What is Global Medical Sterile Surgical Films Market?

The Global Medical Sterile Surgical Films Market refers to the industry that produces and distributes films used in medical settings to maintain sterility during surgical procedures. These films are crucial in preventing infections and ensuring a sterile environment in operating rooms. They are typically used to cover surgical instruments, equipment, and even patients' skin to create a barrier against bacteria and other contaminants. The market for these films is driven by the increasing number of surgeries worldwide, advancements in medical technology, and a growing awareness of the importance of infection control in healthcare settings. As healthcare systems strive to improve patient outcomes and reduce hospital-acquired infections, the demand for high-quality sterile surgical films continues to rise. These films are made from various materials, each offering unique properties such as breathability, flexibility, and strength, to meet the diverse needs of surgical procedures. The market is also influenced by regulatory standards and guidelines that ensure the safety and efficacy of these products. Overall, the Global Medical Sterile Surgical Films Market plays a vital role in modern healthcare by supporting safe and effective surgical practices.

PU Film, PE Film, Iodophor Film in the Global Medical Sterile Surgical Films Market:

Polyurethane (PU) film, polyethylene (PE) film, and iodophor film are three significant types of materials used in the Global Medical Sterile Surgical Films Market, each offering distinct advantages for surgical applications. PU film is known for its excellent breathability and flexibility, making it ideal for use in wound dressings and surgical drapes. Its ability to allow moisture vapor transmission while maintaining a barrier against liquids and bacteria makes it a preferred choice in surgeries where maintaining a sterile environment is critical. PU films are also highly conformable, which means they can easily adapt to the contours of the body, providing a secure fit that minimizes the risk of contamination. On the other hand, PE film is valued for its strength and durability. It is often used in the production of surgical drapes and covers that require a robust barrier against fluids and pathogens. PE films are typically less expensive than PU films, making them a cost-effective option for healthcare facilities. They are also resistant to tearing and puncturing, which ensures that they maintain their integrity during surgical procedures. Iodophor film is another important material in this market, known for its antimicrobial properties. It is impregnated with iodine, which provides an additional layer of protection against infection by actively killing bacteria on contact. This makes iodophor films particularly useful in surgeries where there is a high risk of infection or in settings where sterility is paramount. The use of iodophor films can help reduce the incidence of surgical site infections, which are a significant concern in healthcare. Each of these films plays a crucial role in the Global Medical Sterile Surgical Films Market, offering unique benefits that cater to the specific needs of different surgical procedures. As the demand for safer and more effective surgical solutions continues to grow, the development and innovation of these films remain a key focus for manufacturers and healthcare providers alike.

Hospital, Ambulatory Surgical Centers, Other in the Global Medical Sterile Surgical Films Market:

The usage of Global Medical Sterile Surgical Films Market products extends across various healthcare settings, including hospitals, ambulatory surgical centers, and other medical facilities. In hospitals, these films are an integral part of infection control protocols. They are used extensively in operating rooms to cover surgical instruments, equipment, and even the patient's skin to create a sterile field. This is crucial in preventing surgical site infections, which can lead to prolonged hospital stays and increased healthcare costs. The films' ability to provide a reliable barrier against bacteria and other contaminants makes them indispensable in maintaining a sterile environment during surgeries. In ambulatory surgical centers, where outpatient surgeries are performed, the need for sterile surgical films is equally important. These centers often handle a high volume of procedures, and the use of sterile films helps ensure that each surgery is conducted in a safe and controlled environment. The films' ease of use and effectiveness in preventing contamination make them a valuable tool in these settings, where quick turnover and efficiency are essential. Other medical facilities, such as clinics and specialized surgical centers, also rely on sterile surgical films to maintain high standards of infection control. These films are used in various procedures, from minor surgeries to complex interventions, providing a consistent level of protection against infection. The versatility of these films allows them to be used in a wide range of applications, making them a critical component of modern surgical practices. Overall, the Global Medical Sterile Surgical Films Market plays a vital role in supporting safe and effective surgical procedures across different healthcare settings, contributing to improved patient outcomes and reduced healthcare-associated infections.

Global Medical Sterile Surgical Films Market Outlook:

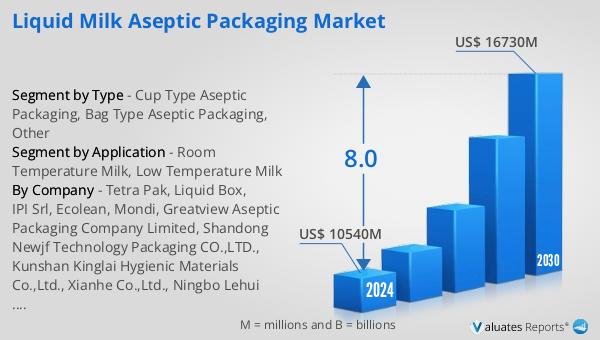

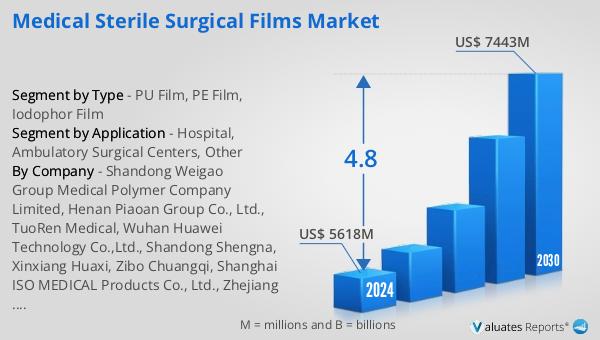

The outlook for the Global Medical Sterile Surgical Films Market indicates a promising growth trajectory over the coming years. The market is expected to expand from a valuation of US$ 5618 million in 2024 to US$ 7443 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 4.8% during this period. This growth is driven by several factors, including the increasing demand for surgical procedures worldwide, advancements in medical technology, and a heightened focus on infection control in healthcare settings. As healthcare systems continue to prioritize patient safety and the reduction of hospital-acquired infections, the demand for high-quality sterile surgical films is anticipated to rise. Additionally, the broader medical devices market, estimated at US$ 603 billion in 2023, is projected to grow at a CAGR of 5% over the next six years. This growth in the medical devices sector is likely to have a positive impact on the sterile surgical films market, as these films are an essential component of many medical devices and surgical procedures. The increasing awareness of the importance of maintaining a sterile environment in healthcare settings is expected to further drive the demand for these films, supporting their continued growth and development in the global market.

| Report Metric | Details |

| Report Name | Medical Sterile Surgical Films Market |

| Accounted market size in 2024 | US$ 5618 in million |

| Forecasted market size in 2030 | US$ 7443 million |

| CAGR | 4.8 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Shandong Weigao Group Medical Polymer Company Limited, Henan Piaoan Group Co., Ltd., TuoRen Medical, Wuhan Huawei Technology Co.,Ltd., Shandong Shengna, Xinxiang Huaxi, Zibo Chuangqi, Shanghai ISO MEDICAL Products Co., Ltd., Zhejiang Kang Li Di Medical Articles CO.,LTD, Henan Ruike Medical Equipment Co., Ltd., Shijiazhuang Zhonghui Pharmaceutical Packaging Co., Ltd., TekniPlex, Foster Corporation, SÜDPACK Medica |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |