What is Global Printed Electronics Products Market?

The Global Printed Electronics Products Market is a rapidly evolving sector that focuses on the development and commercialization of electronic devices produced through printing technologies. This market encompasses a wide range of products, including flexible displays, sensors, and photovoltaic cells, which are manufactured using various printing techniques. The primary advantage of printed electronics is their ability to be produced on flexible substrates, allowing for lightweight, thin, and cost-effective electronic components. This flexibility opens up new possibilities for integrating electronics into everyday objects, creating innovative applications across different industries. The market is driven by the increasing demand for lightweight, flexible, and cost-effective electronic solutions, as well as advancements in printing technologies that enable high-resolution and high-speed production. As industries continue to seek more efficient and versatile electronic components, the Global Printed Electronics Products Market is poised for significant growth, offering new opportunities for innovation and application in various fields.

Inkjet, Gravure, Screen, Flexography, Others in the Global Printed Electronics Products Market:

Inkjet, gravure, screen, flexography, and other printing techniques play a crucial role in the Global Printed Electronics Products Market, each offering unique advantages and applications. Inkjet printing is a versatile and widely used method in printed electronics due to its ability to precisely deposit small droplets of ink onto a substrate. This technique is ideal for creating intricate patterns and is often used in the production of flexible displays, sensors, and RFID tags. Inkjet printing allows for rapid prototyping and customization, making it a popular choice for research and development in the printed electronics field. Gravure printing, on the other hand, is known for its high-speed production capabilities and is commonly used for large-scale manufacturing of printed electronics. This technique involves engraving the desired pattern onto a cylinder, which is then used to transfer ink onto the substrate. Gravure printing is particularly suitable for producing large volumes of consistent and high-quality printed electronics, such as photovoltaic cells and printed batteries. Screen printing is another widely used technique in the printed electronics market, known for its simplicity and versatility. It involves using a mesh screen to transfer ink onto a substrate, creating a wide range of electronic components, including sensors, displays, and circuits. Screen printing is particularly advantageous for producing thick, conductive layers, making it ideal for applications that require robust and durable electronic components. Flexography is a printing technique that uses flexible relief plates to transfer ink onto a substrate. This method is known for its ability to print on a variety of materials, including flexible and rigid substrates, making it suitable for a wide range of printed electronics applications. Flexography is often used in the production of packaging materials with integrated electronic components, such as smart labels and RFID tags. Other printing techniques, such as offset and digital printing, also contribute to the Global Printed Electronics Products Market, each offering unique benefits and applications. These techniques enable the production of innovative electronic components that are lightweight, flexible, and cost-effective, driving the growth and development of the printed electronics industry.

Smart Cards, Sensors, Printed Batteries, RFID Tags, OLED, Others in the Global Printed Electronics Products Market:

The Global Printed Electronics Products Market finds extensive usage across various applications, including smart cards, sensors, printed batteries, RFID tags, OLEDs, and others. Smart cards, which are widely used in banking, transportation, and identification, benefit from printed electronics by incorporating flexible and cost-effective electronic components. Printed electronics enable the integration of advanced features, such as contactless communication and enhanced security, into smart cards, making them more versatile and efficient. Sensors, another key application area, leverage printed electronics to create lightweight, flexible, and low-cost sensing solutions. These sensors are used in a wide range of industries, including healthcare, automotive, and consumer electronics, for applications such as environmental monitoring, health diagnostics, and motion detection. Printed batteries, which are essential for powering various electronic devices, benefit from the advancements in printed electronics by offering lightweight, flexible, and environmentally friendly energy storage solutions. These batteries are used in applications such as wearable devices, IoT devices, and portable electronics, where traditional batteries may be too bulky or rigid. RFID tags, which are widely used for tracking and identification purposes, also benefit from printed electronics by enabling the production of low-cost, flexible, and durable tags. These tags are used in various industries, including retail, logistics, and healthcare, for applications such as inventory management, asset tracking, and patient identification. OLEDs, or organic light-emitting diodes, are another significant application area for printed electronics. These displays offer high-resolution, flexible, and energy-efficient solutions for a wide range of applications, including televisions, smartphones, and wearable devices. The use of printed electronics in OLED production allows for the creation of innovative display technologies that are lightweight, thin, and capable of being integrated into various form factors. Other applications of printed electronics include photovoltaic cells, which harness solar energy to generate electricity, and electronic textiles, which integrate electronic components into fabrics for applications such as smart clothing and wearable technology. The versatility and cost-effectiveness of printed electronics make them an attractive solution for a wide range of applications, driving the growth and development of the Global Printed Electronics Products Market.

Global Printed Electronics Products Market Outlook:

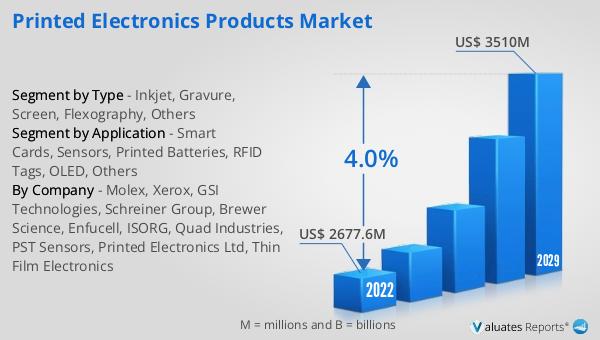

The global market for Printed Electronics Products was valued at approximately $2,874 million in 2024, and it is anticipated to expand to a revised size of around $3,767 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 4.0% over the forecast period. The steady increase in market size reflects the growing demand for innovative and cost-effective electronic solutions across various industries. As the market continues to evolve, advancements in printing technologies and materials are expected to drive further growth and development. The increasing adoption of printed electronics in applications such as smart cards, sensors, and OLEDs is a testament to the market's potential and versatility. The ability to produce lightweight, flexible, and environmentally friendly electronic components is a key factor contributing to the market's expansion. As industries continue to seek more efficient and sustainable solutions, the Global Printed Electronics Products Market is poised to play a significant role in shaping the future of electronics. The projected growth in market size underscores the importance of printed electronics in addressing the evolving needs of various industries and applications.

| Report Metric |

Details |

| Report Name |

Printed Electronics Products Market |

| Accounted market size in year |

US$ 2874 million |

| Forecasted market size in 2031 |

US$ 3767 million |

| CAGR |

4.0% |

| Base Year |

year |

| Forecasted years |

2025 - 2031 |

| Segment by Type |

- Inkjet

- Gravure

- Screen

- Flexography

- Others

|

| Segment by Application |

- Smart Cards

- Sensors

- Printed Batteries

- RFID Tags

- OLED

- Others

|

| By Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia) Rest of Europe

- Nordic Countries

- Asia-Pacific (China, Japan, South Korea)

- Southeast Asia (India, Australia)

- Rest of Asia

- Latin America (Mexico, Brazil)

- Rest of Latin America

- Middle East & Africa (Turkey, Saudi Arabia, UAE, Rest of MEA)

|

| By Company |

Molex, Xerox, GSI Technologies, Schreiner Group, Brewer Science, Enfucell, ISORG, Quad Industries, PST Sensors, Printed Electronics Ltd, Thin Film Electronics |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |