What is Global Drying And Storage Cabinet For Endoscope Market?

The Global Drying and Storage Cabinet for Endoscope Market is a specialized segment within the medical equipment industry, focusing on the development and distribution of cabinets designed to dry and store endoscopes. Endoscopes are essential medical devices used in various diagnostic and surgical procedures, and their proper maintenance is crucial to ensure patient safety and device longevity. These cabinets are engineered to provide optimal conditions for drying and storing endoscopes, preventing microbial contamination and ensuring that the devices are ready for use when needed. The market for these cabinets is driven by the increasing demand for endoscopic procedures, advancements in healthcare infrastructure, and the growing emphasis on infection control. As healthcare facilities strive to meet stringent regulatory standards and improve patient outcomes, the adoption of advanced drying and storage solutions for endoscopes is becoming increasingly important. This market is characterized by a range of products, including single-door, double-door, and multiple-door cabinets, each designed to meet the specific needs of different healthcare settings. With the ongoing advancements in technology and the rising awareness of infection prevention, the Global Drying and Storage Cabinet for Endoscope Market is poised for significant growth in the coming years.

Single Door Cabinet, Double Door Cabinet, Multiple Door Cabinet in the Global Drying And Storage Cabinet For Endoscope Market:

In the Global Drying and Storage Cabinet for Endoscope Market, the design and functionality of cabinets vary to cater to different healthcare facility needs. Single-door cabinets are typically compact and designed for smaller healthcare settings or facilities with limited space. These cabinets offer a straightforward solution for drying and storing a limited number of endoscopes, making them ideal for clinics or small hospitals where space and budget constraints are a concern. Despite their smaller size, single-door cabinets are equipped with essential features such as controlled airflow and temperature regulation to ensure effective drying and storage of endoscopes. On the other hand, double-door cabinets are more suitable for medium to large healthcare facilities that require the storage of a greater number of endoscopes. These cabinets provide enhanced capacity and often come with advanced features like automated drying cycles, HEPA filtration systems, and digital monitoring to ensure optimal storage conditions. The double-door design allows for better organization and accessibility, making it easier for healthcare professionals to manage multiple endoscopes efficiently. Multiple-door cabinets represent the most advanced and versatile option in the market, catering to large hospitals and specialized surgical centers with high volumes of endoscopic procedures. These cabinets offer the highest capacity and are equipped with state-of-the-art technology to ensure the highest standards of hygiene and efficiency. Features such as customizable storage configurations, real-time monitoring, and integration with hospital management systems make multiple-door cabinets an indispensable asset for large healthcare facilities. The choice between single-door, double-door, and multiple-door cabinets depends on various factors, including the size of the healthcare facility, the volume of endoscopic procedures performed, and the budget available for equipment investment. Each type of cabinet plays a crucial role in ensuring the safe and efficient management of endoscopes, ultimately contributing to improved patient care and infection control. As the demand for endoscopic procedures continues to rise, the need for reliable and efficient drying and storage solutions will remain a key focus for healthcare providers worldwide.

Hospitals, Ambulatory Surgical Centers, Clinics, Others in the Global Drying And Storage Cabinet For Endoscope Market:

The usage of Global Drying and Storage Cabinets for Endoscopes is critical across various healthcare settings, including hospitals, ambulatory surgical centers, clinics, and other medical facilities. In hospitals, these cabinets play a vital role in maintaining the hygiene and functionality of endoscopes, which are frequently used in diagnostic and surgical procedures. Hospitals often deal with a high volume of endoscopic procedures, necessitating the use of advanced drying and storage solutions to ensure that endoscopes are always ready for use and free from microbial contamination. The integration of these cabinets into hospital workflows helps streamline the process of endoscope reprocessing, reducing the risk of infection and improving patient safety. In ambulatory surgical centers, where efficiency and quick turnaround times are crucial, drying and storage cabinets for endoscopes are indispensable. These centers perform a wide range of outpatient surgical procedures, many of which require the use of endoscopes. The ability to quickly and effectively dry and store endoscopes ensures that these devices are available for consecutive procedures without compromising on safety or hygiene. Clinics, which may have limited resources compared to larger healthcare facilities, also benefit from the use of drying and storage cabinets. These cabinets provide a cost-effective solution for maintaining the cleanliness and readiness of endoscopes, allowing clinics to offer high-quality care to their patients. By investing in reliable drying and storage solutions, clinics can enhance their service offerings and ensure compliance with regulatory standards. Other healthcare facilities, such as specialized diagnostic centers and research institutions, also rely on drying and storage cabinets to maintain the integrity of their endoscopic equipment. These facilities often handle sensitive and complex procedures, making the proper maintenance of endoscopes a top priority. The use of drying and storage cabinets in these settings helps prevent equipment downtime and ensures that endoscopes are always in optimal condition for use. Overall, the adoption of Global Drying and Storage Cabinets for Endoscopes across various healthcare settings underscores the importance of infection control and equipment maintenance in delivering high-quality patient care.

Global Drying And Storage Cabinet For Endoscope Market Outlook:

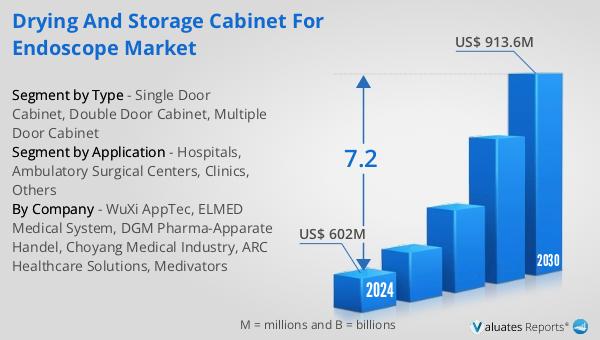

The outlook for the Global Drying and Storage Cabinet for Endoscope Market indicates a promising growth trajectory. The market is expected to expand from $602 million in 2024 to $913.6 million by 2030, reflecting a compound annual growth rate (CAGR) of 7.2% during the forecast period. This growth is driven by the increasing demand for endoscopic procedures, advancements in healthcare infrastructure, and the growing emphasis on infection control. As healthcare facilities strive to meet stringent regulatory standards and improve patient outcomes, the adoption of advanced drying and storage solutions for endoscopes is becoming increasingly important. In parallel, the global market for medical devices is estimated to be valued at $603 billion in 2023, with a projected CAGR of 5% over the next six years. This broader market growth is indicative of the rising demand for innovative medical technologies and solutions that enhance patient care and operational efficiency. The Global Drying and Storage Cabinet for Endoscope Market is poised to benefit from these trends, as healthcare providers continue to invest in state-of-the-art equipment to support their clinical operations. The increasing awareness of infection prevention and the need for reliable and efficient drying and storage solutions will remain key drivers of market growth in the coming years.

| Report Metric | Details |

| Report Name | Drying And Storage Cabinet For Endoscope Market |

| Accounted market size in 2024 | US$ 602 million |

| Forecasted market size in 2030 | US$ 913.6 million |

| CAGR | 7.2 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | WuXi AppTec, ELMED Medical System, DGM Pharma-Apparate Handel, Choyang Medical Industry, ARC Healthcare Solutions, Medivators |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |