What is Global Microbiome DNA Kit Market?

The Global Microbiome DNA Kit Market refers to the industry focused on the production and distribution of kits designed to extract and analyze DNA from microbiomes. Microbiomes are communities of microorganisms, such as bacteria, fungi, and viruses, that inhabit various environments, including the human body, soil, and water. These kits are essential tools in scientific research, enabling researchers to study the genetic material of these microorganisms to understand their roles in health, disease, and environmental processes. The market for these kits is driven by the growing interest in microbiome research, advancements in DNA sequencing technologies, and the increasing application of microbiome studies in fields such as medicine, agriculture, and environmental science. The kits typically include reagents and protocols for the efficient extraction, purification, and analysis of microbial DNA, ensuring high-quality results for various research purposes. As the understanding of microbiomes continues to expand, the demand for reliable and efficient DNA extraction kits is expected to grow, making this market a crucial component of the broader biotechnology and life sciences sectors.

Purification Kit, Enrichment Kit, Isolation Kit, Others in the Global Microbiome DNA Kit Market:

Purification kits, enrichment kits, isolation kits, and other types of kits play distinct roles in the Global Microbiome DNA Kit Market. Purification kits are designed to remove contaminants and inhibitors from DNA samples, ensuring that the extracted DNA is of high purity and suitable for downstream applications such as sequencing and PCR. These kits typically include reagents and protocols for the lysis of microbial cells, binding of DNA to a purification matrix, washing away impurities, and elution of purified DNA. Enrichment kits, on the other hand, are used to selectively amplify or concentrate specific microbial DNA sequences from a mixed sample. This is particularly useful when studying low-abundance microorganisms or targeting specific genes of interest. Enrichment kits often employ techniques such as PCR amplification, hybridization, or magnetic bead-based separation to achieve selective enrichment. Isolation kits are focused on the initial extraction of DNA from microbial cells. These kits provide the necessary reagents and protocols for efficient cell lysis, DNA binding, and recovery, ensuring that the maximum amount of DNA is extracted from the sample. Isolation kits are crucial for obtaining high-quality DNA from various sample types, including soil, stool, and water. Other types of kits in the market may include specialized kits for specific applications, such as metagenomic sequencing, pathogen detection, or microbiome profiling. These kits are tailored to meet the unique requirements of different research and diagnostic applications, providing researchers with the tools they need to achieve accurate and reliable results. Overall, the diversity of kits available in the Global Microbiome DNA Kit Market reflects the wide range of applications and research needs in the field of microbiome studies. Each type of kit plays a critical role in enabling researchers to extract, purify, and analyze microbial DNA, contributing to the advancement of our understanding of microbiomes and their impact on health and the environment.

Life Sciences Laboratories, Clinical Laboratories, Others in the Global Microbiome DNA Kit Market:

The usage of Global Microbiome DNA Kit Market products spans various areas, including life sciences laboratories, clinical laboratories, and other specialized fields. In life sciences laboratories, these kits are essential for conducting fundamental research on microbiomes. Researchers use these kits to extract and analyze microbial DNA from diverse samples, such as soil, water, and human tissues. This research helps to uncover the roles of microbiomes in different ecosystems, understand microbial interactions, and identify potential applications in agriculture, environmental science, and biotechnology. For instance, studying soil microbiomes can lead to the development of sustainable agricultural practices, while analyzing water microbiomes can help monitor and improve water quality. In clinical laboratories, microbiome DNA kits are used for diagnostic and therapeutic purposes. These kits enable the identification and characterization of microbial communities associated with various diseases, such as gastrointestinal disorders, infections, and metabolic conditions. By analyzing the microbiome composition in patient samples, clinicians can gain insights into disease mechanisms, develop personalized treatment plans, and monitor the effectiveness of therapies. For example, microbiome analysis can help identify bacterial infections, guide antibiotic therapy, and assess the impact of probiotics on gut health. Other specialized fields, such as forensic science and industrial microbiology, also benefit from the use of microbiome DNA kits. In forensic science, these kits can be used to analyze microbial DNA from crime scene samples, providing valuable information for criminal investigations. In industrial microbiology, microbiome DNA kits are used to monitor and optimize microbial processes in various industries, such as food production, pharmaceuticals, and biofuels. By understanding the microbial communities involved in these processes, companies can improve product quality, enhance production efficiency, and develop new biotechnological applications. Overall, the Global Microbiome DNA Kit Market plays a crucial role in advancing research and applications across multiple fields, contributing to the growing understanding of microbiomes and their impact on health, disease, and the environment.

Global Microbiome DNA Kit Market Outlook:

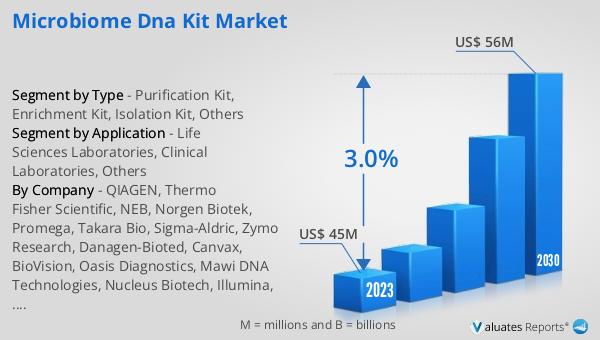

The global Microbiome DNA Kit market was valued at US$ 45 million in 2023 and is anticipated to reach US$ 56 million by 2030, witnessing a CAGR of 3.0% during the forecast period 2024-2030. This market growth reflects the increasing demand for microbiome DNA kits driven by advancements in microbiome research and the expanding applications of these kits in various fields. The steady growth rate indicates a sustained interest in microbiome studies, as researchers and clinicians continue to explore the potential of microbiomes in health, disease, and environmental science. The market's valuation highlights the significant investment in developing and distributing high-quality DNA extraction kits that meet the diverse needs of researchers and practitioners. As the understanding of microbiomes deepens, the demand for reliable and efficient DNA extraction kits is expected to grow, further driving the market's expansion. The projected growth in the market underscores the importance of microbiome research in advancing scientific knowledge and developing innovative solutions for various challenges in medicine, agriculture, and environmental science. Overall, the Global Microbiome DNA Kit Market is poised for steady growth, reflecting the ongoing advancements and increasing applications of microbiome research.

| Report Metric | Details |

| Report Name | Microbiome DNA Kit Market |

| Accounted market size in 2023 | US$ 45 million |

| Forecasted market size in 2030 | US$ 56 million |

| CAGR | 3.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | QIAGEN, Thermo Fisher Scientific, NEB, Norgen Biotek, Promega, Takara Bio, Sigma-Aldric, Zymo Research, Danagen-Bioted, Canvax, BioVision, Oasis Diagnostics, Mawi DNA Technologies, Nucleus Biotech, Illumina, Omega Bio-tek, MP Biomedicals, Analytik Jena, MagBio Genomics, Genesee Scientific |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |