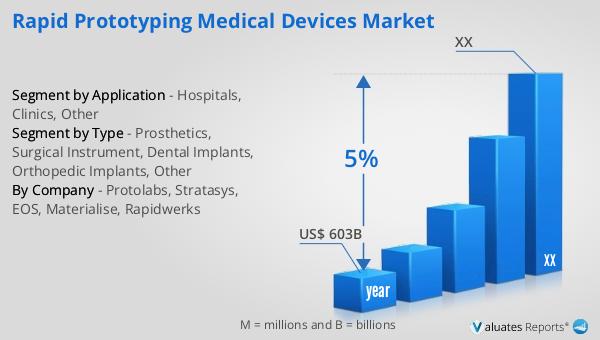

Global Rapid Prototyping Medical Devices Market Outlook:

According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% during the next six years. This significant market size highlights the importance and potential of the medical devices industry in addressing the healthcare needs of the global population. The projected growth rate indicates a steady increase in demand for medical devices, driven by factors such as technological advancements, an aging population, and the rising prevalence of chronic diseases. As the market continues to expand, there will be increased opportunities for innovation and development in the medical devices sector. Companies operating in this market will need to stay at the forefront of technological advancements and continuously improve their products to meet the evolving needs of healthcare providers and patients. The growing market size also underscores the importance of regulatory compliance and quality assurance in the development and production of medical devices. Ensuring that devices meet the necessary standards and requirements is crucial for maintaining patient safety and achieving successful clinical outcomes. Overall, the positive market outlook for the global medical devices industry reflects the critical role that these devices play in improving healthcare delivery and patient care worldwide.

| Report Metric | Details |

| Report Name | Rapid Prototyping Medical Devices Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Protolabs, Stratasys, EOS, Materialise, Rapidwerks |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |