What is Global Hydrogen Fuel Cells for Vehicles Market?

The Global Hydrogen Fuel Cells for Vehicles Market is an emerging sector that focuses on the development and deployment of hydrogen fuel cell technology in the automotive industry. Hydrogen fuel cells are devices that convert hydrogen gas into electricity through a chemical reaction with oxygen, producing only water and heat as byproducts. This makes them an environmentally friendly alternative to traditional internal combustion engines, which emit harmful pollutants. The market encompasses a wide range of applications, including passenger cars, commercial vehicles, and public transportation systems. As governments and industries worldwide seek to reduce carbon emissions and transition to cleaner energy sources, the demand for hydrogen fuel cell vehicles is expected to grow. This market is driven by technological advancements, supportive government policies, and increasing consumer awareness of environmental issues. Companies in this sector are investing heavily in research and development to improve the efficiency, durability, and cost-effectiveness of hydrogen fuel cells, making them a viable option for mass-market adoption. The Global Hydrogen Fuel Cells for Vehicles Market represents a significant opportunity for innovation and growth in the automotive industry, as it aligns with global efforts to combat climate change and promote sustainable transportation solutions.

Below 80KW, 80-120KW, 120-150KW, 150-240KW, Above 240KW in the Global Hydrogen Fuel Cells for Vehicles Market:

In the Global Hydrogen Fuel Cells for Vehicles Market, power output categories play a crucial role in determining the suitability of fuel cells for different types of vehicles. The power output is measured in kilowatts (KW) and is a key factor in the performance and application of hydrogen fuel cells. The category "Below 80KW" typically includes smaller fuel cells that are suitable for light-duty vehicles and some passenger cars. These fuel cells are designed for efficiency and compactness, making them ideal for vehicles that require less power and have limited space for fuel cell installation. The "80-120KW" range is more versatile, catering to a broader spectrum of passenger cars and light commercial vehicles. This power range offers a balance between performance and efficiency, making it a popular choice for manufacturers looking to integrate hydrogen fuel cells into their vehicle lineup. Moving up the scale, the "120-150KW" category is often used in larger passenger vehicles and medium-duty commercial vehicles. These fuel cells provide more power, enabling vehicles to achieve higher speeds and carry heavier loads. The "150-240KW" range is typically reserved for heavy-duty commercial vehicles, such as buses and trucks, which require substantial power to operate efficiently over long distances. These fuel cells are designed to deliver high performance and reliability, making them suitable for demanding applications. Finally, the "Above 240KW" category represents the most powerful hydrogen fuel cells, used in specialized applications such as large commercial trucks, buses, and even trains. These fuel cells are engineered to provide maximum power and endurance, supporting the transportation of heavy goods and large numbers of passengers. Each power output category addresses specific needs within the automotive market, allowing manufacturers to tailor their hydrogen fuel cell offerings to meet the diverse requirements of different vehicle types. As the technology continues to evolve, these categories may expand or shift, reflecting advancements in fuel cell efficiency and performance. The Global Hydrogen Fuel Cells for Vehicles Market is poised for growth as these power output categories enable the adoption of hydrogen fuel cells across a wide range of transportation applications, contributing to a more sustainable and environmentally friendly future.

Passenger Cars, Commercial Vehicles in the Global Hydrogen Fuel Cells for Vehicles Market:

The usage of hydrogen fuel cells in the Global Hydrogen Fuel Cells for Vehicles Market is particularly significant in the areas of passenger cars and commercial vehicles. For passenger cars, hydrogen fuel cells offer a promising alternative to traditional gasoline and diesel engines. These vehicles are equipped with fuel cells that convert hydrogen gas into electricity, which powers an electric motor. This process produces zero emissions, making hydrogen fuel cell passenger cars an attractive option for environmentally conscious consumers. The driving experience is similar to that of electric vehicles, with smooth acceleration and quiet operation. Additionally, hydrogen fuel cell vehicles can be refueled quickly, similar to conventional vehicles, which addresses one of the main drawbacks of battery electric vehicles: long charging times. This makes them a practical choice for consumers who value convenience and sustainability. In the realm of commercial vehicles, hydrogen fuel cells are gaining traction as a viable solution for reducing emissions and improving efficiency. Commercial vehicles, such as buses, trucks, and delivery vans, often require more power and longer range than passenger cars. Hydrogen fuel cells can meet these demands by providing a high energy density and extended driving range. This is particularly beneficial for long-haul trucking and public transportation, where vehicles need to operate for extended periods without frequent refueling. The use of hydrogen fuel cells in commercial vehicles also contributes to lower operational costs over time, as they require less maintenance compared to traditional internal combustion engines. Moreover, the adoption of hydrogen fuel cells in commercial fleets can help companies meet stringent emissions regulations and enhance their sustainability credentials. As infrastructure for hydrogen refueling stations expands, the feasibility of hydrogen fuel cell vehicles in both passenger and commercial sectors is expected to increase. This growth is supported by government incentives and investments in clean energy technologies, which aim to accelerate the transition to a low-carbon economy. The Global Hydrogen Fuel Cells for Vehicles Market is thus positioned to play a crucial role in transforming the transportation landscape, offering cleaner and more efficient alternatives for both individual consumers and businesses.

Global Hydrogen Fuel Cells for Vehicles Market Outlook:

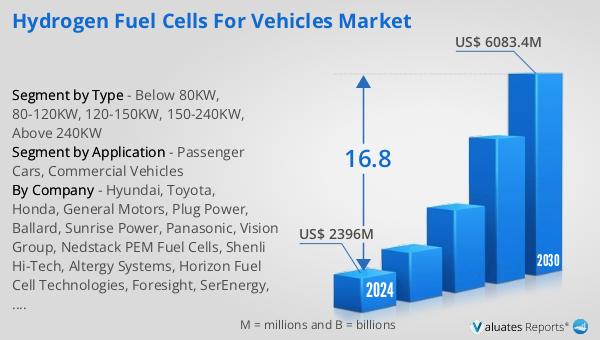

The outlook for the Global Hydrogen Fuel Cells for Vehicles Market indicates a robust growth trajectory over the coming years. According to projections, the market is expected to expand from a valuation of approximately US$ 2,396 million in 2024 to an impressive US$ 6,083.4 million by 2030. This growth is anticipated to occur at a Compound Annual Growth Rate (CAGR) of 16.8% during the forecast period. Such a significant increase underscores the rising demand for hydrogen fuel cell technology in the automotive sector. Several factors contribute to this optimistic market outlook. Firstly, the global push towards reducing carbon emissions and combating climate change has led to increased interest in sustainable transportation solutions. Hydrogen fuel cells, with their zero-emission capabilities, align perfectly with these environmental goals. Additionally, advancements in fuel cell technology have improved their efficiency, durability, and cost-effectiveness, making them more attractive to both manufacturers and consumers. Government policies and incentives aimed at promoting clean energy and reducing reliance on fossil fuels further bolster the market's growth prospects. As infrastructure for hydrogen production and refueling continues to develop, the adoption of hydrogen fuel cell vehicles is likely to accelerate. This market expansion represents a significant opportunity for innovation and investment in the automotive industry, as companies strive to meet the growing demand for cleaner and more efficient transportation options. The Global Hydrogen Fuel Cells for Vehicles Market is poised to play a pivotal role in shaping the future of mobility, offering a sustainable alternative to traditional internal combustion engines and contributing to a greener planet.

| Report Metric | Details |

| Report Name | Hydrogen Fuel Cells for Vehicles Market |

| Accounted market size in 2024 | US$ 2396 million |

| Forecasted market size in 2030 | US$ 6083.4 million |

| CAGR | 16.8 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Hyundai, Toyota, Honda, General Motors, Plug Power, Ballard, Sunrise Power, Panasonic, Vision Group, Nedstack PEM Fuel Cells, Shenli Hi-Tech, Altergy Systems, Horizon Fuel Cell Technologies, Foresight, SerEnergy, SFC Energy, Beijing Sinohytec Co.,Ltd., Stellantis, Cummins, Guangdong Liyuan Technology Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |