What is Global Fibre to X Market?

The Global Fibre to X Market, often abbreviated as FTTx, represents a significant advancement in telecommunications infrastructure, focusing on delivering high-speed internet connectivity through optical fiber cables. This market encompasses various deployment methods, each designed to bring fiber optic connections closer to the end user, thereby enhancing internet speed and reliability. The term "Fibre to X" is a generic representation where "X" can denote different endpoints such as homes, buildings, nodes, or desks. The primary goal of FTTx is to replace traditional copper lines with fiber optics, which offer superior bandwidth and lower latency. This transition is crucial in meeting the growing demand for high-speed internet driven by the proliferation of digital services, streaming platforms, and cloud-based applications. As more devices become interconnected and data consumption increases, the need for robust and scalable internet infrastructure becomes imperative. The Global Fibre to X Market is thus a pivotal component in the digital transformation journey, enabling seamless connectivity and supporting the burgeoning digital economy. With continuous technological advancements and increasing investments in fiber optic networks, the FTTx market is poised for substantial growth, catering to diverse sectors and enhancing the overall internet experience for users worldwide.

Fiber to Buildings (FTTB), Fiber to Desks (FTTD), Fiber to Nodes (FTTN), Others in the Global Fibre to X Market:

Fiber to the Building (FTTB) is a specific type of FTTx deployment where fiber optic cables are installed up to the building's premises. This setup is particularly beneficial for multi-dwelling units like apartment complexes or office buildings, where the fiber connection is terminated at a central point within the building. From there, the connection is distributed to individual units using existing copper or coaxial cables. FTTB offers significant improvements in internet speed and reliability compared to traditional broadband connections, making it an attractive option for property developers and building managers aiming to provide high-quality internet services to tenants. Fiber to the Desk (FTTD) takes the concept a step further by extending the fiber optic connection directly to individual workstations or desks within a building. This approach is ideal for businesses that require ultra-fast and reliable internet connectivity for operations such as video conferencing, data-intensive applications, and cloud computing. By delivering fiber directly to the desk, organizations can ensure that their employees have access to the best possible internet performance, enhancing productivity and enabling seamless digital workflows. Fiber to the Node (FTTN) involves running fiber optic cables to a central node or cabinet located in a neighborhood or community. From this node, the connection is distributed to individual homes or businesses using existing copper lines. While FTTN does not offer the same level of performance as FTTB or FTTD, it is a cost-effective solution for providing high-speed internet to areas where full fiber deployment may not be feasible. FTTN is often used as an interim solution, allowing service providers to upgrade their networks incrementally while still delivering improved internet services to customers. Other variations of FTTx include Fiber to the Home (FTTH), where fiber is extended directly to individual residences, and Fiber to the Curb (FTTC), where fiber is terminated at a street cabinet near the customer's premises. Each of these deployment methods has its own advantages and challenges, and the choice of which to implement depends on factors such as cost, existing infrastructure, and the specific needs of the community or organization. Overall, the Global Fibre to X Market is characterized by a diverse range of deployment strategies, each designed to bring the benefits of fiber optic technology closer to end users and support the growing demand for high-speed internet connectivity.

Industrial, Commercial, Residential in the Global Fibre to X Market:

The usage of the Global Fibre to X Market spans across various sectors, including industrial, commercial, and residential areas, each benefiting from the enhanced connectivity and performance that fiber optic technology provides. In industrial settings, the adoption of FTTx solutions is driven by the need for reliable and high-speed internet connections to support advanced manufacturing processes, automation, and the Internet of Things (IoT). Industries such as automotive, aerospace, and electronics rely on real-time data exchange and seamless communication between machines and systems to optimize production efficiency and reduce downtime. By implementing FTTx, these industries can achieve faster data transfer rates, lower latency, and improved network reliability, enabling them to harness the full potential of digital technologies and maintain a competitive edge in the global market. In the commercial sector, businesses of all sizes are increasingly turning to FTTx solutions to meet their growing connectivity needs. With the rise of remote work, cloud computing, and digital collaboration tools, companies require robust internet infrastructure to ensure smooth operations and maintain productivity. FTTx provides businesses with the bandwidth and reliability needed to support data-intensive applications, video conferencing, and secure data transfer, allowing them to operate efficiently and effectively in a digital-first world. Moreover, FTTx can enhance customer experiences by enabling faster and more reliable online services, such as e-commerce platforms, streaming services, and digital customer support. In residential areas, the demand for high-speed internet has never been greater, driven by the increasing popularity of streaming services, online gaming, and smart home technologies. FTTx solutions, particularly Fiber to the Home (FTTH), offer residents unparalleled internet speeds and reliability, transforming the way people access and consume digital content. With fiber optic connections, households can enjoy seamless streaming of high-definition videos, lag-free online gaming, and uninterrupted video calls, all while supporting multiple devices simultaneously. Additionally, FTTx can facilitate the adoption of smart home devices, which rely on stable and fast internet connections to function effectively. As more households embrace digital lifestyles, the demand for FTTx solutions is expected to continue growing, making it a crucial component of modern residential infrastructure. Overall, the Global Fibre to X Market plays a vital role in supporting the digital transformation of industrial, commercial, and residential sectors, providing the connectivity needed to drive innovation, enhance productivity, and improve quality of life.

Global Fibre to X Market Outlook:

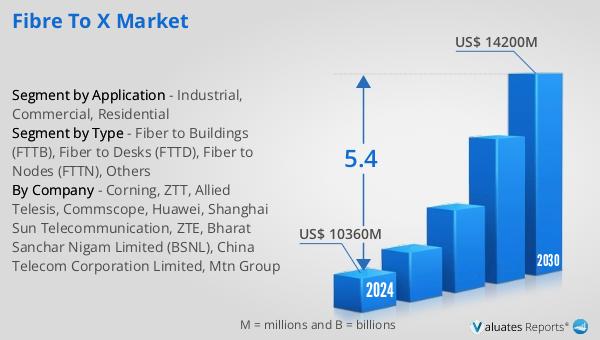

The global Fibre to X market is anticipated to experience significant growth over the coming years. Starting from an estimated value of $10,360 million in 2024, it is projected to reach approximately $14,200 million by 2030. This growth trajectory represents a Compound Annual Growth Rate (CAGR) of 5.4% throughout the forecast period. This expansion is driven by the increasing demand for high-speed internet connectivity across various sectors, including industrial, commercial, and residential areas. As digital transformation continues to accelerate, the need for robust and reliable internet infrastructure becomes more critical, fueling the adoption of FTTx solutions. The market's growth is also supported by ongoing technological advancements in fiber optic technology, which offer improved performance and cost-effectiveness compared to traditional copper-based networks. Additionally, government initiatives and investments in broadband infrastructure development further contribute to the market's expansion, as countries strive to enhance their digital capabilities and bridge the digital divide. As a result, the Global Fibre to X Market is poised to play a pivotal role in shaping the future of internet connectivity, enabling seamless communication and supporting the growing digital economy.

| Report Metric | Details |

| Report Name | Fibre to X Market |

| Accounted market size in 2024 | US$ 10360 million |

| Forecasted market size in 2030 | US$ 14200 million |

| CAGR | 5.4 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Corning, ZTT, Allied Telesis, Commscope, Huawei, Shanghai Sun Telecommunication, ZTE, Bharat Sanchar Nigam Limited (BSNL), China Telecom Corporation Limited, Mtn Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |