What is Global Nano Dense Film Market?

The Global Nano Dense Film Market is a rapidly evolving sector that focuses on the production and application of ultra-thin films at the nanoscale. These films, often just a few nanometers thick, are engineered to possess unique properties that make them highly valuable across various industries. The market is driven by the increasing demand for advanced materials that can enhance the performance and efficiency of products. Nano dense films are used in a wide range of applications, from electronics and energy to healthcare and automotive industries. They are known for their exceptional strength, flexibility, and conductivity, which make them ideal for use in cutting-edge technologies. The market is characterized by continuous research and development efforts aimed at discovering new applications and improving the properties of these films. As industries seek to innovate and improve their products, the demand for nano dense films is expected to grow, making this market a key area of interest for researchers and businesses alike. The global market for these films is poised for significant growth, driven by technological advancements and the increasing need for high-performance materials.

Liquid Phase Method, Gas Phase Method in the Global Nano Dense Film Market:

The Liquid Phase Method and Gas Phase Method are two primary techniques used in the production of nano dense films, each offering distinct advantages and applications. The Liquid Phase Method involves the deposition of materials from a liquid solution onto a substrate, forming a thin film. This method is particularly advantageous for its simplicity and cost-effectiveness, making it suitable for large-scale production. It allows for precise control over the film's thickness and composition, which is crucial for tailoring the film's properties to specific applications. The Liquid Phase Method is widely used in the production of films for electronic devices, where uniformity and precision are paramount. On the other hand, the Gas Phase Method involves the deposition of materials from a vapor phase onto a substrate. This method is known for its ability to produce highly pure and uniform films, making it ideal for applications that require high-quality coatings. The Gas Phase Method is often used in the semiconductor industry, where the purity and uniformity of films are critical for device performance. Both methods have their unique advantages and are chosen based on the specific requirements of the application. The choice between the Liquid Phase and Gas Phase Methods depends on factors such as the desired film properties, production scale, and cost considerations. As the demand for nano dense films continues to grow, advancements in these methods are expected to play a crucial role in meeting the needs of various industries. Researchers are continually exploring new techniques and materials to enhance the performance and efficiency of these methods, ensuring that they remain at the forefront of nano film production. The ongoing development of these methods is essential for the continued growth and innovation in the Global Nano Dense Film Market.

Energy, Electronic, Others in the Global Nano Dense Film Market:

The Global Nano Dense Film Market finds extensive usage in various sectors, including energy, electronics, and others, due to the unique properties of these films. In the energy sector, nano dense films are used to improve the efficiency and performance of solar cells and batteries. Their exceptional conductivity and ability to enhance light absorption make them ideal for use in photovoltaic cells, where they can significantly increase energy conversion efficiency. Additionally, these films are used in the development of advanced battery technologies, where they help improve energy storage capacity and charge-discharge rates. In the electronics industry, nano dense films are used in the production of high-performance electronic devices, such as transistors, sensors, and displays. Their ability to provide excellent electrical conductivity and flexibility makes them suitable for use in flexible electronics and wearable devices. These films are also used in the development of advanced semiconductor devices, where their uniformity and purity are critical for device performance. Beyond energy and electronics, nano dense films are used in various other applications, including healthcare, automotive, and aerospace industries. In healthcare, these films are used in the development of advanced medical devices and drug delivery systems, where their biocompatibility and precision are essential. In the automotive and aerospace industries, nano dense films are used to enhance the performance and durability of components, providing lightweight and strong materials that can withstand harsh conditions. The versatility and unique properties of nano dense films make them a valuable material across multiple industries, driving their demand and application in various fields. As industries continue to seek innovative solutions to improve their products and processes, the usage of nano dense films is expected to expand, further fueling the growth of the Global Nano Dense Film Market.

Global Nano Dense Film Market Outlook:

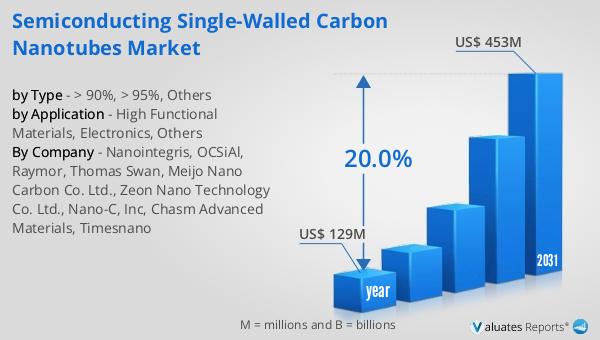

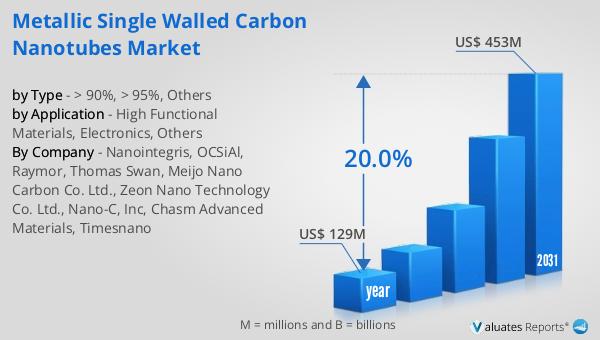

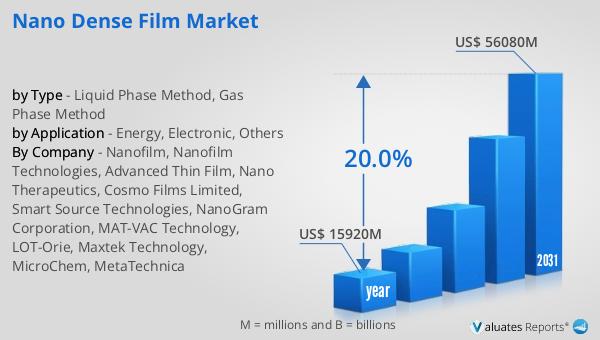

The global market for Nano Dense Film was valued at approximately $15.92 billion in 2024, and it is anticipated to experience substantial growth, reaching an estimated size of $56.08 billion by 2031. This impressive expansion is driven by a compound annual growth rate (CAGR) of 20.0% during the forecast period. The market's robust growth can be attributed to the increasing demand for advanced materials that offer superior performance and efficiency across various industries. As technological advancements continue to drive innovation, the need for high-performance materials like nano dense films is expected to rise. These films are becoming increasingly important in sectors such as electronics, energy, healthcare, and automotive, where their unique properties can significantly enhance product performance. The market's growth is also supported by ongoing research and development efforts aimed at discovering new applications and improving the properties of these films. As industries continue to seek innovative solutions to improve their products and processes, the demand for nano dense films is expected to expand, further fueling the growth of the Global Nano Dense Film Market. The market's potential for growth presents significant opportunities for businesses and researchers looking to capitalize on the increasing demand for high-performance materials.

| Report Metric | Details |

| Report Name | Nano Dense Film Market |

| Accounted market size in year | US$ 15920 million |

| Forecasted market size in 2031 | US$ 56080 million |

| CAGR | 20.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Nanofilm, Nanofilm Technologies, Advanced Thin Film, Nano Therapeutics, Cosmo Films Limited, Smart Source Technologies, NanoGram Corporation, MAT-VAC Technology, LOT-Orie, Maxtek Technology, MicroChem, MetaTechnica |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |