What is Global Pile Driver Market?

The Global Pile Driver Market refers to the worldwide industry involved in the manufacturing, distribution, and utilization of pile drivers. Pile drivers are essential construction equipment used to drive piles into the soil to provide foundational support for buildings, bridges, and other structures. These machines are crucial for ensuring the stability and integrity of various construction projects, especially in areas with unstable soil conditions. The market encompasses a wide range of pile driving equipment, including static pile drivers, piling hammers, piling rigs, and casing rotators. The demand for pile drivers is driven by the growth in construction activities, urbanization, and infrastructure development across the globe. As countries continue to invest in building and upgrading their infrastructure, the need for reliable and efficient pile driving equipment is expected to rise. The market is characterized by technological advancements, with manufacturers focusing on developing more efficient, environmentally friendly, and cost-effective solutions to meet the evolving needs of the construction industry.

Static Pile Drivers, Piling Hammers, Piling Rigs, Casing Rotator in the Global Pile Driver Market:

Static pile drivers, piling hammers, piling rigs, and casing rotators are key components of the Global Pile Driver Market, each serving distinct functions in the pile driving process. Static pile drivers are used to press piles into the ground using hydraulic pressure, making them suitable for noise-sensitive areas and urban environments where vibration and noise must be minimized. They are known for their precision and ability to handle various soil conditions. Piling hammers, on the other hand, use impact force to drive piles into the ground. These can be hydraulic, diesel, or air-powered, and are chosen based on the specific requirements of the project, such as the type of soil and the size of the piles. Piling rigs are versatile machines that can perform multiple functions, including drilling, driving, and extracting piles. They are equipped with various attachments and can be used for different types of piling techniques, making them highly adaptable to different construction needs. Casing rotators are specialized equipment used in the construction of deep foundations, particularly in hard soil or rock conditions. They rotate the casing pipe to cut through the soil, allowing for the insertion of piles or other structural elements. Each of these machines plays a crucial role in ensuring the stability and safety of construction projects, and their usage is determined by the specific requirements of the site and the type of structure being built. The integration of advanced technologies in these machines, such as GPS and automated controls, has further enhanced their efficiency and precision, making them indispensable tools in modern construction.

Buildings Construction, Transport Infrastructure Construction, Others in the Global Pile Driver Market:

The Global Pile Driver Market finds extensive usage in various areas, including buildings construction, transport infrastructure construction, and other sectors. In buildings construction, pile drivers are essential for creating strong foundations for residential, commercial, and industrial buildings. They ensure that the structures are stable and can withstand various environmental conditions, such as earthquakes and heavy loads. The use of pile drivers in this sector is crucial for high-rise buildings, where deep foundations are necessary to support the weight and height of the structure. In transport infrastructure construction, pile drivers are used to build bridges, highways, railways, and ports. These structures require robust foundations to handle the dynamic loads and stresses associated with transportation activities. Pile drivers help in driving piles deep into the ground, providing the necessary support for these large-scale infrastructure projects. The efficiency and precision of modern pile driving equipment have made it possible to complete these projects faster and with greater accuracy, reducing construction time and costs. In other sectors, pile drivers are used in the construction of offshore platforms, wind farms, and other specialized structures. Offshore platforms, for instance, require piles to be driven into the seabed to provide stability in the harsh marine environment. Wind farms also rely on pile drivers to install the foundations for wind turbines, ensuring they remain stable and operational even in strong winds. The versatility and adaptability of pile driving equipment make them suitable for a wide range of applications, contributing to the growth and development of various industries.

Global Pile Driver Market Outlook:

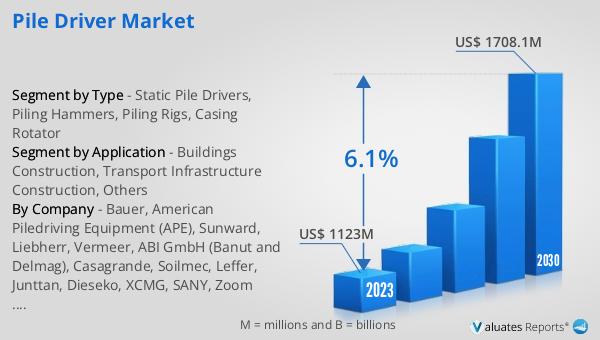

The global Pile Driver market is anticipated to expand from US$ 1197.3 million in 2024 to US$ 1708.1 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 6.1% during the forecast period. This growth is driven by the increasing demand for construction activities worldwide, as countries invest in infrastructure development and urbanization. The need for reliable and efficient pile driving equipment is paramount to ensure the stability and safety of various construction projects. Technological advancements in pile driving equipment, such as the integration of GPS and automated controls, have further enhanced their efficiency and precision, making them indispensable tools in modern construction. The market is also characterized by a focus on developing environmentally friendly and cost-effective solutions to meet the evolving needs of the construction industry. As the demand for infrastructure development continues to rise, the Global Pile Driver Market is expected to witness significant growth, providing ample opportunities for manufacturers and stakeholders in the industry.

| Report Metric | Details |

| Report Name | Pile Driver Market |

| Accounted market size in 2024 | US$ 1197.3 in million |

| Forecasted market size in 2030 | US$ 1708.1 million |

| CAGR | 6.1 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Bauer, American Piledriving Equipment (APE), Sunward, Liebherr, Vermeer, ABI GmbH (Banut and Delmag), Casagrande, Soilmec, Leffer, Junttan, Dieseko, XCMG, SANY, Zoom Lion, Nippon Sharyo, SEM, Yongan Machinery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |