What is Global 25G Laser Chips Market?

The Global 25G Laser Chips Market refers to the industry focused on the production and distribution of laser chips capable of transmitting data at a rate of 25 gigabits per second (25G). These laser chips are integral components in optical communication systems, enabling high-speed data transmission over fiber optic networks. As the demand for faster internet speeds and more efficient data centers grows, the need for advanced laser chips like the 25G variants becomes increasingly critical. These chips are used in various applications, including telecommunications, data centers, and other industries that require rapid data transfer capabilities. The market for 25G laser chips is expanding due to technological advancements and the increasing adoption of high-speed internet services worldwide. As businesses and consumers alike demand faster and more reliable internet connections, the 25G laser chips market is poised for significant growth, driven by innovations in semiconductor technology and the ongoing expansion of global communication networks. The market's growth is also fueled by the rising need for efficient data management and storage solutions, which are essential for supporting the ever-increasing volume of digital information generated by modern society.

FP Laser Chip, DFB Laser Chip, EML Laser Chip, VCSEL Laser Chip in the Global 25G Laser Chips Market:

In the Global 25G Laser Chips Market, several types of laser chips play crucial roles, each with unique characteristics and applications. The FP (Fabry-Pérot) Laser Chip is one of the simplest forms of laser chips, known for its cost-effectiveness and ease of production. It operates by reflecting light between two mirrors, creating a standing wave that amplifies the light. FP laser chips are commonly used in applications where cost is a significant factor, and high precision is not as critical, such as in short-distance communication systems. On the other hand, the DFB (Distributed Feedback) Laser Chip offers higher precision and stability. It uses a diffraction grating to provide feedback, which helps maintain a single wavelength of light. This makes DFB laser chips ideal for long-distance communication and applications requiring high data integrity, such as in telecommunications networks. The EML (Electro-absorption Modulated Laser) Chip combines a laser with an electro-absorption modulator, allowing for direct modulation of the laser light. This integration results in high-speed data transmission capabilities, making EML chips suitable for high-performance applications like data centers and advanced communication systems. Lastly, the VCSEL (Vertical-Cavity Surface-Emitting Laser) Chip is known for its efficiency and ability to emit light perpendicular to the surface of the chip. VCSELs are widely used in data communication, sensing, and 3D imaging applications due to their low power consumption and high modulation speeds. Each of these laser chip types contributes to the overall growth and diversification of the Global 25G Laser Chips Market, catering to different needs and technological advancements in the industry.

Communication Industry, Data Center, Other in the Global 25G Laser Chips Market:

The Global 25G Laser Chips Market finds extensive usage across various sectors, with the communication industry being one of the primary beneficiaries. In the communication industry, 25G laser chips are essential for enabling high-speed internet and telecommunication services. They facilitate the rapid transmission of large volumes of data over fiber optic networks, ensuring seamless connectivity and efficient communication. As the demand for faster and more reliable internet services continues to rise, the adoption of 25G laser chips in the communication industry is expected to grow significantly. These chips are crucial for supporting the infrastructure needed for advanced communication technologies, such as 5G networks and beyond. In data centers, 25G laser chips play a vital role in managing the massive amounts of data generated and processed daily. They enable high-speed data transfer between servers, storage systems, and networking equipment, ensuring efficient data management and reducing latency. As data centers continue to expand to accommodate the growing demand for cloud computing and data storage solutions, the need for advanced laser chips like the 25G variants becomes increasingly important. Additionally, 25G laser chips are used in various other applications, including industrial automation, medical imaging, and scientific research. In these areas, the chips facilitate precise and rapid data transmission, supporting the development of innovative technologies and solutions. The versatility and high performance of 25G laser chips make them indispensable in a wide range of industries, driving their adoption and contributing to the overall growth of the Global 25G Laser Chips Market.

Global 25G Laser Chips Market Outlook:

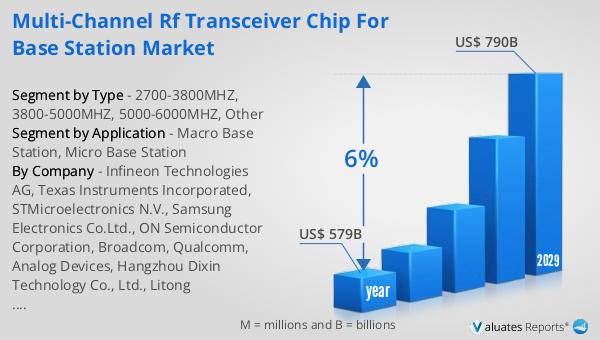

This analysis examines laser chips with a 25G transmission rate. The Global 25G Laser Chips Market is anticipated to expand from $1,017 million in 2024 to $2,364.7 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 15.1% during the forecast period. In parallel, the global semiconductor market, valued at $579 billion in 2022, is projected to reach $790 billion by 2029, growing at a CAGR of 6% over the same period. This growth underscores the increasing demand for advanced semiconductor technologies, including 25G laser chips, driven by the need for faster and more efficient data transmission solutions. As industries continue to evolve and embrace digital transformation, the role of high-speed laser chips becomes increasingly critical in supporting the infrastructure required for modern communication and data management systems. The projected growth of the 25G Laser Chips Market highlights the importance of these components in meeting the demands of a rapidly changing technological landscape, where speed, efficiency, and reliability are paramount.

| Report Metric | Details |

| Report Name | 25G Laser Chips Market |

| Accounted market size in 2024 | US$ 1017 in million |

| Forecasted market size in 2030 | US$ 2364.7 million |

| CAGR | 15.1 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | MACOM, LandMark Optoelectronics Corporation (LMOC), Suzhou Everbright Photonics Co., Ltd., YuanjieSemiconductorTechnology Co., Ltd., Toptrans (Suzhou) Corporation, Optocom Corporation, Broadcom, Mitsubishi Electric, Sumitomo Electric Industries Co.,Ltd., EMCORE Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |