What is Global Audio Streaming Players Market?

The Global Audio Streaming Players Market refers to the industry focused on devices and platforms that enable the streaming of audio content over the internet. These players are designed to provide users with access to a vast array of audio content, including music, podcasts, audiobooks, and more, without the need for physical media. The market encompasses a wide range of products, from dedicated audio streaming devices to multifunctional gadgets like smartphones and smart speakers. The growth of this market is driven by the increasing demand for on-demand audio content, advancements in internet connectivity, and the proliferation of smart devices. Consumers are increasingly seeking seamless and high-quality audio experiences, which has led to innovations in streaming technology and the development of user-friendly interfaces. Additionally, the rise of subscription-based streaming services has further fueled the market, offering users access to extensive libraries of audio content for a monthly fee. As a result, the Global Audio Streaming Players Market is characterized by rapid technological advancements and a competitive landscape, with numerous companies vying for market share by offering unique features and superior sound quality.

6 Channels, 8 Channels, 16 Channels, 24 Channels, 32 Channels, Others in the Global Audio Streaming Players Market:

In the Global Audio Streaming Players Market, the number of channels refers to the audio output capabilities of the devices, which can significantly impact the listening experience. Starting with 6-channel audio streaming players, these devices are typically designed for basic surround sound setups, providing a more immersive audio experience than traditional stereo systems. They are often used in home theater systems where space and budget constraints exist, offering a balanced sound distribution that enhances the overall audio quality. Moving up to 8-channel audio streaming players, these devices offer a more advanced surround sound experience, often used in more sophisticated home theater setups. They provide additional channels for more precise sound localization, which can be particularly beneficial for movie enthusiasts who seek a more cinematic experience at home. The 16-channel audio streaming players are generally used in professional settings, such as recording studios or live sound environments, where detailed sound mixing and distribution are crucial. These players allow for intricate audio configurations, enabling sound engineers to create complex soundscapes with precision. The 24-channel audio streaming players take this a step further, offering even more flexibility and control over audio output. They are often used in large venues or professional audio installations where high-quality sound reproduction is essential. The 32-channel audio streaming players represent the pinnacle of audio streaming technology, providing unparalleled sound quality and control. These devices are typically used in large-scale professional audio environments, such as concert halls or broadcast studios, where the highest level of audio fidelity is required. Finally, the "Others" category in the Global Audio Streaming Players Market includes devices with unique or customizable channel configurations, catering to niche markets or specific audio needs. These players might offer specialized features or support for unconventional audio setups, providing solutions for users with specific requirements. Overall, the variety of channel configurations available in the Global Audio Streaming Players Market reflects the diverse needs of consumers and professionals alike, with each option offering distinct advantages depending on the intended use and environment.

Home Use, Commercial Use, Others in the Global Audio Streaming Players Market:

The Global Audio Streaming Players Market finds its usage across various areas, including home use, commercial use, and other specialized applications. In the realm of home use, audio streaming players have become an integral part of modern households, offering users the convenience of accessing a vast library of audio content at their fingertips. These devices are often integrated into smart home ecosystems, allowing users to control their audio experience through voice commands or mobile apps. The ability to stream high-quality audio content from various online platforms has transformed the way people consume music, podcasts, and other audio media at home. In commercial settings, audio streaming players are utilized to enhance customer experiences and create engaging environments. Retail stores, restaurants, and hospitality venues often use these devices to stream background music or curated playlists that align with their brand identity. This not only improves the ambiance but also helps in attracting and retaining customers. Additionally, businesses can use audio streaming players for in-store announcements or promotional messages, providing a versatile tool for communication. Beyond home and commercial use, the Global Audio Streaming Players Market also caters to other specialized applications. For instance, educational institutions may use these devices to stream audio content for language learning or other educational purposes. Similarly, fitness centers might employ audio streaming players to provide motivational music or guided workout sessions to their clients. The versatility of audio streaming players makes them suitable for a wide range of applications, each benefiting from the ability to deliver high-quality audio content seamlessly. As technology continues to evolve, the usage of audio streaming players is expected to expand further, offering new possibilities for both consumers and businesses.

Global Audio Streaming Players Market Outlook:

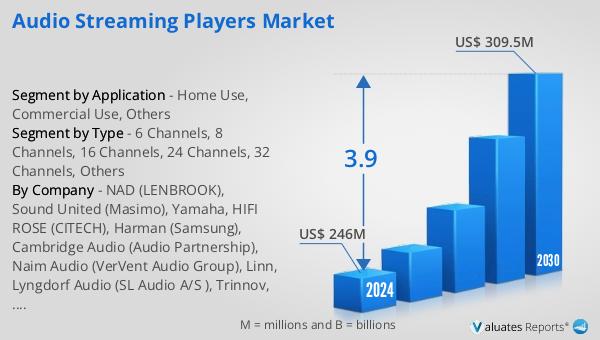

The outlook for the Global Audio Streaming Players Market indicates a steady growth trajectory over the coming years. The market is anticipated to expand from a valuation of $246 million in 2024 to approximately $309.5 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 3.9% during this period. This growth is driven by several factors, including the increasing demand for on-demand audio content and the proliferation of smart devices that facilitate seamless audio streaming. The market's expansion is also supported by the rising popularity of subscription-based streaming services, which offer users access to extensive libraries of audio content for a monthly fee. Additionally, advancements in internet connectivity and streaming technology have made it easier for consumers to access high-quality audio content from anywhere, further fueling market growth. In 2022, China emerged as the largest online retail market, with online retail sales reaching 13.79 trillion yuan, marking a year-on-year increase of 4%. This highlights the growing importance of digital platforms and the potential for further growth in the audio streaming sector. As the market continues to evolve, companies are likely to focus on developing innovative features and enhancing sound quality to capture a larger share of this expanding market.

| Report Metric | Details |

| Report Name | Audio Streaming Players Market |

| Accounted market size in 2024 | US$ 246 million |

| Forecasted market size in 2030 | US$ 309.5 million |

| CAGR | 3.9 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | NAD (LENBROOK), Sound United (Masimo), Yamaha, HIFI ROSE (CITECH), Harman (Samsung), Cambridge Audio (Audio Partnership), Naim Audio (VerVent Audio Group), Linn, Lyngdorf Audio (SL Audio A/S ), Trinnov, Krell Industries, Pioneer Corporation, Roksan (Monitor Audio), AudioControl (AAMP Global), McIntosh, Rotel, Crestron, Meridian, Parasound Products, Hegel Music Systems, AVM Audio Video, MOON (Simaudio), Primare, Audiolab (International Audio Group), Anthem, Bryston |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |