What is Global Airborne Synthetic Aperture Radar Market?

The Global Airborne Synthetic Aperture Radar (SAR) Market is a specialized segment within the broader radar technology industry, focusing on advanced radar systems mounted on aircraft. These systems are designed to capture high-resolution images of the Earth's surface, regardless of weather conditions or time of day. Unlike traditional radar systems, SAR uses the motion of the aircraft to simulate a larger antenna, thereby achieving finer resolution images. This technology is crucial for various applications, including military reconnaissance, environmental monitoring, and natural resource exploration. The market for airborne SAR is driven by the increasing demand for precise and reliable imaging solutions in challenging environments. As governments and organizations worldwide seek to enhance their surveillance and monitoring capabilities, the adoption of airborne SAR systems is expected to grow. The market is characterized by continuous technological advancements, with manufacturers focusing on developing more efficient and versatile systems. These innovations aim to improve image quality, reduce system weight, and enhance operational flexibility. Overall, the Global Airborne Synthetic Aperture Radar Market represents a dynamic and evolving field, offering significant opportunities for growth and development in the coming years.

Single Mode, Multi-Mode in the Global Airborne Synthetic Aperture Radar Market:

In the Global Airborne Synthetic Aperture Radar Market, systems are primarily categorized into Single Mode and Multi-Mode configurations, each serving distinct operational needs. Single Mode SAR systems are designed to operate in a specific mode, such as stripmap, spotlight, or scan mode, each offering unique advantages. Stripmap mode provides continuous coverage along a flight path, making it ideal for wide-area surveillance. Spotlight mode, on the other hand, focuses on a smaller area, allowing for higher resolution imaging, which is beneficial for detailed analysis of specific targets. Scan mode offers a balance between coverage and resolution, suitable for general reconnaissance missions. These Single Mode systems are typically simpler and more cost-effective, making them a popular choice for applications with well-defined requirements. Multi-Mode SAR systems, however, offer greater versatility by integrating multiple operational modes within a single system. This flexibility allows users to switch between modes based on mission objectives, environmental conditions, or specific imaging needs. For instance, a Multi-Mode SAR can start with a wide-area scan to identify areas of interest and then switch to spotlight mode for detailed examination. This adaptability is particularly valuable in dynamic operational environments, such as military missions or disaster response scenarios, where situational requirements can change rapidly. The development of Multi-Mode SAR systems involves sophisticated engineering to ensure seamless mode transitions and optimal performance across different configurations. Manufacturers invest heavily in research and development to enhance the capabilities of these systems, focusing on improving resolution, range, and processing speed. The integration of advanced technologies, such as digital beamforming and real-time data processing, further enhances the functionality of Multi-Mode SAR systems. These advancements enable more precise and timely decision-making, which is critical in high-stakes operations. Additionally, the ability to operate in multiple modes reduces the need for multiple specialized systems, offering cost savings and logistical advantages. As a result, Multi-Mode SAR systems are increasingly favored in applications requiring high flexibility and adaptability. Despite their higher initial cost, the long-term benefits of Multi-Mode systems, including enhanced operational efficiency and reduced mission complexity, make them an attractive investment for organizations with diverse imaging needs. In summary, the choice between Single Mode and Multi-Mode SAR systems in the Global Airborne Synthetic Aperture Radar Market depends on specific operational requirements, budget constraints, and the desired level of flexibility. Both configurations have their unique strengths and are essential components of modern airborne radar technology, contributing to the market's growth and evolution.

Defense, Environmental Monitoring, Natural Resource Exploration, Others in the Global Airborne Synthetic Aperture Radar Market:

The Global Airborne Synthetic Aperture Radar Market finds extensive applications across various sectors, including Defense, Environmental Monitoring, Natural Resource Exploration, and others. In the Defense sector, airborne SAR systems are invaluable for intelligence, surveillance, and reconnaissance (ISR) missions. They provide high-resolution imagery that is crucial for identifying and tracking potential threats, assessing battlefield conditions, and planning military operations. The ability to operate in all weather conditions and through cloud cover gives military forces a significant strategic advantage. Environmental Monitoring is another critical area where airborne SAR technology is utilized. These systems are used to monitor changes in land use, track deforestation, and assess the impact of natural disasters such as floods and earthquakes. The high-resolution images produced by SAR systems enable detailed analysis of environmental changes, supporting efforts in conservation and sustainable development. In Natural Resource Exploration, airborne SAR systems play a vital role in mapping geological features, identifying mineral deposits, and monitoring oil and gas pipelines. The ability to penetrate vegetation and soil makes SAR an effective tool for exploring remote and inaccessible areas. This capability is particularly valuable in the mining and energy sectors, where accurate and timely data is essential for resource management and operational planning. Beyond these primary applications, airborne SAR systems are also used in various other fields, such as agriculture, urban planning, and infrastructure monitoring. In agriculture, SAR technology helps in crop monitoring, soil moisture assessment, and precision farming, contributing to increased agricultural productivity. In urban planning, SAR systems assist in mapping urban growth, monitoring infrastructure development, and assessing the impact of urbanization on the environment. The versatility and reliability of airborne SAR systems make them indispensable tools in a wide range of applications, driving their demand across different sectors. As technology continues to advance, the potential uses of airborne SAR systems are expected to expand, offering new opportunities for innovation and growth in the Global Airborne Synthetic Aperture Radar Market.

Global Airborne Synthetic Aperture Radar Market Outlook:

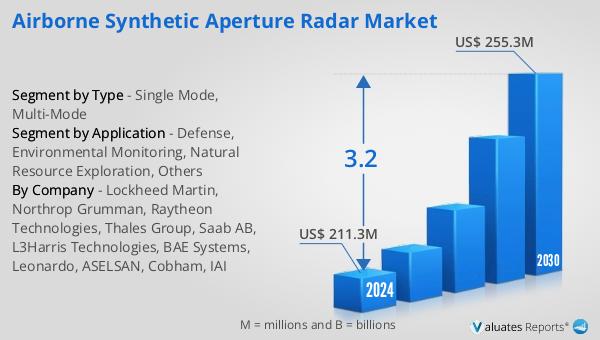

The outlook for the Global Airborne Synthetic Aperture Radar Market indicates a steady growth trajectory, with projections suggesting an increase from $211.3 million in 2024 to $255.3 million by 2030. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of 3.2% over the forecast period. A significant factor contributing to this market expansion is the substantial military expenditure by countries like the United States, which leads the world with a defense budget of $877 billion, accounting for 39% of global military spending. This high level of investment in defense underscores the importance of advanced surveillance and reconnaissance technologies, such as airborne SAR systems, in maintaining national security and strategic superiority. The increasing demand for precise and reliable imaging solutions in various sectors, including defense, environmental monitoring, and natural resource exploration, further fuels the market's growth. As governments and organizations worldwide recognize the value of airborne SAR technology in enhancing their operational capabilities, the adoption of these systems is expected to rise. The market's growth is also driven by continuous technological advancements, with manufacturers focusing on developing more efficient and versatile systems to meet the evolving needs of different industries. Overall, the Global Airborne Synthetic Aperture Radar Market presents significant opportunities for growth and development, driven by increasing demand and ongoing innovation in radar technology.

| Report Metric | Details |

| Report Name | Airborne Synthetic Aperture Radar Market |

| Accounted market size in 2024 | US$ 211.3 million |

| Forecasted market size in 2030 | US$ 255.3 million |

| CAGR | 3.2 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Lockheed Martin, Northrop Grumman, Raytheon Technologies, Thales Group, Saab AB, L3Harris Technologies, BAE Systems, Leonardo, ASELSAN, Cobham, IAI |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |