What is Zeolite Membrane Separation System - Global Market?

Zeolite Membrane Separation Systems are advanced filtration technologies that utilize zeolite materials to separate different components in a mixture. Zeolites are microporous, aluminosilicate minerals that have a unique crystalline structure, allowing them to act as molecular sieves. This means they can selectively allow certain molecules to pass through while blocking others based on size and shape. The global market for these systems is growing due to their efficiency and effectiveness in various industrial applications. They are particularly valued for their ability to operate under high temperatures and pressures, making them suitable for challenging environments. Industries such as chemical processing, pharmaceuticals, and electronics are increasingly adopting these systems to enhance their production processes. The demand is driven by the need for more sustainable and energy-efficient separation technologies, as zeolite membranes often require less energy compared to traditional methods. As industries continue to seek greener solutions, the adoption of zeolite membrane separation systems is expected to rise, contributing to their expanding global market presence.

Pervaporation (PV) Separation System, Vapor Permeation (VP) Separation System in the Zeolite Membrane Separation System - Global Market:

Pervaporation (PV) and Vapor Permeation (VP) are two key separation processes that utilize zeolite membrane technology. Pervaporation involves the separation of liquid mixtures by partial vaporization through a membrane. In this process, a liquid feed mixture is brought into contact with one side of a zeolite membrane. The membrane selectively allows certain components to pass through as vapor, which is then collected on the other side. This method is particularly effective for separating azeotropic mixtures or those with close boiling points, which are challenging to separate using conventional distillation. The zeolite membrane's selectivity is crucial in determining which components are permeated, making it a highly efficient process for specific applications such as dehydration of alcohols and removal of volatile organic compounds from water. On the other hand, Vapor Permeation (VP) involves the separation of vapor mixtures. In this process, a vapor feed is introduced to the zeolite membrane, which selectively permeates certain components based on their molecular size and affinity to the membrane material. This technique is often used in the petrochemical industry for the separation of hydrocarbons and in the recovery of valuable solvents. Both PV and VP benefit from the inherent properties of zeolite membranes, such as thermal stability and chemical resistance, which allow them to operate under harsh conditions. The global market for these systems is expanding as industries recognize the advantages of zeolite membranes in improving separation efficiency and reducing energy consumption. The versatility of zeolite membranes in handling a wide range of feed compositions and operating conditions makes them an attractive choice for industries looking to optimize their separation processes. As environmental regulations become stricter, the demand for cleaner and more efficient separation technologies is expected to drive further growth in the adoption of PV and VP systems based on zeolite membranes.

Chemical, Pharmaceutical, Electronics and Engineering, Others in the Zeolite Membrane Separation System - Global Market:

Zeolite Membrane Separation Systems are utilized across various industries due to their unique properties and efficiency. In the chemical industry, these systems are employed for the separation and purification of chemical compounds. They are particularly useful in processes where traditional separation methods, such as distillation, are less effective or too energy-intensive. For instance, zeolite membranes can be used to separate isomers or to remove impurities from chemical mixtures, enhancing the purity and quality of the final product. In the pharmaceutical industry, zeolite membranes play a crucial role in the purification of active pharmaceutical ingredients (APIs). The ability of zeolite membranes to selectively separate molecules based on size and shape makes them ideal for isolating specific compounds from complex mixtures. This is essential in ensuring the efficacy and safety of pharmaceutical products. In the electronics and engineering sectors, zeolite membranes are used in the production of high-purity gases and solvents, which are critical for manufacturing processes. The precision and reliability of zeolite membrane separation systems help maintain the stringent quality standards required in these industries. Additionally, other sectors, such as environmental engineering, benefit from zeolite membranes in applications like water treatment and air purification. The ability to efficiently separate contaminants from water and air makes zeolite membranes a valuable tool in addressing environmental challenges. As industries continue to seek sustainable and efficient solutions, the adoption of zeolite membrane separation systems is likely to increase, further driving their global market growth.

Zeolite Membrane Separation System - Global Market Outlook:

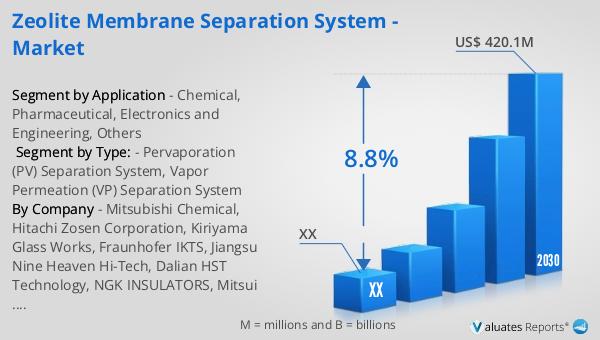

The global market for Zeolite Membrane Separation Systems was valued at approximately $242 million in 2023. It is projected to grow significantly, reaching an estimated size of $420.1 million by 2030, with a compound annual growth rate (CAGR) of 8.8% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for efficient and sustainable separation technologies across various industries. In North America, the market for these systems was valued at $ million in 2023, with expectations to reach $ million by 2030, maintaining a CAGR of % throughout the forecast period. The rising awareness of environmental concerns and the need for energy-efficient solutions are key factors driving this growth. As industries continue to innovate and adopt greener technologies, the demand for zeolite membrane separation systems is anticipated to rise, contributing to their expanding market presence globally. The versatility and efficiency of these systems make them an attractive choice for industries looking to optimize their processes and reduce their environmental footprint.

| Report Metric | Details |

| Report Name | Zeolite Membrane Separation System - Market |

| Forecasted market size in 2030 | US$ 420.1 million |

| CAGR | 8.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Mitsubishi Chemical, Hitachi Zosen Corporation, Kiriyama Glass Works, Fraunhofer IKTS, Jiangsu Nine Heaven Hi-Tech, Dalian HST Technology, NGK INSULATORS, Mitsui E&S Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |