What is Global VCI Aerosols Market?

The Global VCI (Vapor Corrosion Inhibitor) Aerosols Market is a specialized segment within the broader corrosion protection industry. VCI aerosols are innovative products designed to prevent corrosion on metal surfaces by releasing a vapor that forms a protective layer. This layer inhibits the electrochemical reactions that cause rust and corrosion, making these aerosols particularly valuable in industries where metal preservation is crucial. The market for VCI aerosols is driven by the increasing demand for effective and convenient corrosion protection solutions across various sectors, including automotive, aerospace, and manufacturing. These aerosols are favored for their ease of application, portability, and ability to provide long-lasting protection without the need for extensive surface preparation. As industries continue to seek efficient ways to extend the lifespan of their metal components and reduce maintenance costs, the demand for VCI aerosols is expected to grow. Additionally, the market is influenced by advancements in aerosol technology and the development of eco-friendly formulations that meet stringent environmental regulations. Overall, the Global VCI Aerosols Market represents a dynamic and evolving industry, with significant potential for growth as industries prioritize corrosion prevention and sustainability.

Organic, Inorganic in the Global VCI Aerosols Market:

In the Global VCI Aerosols Market, products are typically categorized based on their chemical composition, primarily into organic and inorganic types. Organic VCI aerosols are formulated using organic compounds that are often derived from natural sources. These compounds are known for their ability to form a protective barrier on metal surfaces, effectively preventing moisture and oxygen from initiating the corrosion process. Organic VCI aerosols are particularly valued for their environmental friendliness, as they tend to be biodegradable and less harmful to the ecosystem. They are often used in applications where environmental regulations are stringent, and there is a need for sustainable corrosion protection solutions. On the other hand, inorganic VCI aerosols are composed of inorganic compounds, which are typically more robust and offer superior protection in harsh environments. These aerosols are favored in industries where metal components are exposed to extreme conditions, such as high temperatures or corrosive chemicals. Inorganic VCI aerosols are known for their durability and long-lasting protection, making them ideal for heavy-duty applications. However, they may not be as environmentally friendly as their organic counterparts, which can be a consideration for industries aiming to reduce their ecological footprint. The choice between organic and inorganic VCI aerosols often depends on the specific requirements of the application, including the level of protection needed, environmental considerations, and cost-effectiveness. As the Global VCI Aerosols Market continues to evolve, manufacturers are investing in research and development to create advanced formulations that combine the benefits of both organic and inorganic compounds. This has led to the emergence of hybrid VCI aerosols that offer enhanced performance and sustainability. These hybrid products are designed to provide superior corrosion protection while minimizing environmental impact, making them an attractive option for industries seeking innovative solutions. Additionally, the market is witnessing a trend towards the development of customized VCI aerosols tailored to meet the unique needs of different industries and applications. This customization allows for more targeted and efficient corrosion protection, further driving the demand for VCI aerosols in the global market. Overall, the distinction between organic and inorganic VCI aerosols highlights the diverse range of options available to industries seeking effective corrosion protection solutions. As the market continues to grow, the focus on sustainability and innovation is expected to drive the development of new and improved VCI aerosol products that meet the evolving needs of industries worldwide.

Oil & Gas, Power Generation, Paper & Pulp, Metal Processing, Chemical Processing, Water Treatment, Others in the Global VCI Aerosols Market:

The Global VCI Aerosols Market finds extensive usage across various industries, each with unique requirements for corrosion protection. In the oil and gas sector, VCI aerosols are crucial for maintaining the integrity of metal components exposed to harsh environments, such as offshore platforms and pipelines. These aerosols provide a protective barrier against the corrosive effects of saltwater, chemicals, and extreme temperatures, ensuring the longevity and reliability of critical infrastructure. In the power generation industry, VCI aerosols are used to protect metal parts in turbines, generators, and other equipment from corrosion caused by moisture and environmental pollutants. This helps in reducing maintenance costs and preventing unexpected equipment failures, thereby ensuring uninterrupted power supply. The paper and pulp industry also benefits from VCI aerosols, as they help in preserving the metal components of machinery used in the production process. These aerosols prevent rust and corrosion, which can lead to costly downtime and repairs. In metal processing, VCI aerosols are used to protect raw materials and finished products during storage and transportation. They ensure that metal surfaces remain free from corrosion, maintaining their quality and appearance. The chemical processing industry relies on VCI aerosols to protect equipment and storage tanks from the corrosive effects of chemicals and moisture. This is essential for maintaining the safety and efficiency of chemical processing operations. In water treatment facilities, VCI aerosols are used to protect metal components from corrosion caused by exposure to water and chemicals. This helps in extending the lifespan of equipment and reducing maintenance costs. Other industries, such as automotive, aerospace, and manufacturing, also utilize VCI aerosols to protect metal parts and components from corrosion. These aerosols are particularly valuable in applications where metal surfaces are exposed to moisture, chemicals, or extreme temperatures. Overall, the Global VCI Aerosols Market plays a vital role in ensuring the longevity and reliability of metal components across a wide range of industries. By providing effective and convenient corrosion protection, VCI aerosols help industries reduce maintenance costs, prevent equipment failures, and extend the lifespan of their assets.

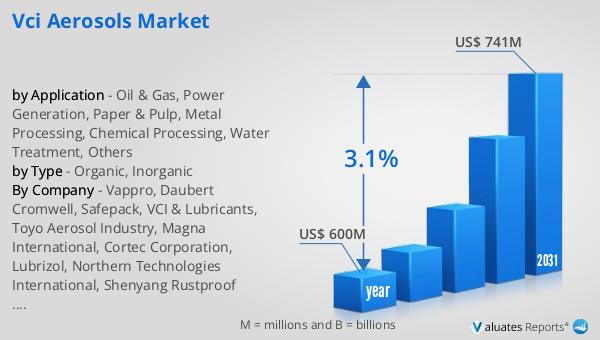

Global VCI Aerosols Market Outlook:

The global market for VCI Aerosols was valued at $600 million in 2024, and it is anticipated to expand to a revised size of $741 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.1% during the forecast period. This growth trajectory underscores the increasing demand for effective corrosion protection solutions across various industries. The steady rise in market value can be attributed to several factors, including the growing awareness of the benefits of VCI aerosols in preventing corrosion and extending the lifespan of metal components. As industries continue to prioritize cost-effective and sustainable solutions, the demand for VCI aerosols is expected to rise. The market's expansion is also driven by advancements in aerosol technology, which have led to the development of more efficient and environmentally friendly formulations. These innovations are particularly appealing to industries that are subject to stringent environmental regulations and are seeking to reduce their ecological footprint. Additionally, the increasing focus on infrastructure development and industrialization in emerging economies is expected to contribute to the market's growth. As these economies invest in new infrastructure and manufacturing facilities, the demand for corrosion protection solutions, including VCI aerosols, is likely to increase. Overall, the Global VCI Aerosols Market is poised for steady growth, driven by the need for effective corrosion protection solutions and the ongoing advancements in aerosol technology.

| Report Metric | Details |

| Report Name | VCI Aerosols Market |

| Accounted market size in year | US$ 600 million |

| Forecasted market size in 2031 | US$ 741 million |

| CAGR | 3.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Vappro, Daubert Cromwell, Safepack, VCI & Lubricants, Toyo Aerosol Industry, Magna International, Cortec Corporation, Lubrizol, Northern Technologies International, Shenyang Rustproof Packaging Material, Whitebird, Rustx |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |