What is High-Performance Long-Acting Fungicide - Global Market?

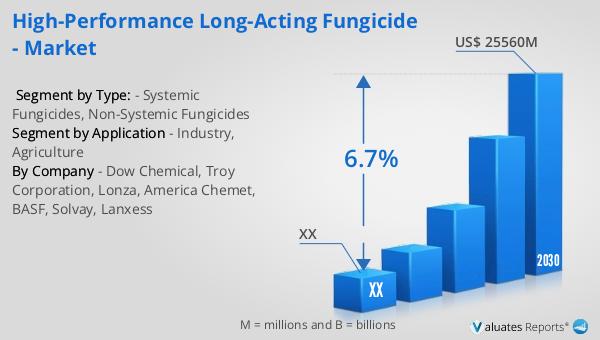

High-performance long-acting fungicides are specialized chemical agents designed to combat fungal infections by inhibiting, killing, and preventing the growth and reproduction of fungi and other microorganisms. These fungicides are formulated to provide extended protection, reducing the need for frequent applications and thereby offering cost-effective and efficient solutions for managing fungal diseases. The global market for these fungicides was valued at approximately US$ 16,310 million in 2023. It is projected to grow significantly, reaching an estimated size of US$ 25,560 million by 2030, with a compound annual growth rate (CAGR) of 6.7% during the forecast period from 2024 to 2030. This growth is driven by increasing demand across various sectors, including agriculture and industry, where the need for effective and long-lasting fungal control is paramount. The fungicides are particularly valued for their ability to provide robust protection against a wide range of pathogens, ensuring the health and productivity of crops and materials. As the global population continues to grow and the demand for food and resources increases, the role of high-performance long-acting fungicides in safeguarding agricultural yields and industrial products becomes increasingly critical.

Systemic Fungicides, Non-Systemic Fungicides in the High-Performance Long-Acting Fungicide - Global Market:

Systemic fungicides and non-systemic fungicides are two primary categories within the high-performance long-acting fungicide market, each offering distinct mechanisms of action and benefits. Systemic fungicides are absorbed by the plant and translocated throughout its tissues, providing internal protection against fungal pathogens. This type of fungicide is particularly effective because it can reach and protect new growth, offering comprehensive coverage and long-lasting effects. Systemic fungicides are often used in agriculture to protect crops from diseases that affect the entire plant, such as rusts, mildews, and blights. They are valued for their ability to provide consistent protection, even in adverse weather conditions, and for their reduced environmental impact compared to non-systemic options. On the other hand, non-systemic fungicides, also known as contact fungicides, remain on the surface of the plant and act as a protective barrier against fungal spores. These fungicides are typically used as a preventive measure, applied before the onset of disease to prevent infection. Non-systemic fungicides are often favored for their immediate action and effectiveness in controlling surface-level infections. However, they require more frequent applications to maintain their protective barrier, especially after rain or irrigation. In the global market, both systemic and non-systemic fungicides play crucial roles, with their usage often determined by the specific needs of the crop, environmental conditions, and the type of fungal threat present. The choice between systemic and non-systemic fungicides is influenced by factors such as the severity of the disease, the stage of crop growth, and the potential for resistance development. As the demand for high-performance long-acting fungicides continues to grow, advancements in formulation and delivery methods are enhancing the efficacy and sustainability of both systemic and non-systemic options. Innovations such as nano-formulations and bio-based fungicides are emerging, offering new possibilities for effective and environmentally friendly fungal control. These advancements are expected to further drive the growth of the global fungicide market, as they address the increasing need for sustainable agricultural practices and improved crop protection.

Industry, Agriculture in the High-Performance Long-Acting Fungicide - Global Market:

High-performance long-acting fungicides are extensively used in both industry and agriculture, providing essential protection against fungal infections that can compromise productivity and quality. In the agricultural sector, these fungicides are crucial for safeguarding crops from a wide range of fungal diseases that can significantly reduce yields and affect food security. Farmers rely on these fungicides to protect staple crops such as wheat, rice, and corn, as well as high-value crops like fruits and vegetables. The long-acting nature of these fungicides reduces the need for frequent applications, saving time and resources while ensuring continuous protection throughout the growing season. This is particularly important in regions with high humidity and rainfall, where fungal diseases are more prevalent. In addition to crop protection, high-performance fungicides are also used in seed treatment, ensuring healthy germination and early growth. In the industrial sector, these fungicides are used to protect materials and products from fungal degradation. Industries such as textiles, paper, and leather rely on fungicides to prevent mold and mildew, which can cause discoloration, odor, and structural damage. In construction, fungicides are used to protect building materials like wood and drywall from fungal decay, extending the lifespan of structures and reducing maintenance costs. The use of high-performance long-acting fungicides in these industries is driven by the need to maintain product quality and durability, as well as to comply with health and safety regulations. As industries continue to innovate and develop new materials, the demand for effective fungal protection solutions is expected to grow. The versatility and efficacy of high-performance long-acting fungicides make them indispensable tools in both agriculture and industry, supporting productivity and sustainability across various sectors.

High-Performance Long-Acting Fungicide - Global Market Outlook:

The global market for high-performance long-acting fungicides was valued at approximately US$ 16,310 million in 2023, with projections indicating a significant increase to US$ 25,560 million by 2030. This growth, at a compound annual growth rate (CAGR) of 6.7% from 2024 to 2030, underscores the increasing demand for effective and long-lasting solutions to combat fungal infections. High-performance long-acting fungicides are chemical agents with potent bactericidal properties, designed to inhibit, kill, and prevent the growth and reproduction of various bacteria, viruses, fungi, and other microorganisms. These fungicides are essential in both agricultural and industrial applications, where they provide critical protection against fungal threats that can compromise productivity and quality. The market's expansion is driven by the growing need for sustainable and efficient fungal control solutions, as well as advancements in fungicide formulations and delivery methods. As the global population continues to rise and the demand for food and resources increases, the role of high-performance long-acting fungicides in ensuring agricultural yields and protecting industrial products becomes increasingly vital. The market outlook reflects the importance of these fungicides in supporting global food security and industrial sustainability, highlighting their value as indispensable tools in the fight against fungal diseases.

| Report Metric | Details |

| Report Name | High-Performance Long-Acting Fungicide - Market |

| Forecasted market size in 2030 | US$ 25560 million |

| CAGR | 6.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Dow Chemical, Troy Corporation, Lonza, America Chemet, BASF, Solvay, Lanxess |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |