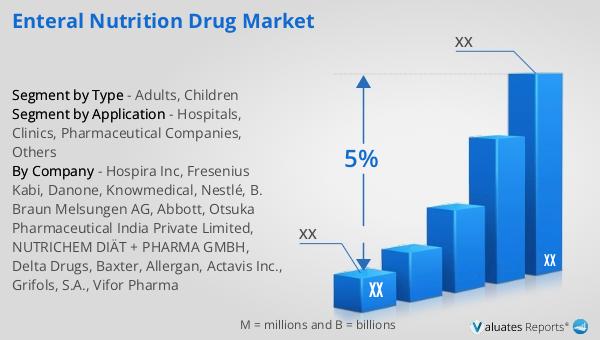

What is Global Enteral Nutrition Drug Market?

The Global Enteral Nutrition Drug Market is a specialized segment of the healthcare industry that focuses on providing nutritional support to individuals who cannot consume food orally. This market encompasses a range of products designed to deliver nutrients directly into the gastrointestinal tract through tubes. Enteral nutrition is crucial for patients with conditions that impair their ability to eat, such as neurological disorders, gastrointestinal diseases, or severe illnesses that require intensive care. The market includes various formulations, such as standard, disease-specific, and peptide-based formulas, catering to different patient needs. These products are developed to ensure that patients receive essential nutrients, vitamins, and minerals to maintain their health and support recovery. The market is driven by factors such as the increasing prevalence of chronic diseases, an aging population, and advancements in medical technology that enhance the efficacy and safety of enteral nutrition products. Additionally, the growing awareness of the benefits of enteral nutrition in improving patient outcomes and reducing healthcare costs contributes to the market's expansion. As healthcare systems worldwide continue to evolve, the Global Enteral Nutrition Drug Market plays a vital role in supporting patient care and improving quality of life for those who rely on nutritional support.

Adults, Children in the Global Enteral Nutrition Drug Market:

In the Global Enteral Nutrition Drug Market, the needs of adults and children differ significantly, necessitating tailored approaches to nutritional support. For adults, enteral nutrition is often used to manage chronic conditions such as cancer, stroke, and gastrointestinal disorders. These patients may require long-term nutritional support to maintain their health and manage symptoms. Adult enteral nutrition products are formulated to provide balanced nutrition, with options for high-protein, low-carbohydrate, or fiber-enriched formulas depending on the patient's specific needs. The goal is to ensure that adults receive adequate nutrition to support their recovery and overall well-being. In contrast, enteral nutrition for children focuses on supporting growth and development. Pediatric patients may require enteral nutrition due to congenital disorders, metabolic diseases, or severe malnutrition. Children's nutritional needs are different from adults, as they require specific nutrients to support their rapid growth and development. Pediatric enteral nutrition products are designed to provide essential nutrients in appropriate proportions to support healthy growth. These products often come in flavors that are more palatable for children, making it easier for caregivers to administer them. The market for pediatric enteral nutrition is driven by the increasing prevalence of childhood diseases and the growing awareness of the importance of early nutritional intervention. Both adult and pediatric enteral nutrition markets face challenges, such as ensuring product safety, managing costs, and addressing patient compliance. However, advancements in formulation technology and increased research into the specific nutritional needs of different patient populations are helping to overcome these challenges. The Global Enteral Nutrition Drug Market continues to evolve, with a focus on developing innovative products that meet the diverse needs of adults and children. As healthcare providers and caregivers become more aware of the benefits of enteral nutrition, the market is expected to grow, providing essential support to patients of all ages.

Hospitals, Clinics, Pharmaceutical Companies, Others in the Global Enteral Nutrition Drug Market:

The usage of Global Enteral Nutrition Drug Market products spans various healthcare settings, including hospitals, clinics, pharmaceutical companies, and other facilities. In hospitals, enteral nutrition is a critical component of patient care, particularly in intensive care units (ICUs) where patients may be unable to consume food orally due to severe illness or surgery. Hospital staff, including dietitians and nurses, work together to develop individualized nutrition plans that meet the specific needs of each patient. Enteral nutrition helps improve patient outcomes by providing essential nutrients that support recovery and reduce the risk of complications. In clinics, enteral nutrition is often used for patients with chronic conditions who require ongoing nutritional support. Clinics provide a more personalized approach to patient care, allowing healthcare providers to closely monitor patients' nutritional status and adjust their enteral nutrition plans as needed. This setting is particularly beneficial for patients who require long-term nutritional support, as it allows for regular follow-up and adjustments to their care plans. Pharmaceutical companies play a crucial role in the Global Enteral Nutrition Drug Market by developing and manufacturing enteral nutrition products. These companies invest in research and development to create innovative formulations that meet the diverse needs of patients. They also work to ensure that their products are safe, effective, and compliant with regulatory standards. Pharmaceutical companies collaborate with healthcare providers to educate them about the benefits of enteral nutrition and provide training on the proper administration of these products. Other facilities, such as long-term care centers and home healthcare services, also utilize enteral nutrition products to support patients who require nutritional support outside of traditional healthcare settings. These facilities provide a more comfortable environment for patients, allowing them to receive the care they need while maintaining their independence. Home healthcare services, in particular, offer a convenient option for patients who prefer to receive enteral nutrition in the comfort of their own homes. Overall, the Global Enteral Nutrition Drug Market plays a vital role in supporting patient care across various healthcare settings. By providing essential nutritional support, enteral nutrition products help improve patient outcomes, reduce healthcare costs, and enhance the quality of life for patients who rely on these products.

Global Enteral Nutrition Drug Market Outlook:

The outlook for the Global Enteral Nutrition Drug Market is closely tied to the broader pharmaceutical and chemical drug markets. In 2022, the global pharmaceutical market was valued at approximately 1,475 billion USD, with an expected compound annual growth rate (CAGR) of 5% over the next six years. This growth is indicative of the increasing demand for pharmaceutical products, including enteral nutrition drugs, as healthcare systems worldwide continue to evolve and expand. In comparison, the chemical drug market has shown a steady increase, growing from 1,005 billion USD in 2018 to an estimated 1,094 billion USD in 2022. This growth reflects the ongoing advancements in drug development and the increasing need for specialized medications to address a wide range of health conditions. The Global Enteral Nutrition Drug Market is expected to benefit from these trends, as the demand for nutritional support products continues to rise. As healthcare providers and patients become more aware of the benefits of enteral nutrition, the market is likely to see increased adoption of these products across various healthcare settings. The focus on improving patient outcomes and reducing healthcare costs will further drive the growth of the Global Enteral Nutrition Drug Market, making it an essential component of the broader pharmaceutical industry.

| Report Metric | Details |

| Report Name | Enteral Nutrition Drug Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Hospira Inc, Fresenius Kabi, Danone, Knowmedical, Nestlé, B. Braun Melsungen AG, Abbott, Otsuka Pharmaceutical India Private Limited, NUTRICHEM DIÄT + PHARMA GMBH, Delta Drugs, Baxter, Allergan, Actavis Inc., Grifols, S.A., Vifor Pharma |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |