What is Global FPC Market?

The Global Flexible Printed Circuit (FPC) Market is a rapidly evolving sector within the electronics industry. FPCs are essential components used in various electronic devices due to their flexibility, lightweight nature, and ability to fit into compact spaces. These circuits are made by printing conductive pathways on flexible substrates, allowing them to bend and twist without breaking. This adaptability makes them ideal for modern electronic devices that require compact and intricate designs. The market for FPCs is driven by the increasing demand for consumer electronics, advancements in medical devices, and the growing need for sophisticated automotive electronics. Additionally, the aerospace and defense sectors are also significant contributors to the market's growth, as they require reliable and durable electronic components. As technology continues to advance, the applications and demand for FPCs are expected to expand further, making the Global FPC Market a critical area of focus for manufacturers and researchers alike.

Single-sided Circuit, Double-sided Circuit, Multi-layer Circuit, Rigid-Flex Circuit in the Global FPC Market:

Single-sided circuits, double-sided circuits, multi-layer circuits, and rigid-flex circuits are the primary types of FPCs in the Global FPC Market. Single-sided circuits are the simplest form, featuring a single layer of conductive material on one side of the flexible substrate. These are commonly used in applications where space is limited, and the circuit's complexity is minimal. Double-sided circuits, on the other hand, have conductive material on both sides of the substrate, allowing for more complex designs and increased functionality. They are widely used in consumer electronics, automotive, and industrial applications. Multi-layer circuits take this a step further by incorporating multiple layers of conductive material separated by insulating layers. This design allows for even more complex and high-density circuit configurations, making them suitable for advanced medical devices, aerospace, and high-performance computing applications. Rigid-flex circuits combine the benefits of both rigid and flexible circuits, offering a hybrid solution that can withstand mechanical stress while maintaining flexibility. These circuits are particularly useful in applications that require both durability and adaptability, such as in military and aerospace equipment. Each type of circuit has its unique advantages and is chosen based on the specific requirements of the application, contributing to the diverse and dynamic nature of the Global FPC Market.

Medical, Aerospace and Defense or Military, Consumer Electronics, Automotive, Others in the Global FPC Market:

The usage of FPCs in various sectors highlights their versatility and importance. In the medical field, FPCs are used in devices such as pacemakers, hearing aids, and diagnostic equipment. Their flexibility and reliability are crucial for ensuring the proper functioning of these life-saving devices. In the aerospace and defense sectors, FPCs are used in communication systems, navigation equipment, and other critical components. Their ability to withstand harsh environments and mechanical stress makes them ideal for these demanding applications. Consumer electronics is another major area where FPCs are extensively used. Smartphones, tablets, laptops, and wearable devices all rely on FPCs for their compact and intricate designs. The automotive industry also benefits from FPCs, using them in various electronic systems such as infotainment, navigation, and safety features. The adaptability and durability of FPCs make them suitable for the challenging conditions within vehicles. Other sectors, such as industrial automation and telecommunications, also utilize FPCs for their advanced electronic systems. The widespread usage of FPCs across these diverse sectors underscores their critical role in modern technology and their contribution to the growth of the Global FPC Market.

Global FPC Market Outlook:

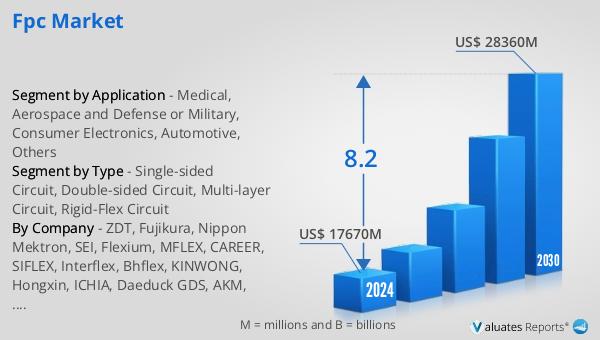

The global FPC market is anticipated to expand significantly, with projections indicating growth from US$ 17,670 million in 2024 to US$ 28,360 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 8.2% during the forecast period. The market is dominated by the top four manufacturers, who collectively hold a share exceeding 25%. Among the various product types, double-sided circuits represent the largest segment, accounting for over 60% of the market share. This substantial growth is driven by the increasing demand for advanced electronic devices across various sectors, including consumer electronics, automotive, medical, aerospace, and defense. The continuous advancements in technology and the need for more compact, reliable, and efficient electronic components are key factors contributing to the market's expansion. As the demand for sophisticated electronic devices continues to rise, the Global FPC Market is poised for sustained growth, making it a vital area of focus for industry stakeholders.

| Report Metric | Details |

| Report Name | FPC Market |

| Accounted market size in 2024 | US$ 17670 in million |

| Forecasted market size in 2030 | US$ 28360 million |

| CAGR | 8.2 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | ZDT, Fujikura, Nippon Mektron, SEI, Flexium, MFLEX, CAREER, SIFLEX, Interflex, Bhflex, KINWONG, Hongxin, ICHIA, Daeduck GDS, AKM, Multek, JCD, Topsun, MFS, Netron Soft-Tech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |